Last updated March 2023

In recent years, processing the growing number of credit card chargeback claims among consumers has become a burden for Visa. The time and money associated with processing all of these claims has led the company to overhaul the old model and roll out a new process to address credit card chargebacks.

The proposed changes went into effect in April 2018, and not all merchants understand what this means for their businesses.

Why Change the Credit Card Chargeback Process?

According to Visa’s official document outlining the changes, “With the number of disputes rising, and processing time and costs increasing, Visa is excited to introduce the Visa Claims Resolution (VCR) initiative. To improve the efficiency of handling disputes, Visa is focused on automating and simplifying the dispute-resolution process while also keeping pace with the needs of the payment industry.”

Simply put, Visa is trying to make the system faster, easier, and less costly.

How Will the Visa Chargeback Rule Change Impact Merchants?

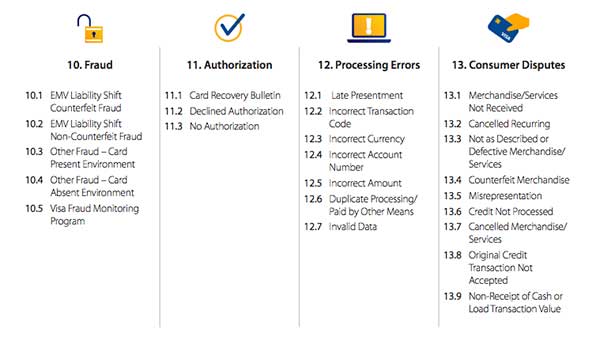

NEW VISA CHARGEBACK REASON CODES HAVE BEEN CREATED

The existing reason codes have been broken into four categories:

- fraud

- authorization

- processing errors

- cardholder disputes

Although the Visa chargeback reasons have been consolidated, the VCR document makes sure to note that “Visa will continue to provide the same level of data received today and, in some cases, additional data to help merchants understand the reason for the dispute.”

So this categorization should simply clarify the nature of the disputes, enhancing the merchant’s ability to respond appropriately.

TWO CATEGORIES FOR VISA DISPUTES HAVE BEEN CREATED

The two new categories classify the previously mentioned codes under either ‘allocation’ or ‘collaboration.’ A merchant’s role in the dispute differs based on which category it is assigned to.

Allocation - is intended for disputes associated with fraud and authorization. During the automated check in the allocation process, Visa will determine factors such as whether the cardholder raised the dispute after the amount of time they are allowed, if 3-D security was used or whether a refund for the charge has been issued. If any of these scenarios has occurred, Visa will block the dispute, and prevent it from becoming a chargeback.

Collaboration - mostly applies to cardholder disputes and processing errors. It is referred to as collaboration because the acquirer, credit card issuer and merchant are expected to work together to resolve the situation. Not much differs in the new collaboration category aside from one notable change: a shorter resolution period.

SHORTER RESOLUTION PERIOD

In the past, merchants had 45 days to respond to chargebacks.

“Visa has enhanced the dispute resolution rules to improve efficiencies and simplify the dispute resolution process,” says Newtek’s EVP of Relationship Management, Tom Harkin. “This will mean that merchants will have less time to respond to a chargeback and they need to provide clear and concise documents to support their case. Otherwise, they will lose the chargeback.”

The shortened span of time--just 30 days--is intended to streamline the period and speed up the Visa chargeback process. The hope is, the new visa chargeback rules will help to resolve chargebacks in as little as 31 days, rather than the previous average of 46.

What Merchants Should Keep in Mind

During the collaboration process, you as the merchant must still prove transactions are valid in order to avoid a chargeback.

According to an article in Digital Transactions, merchants are finding success by building “a solid case with as much information as possible when disputing a chargeback claim.”

This can mean collecting (Address Verification Service) AVS information, screenshots, and transaction dates when accepting credit card payments.

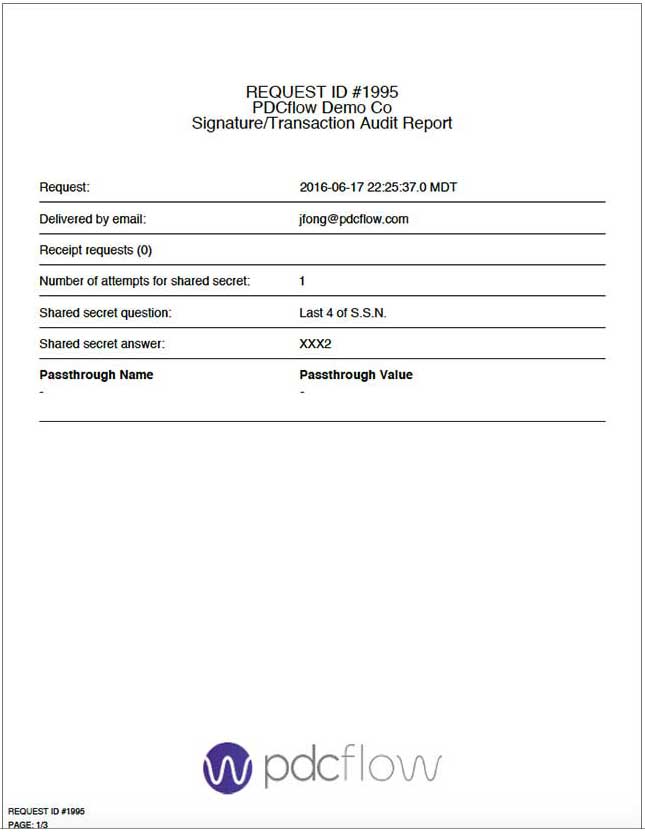

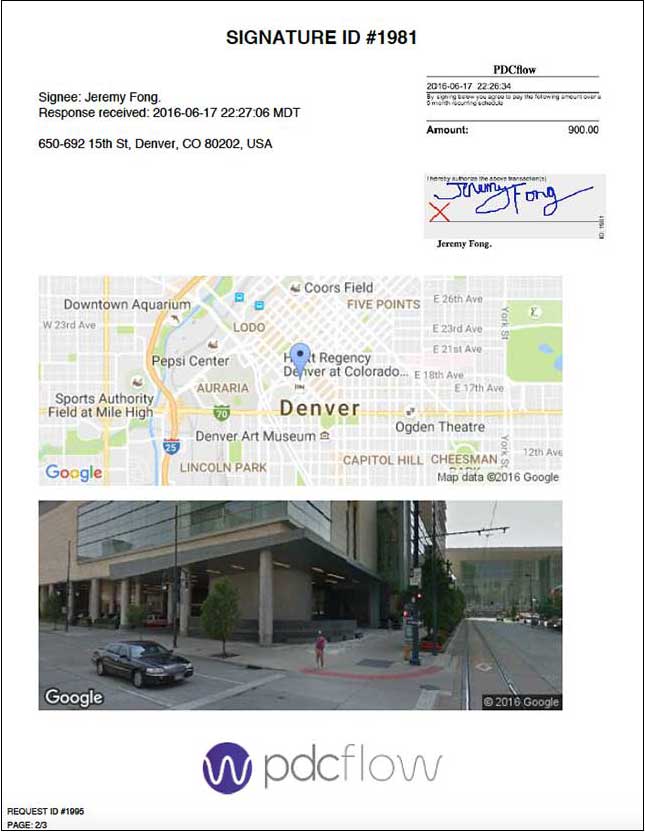

A time-saving option to help fight future chargebacks is to use software that can capture a signature authorizing the payment at the time of processing credit card payments.

PDCflow’s Flow Technology allows a customer to sign at the time of payment via mobile phone, chat conversation or desktop application. It also offers a detailed audit report of the time, date, signature and geolocation information of a payment (this is the piece that will help you fight chargebacks).

PDCFLOW'S FLOW TECHNOLOGY AUDIT REPORT EXAMPLE

Although these Visa chargeback rules are intended to reduce the number of chargebacks your business receives, the best course of action is to minimize your risk upfront.

A comprehensive audit report of the consumer’s payment consent may dissuade a scammer from filing a fraudulent dispute. After all, if there is proof the payment was made from their home address, it’s difficult to deny.

Asking for AVS, requiring the card verification number (CVV), and offering automatic receipts with purchases can also lower the risk of an unauthorized transaction slipping through.

Also, note that some friendly fraud chargebacks occur when consumers don’t recognize how your business is listed on their bank statement. Be sure the description is easily recognizable to avoid this type of dispute claim.

Download our Chargeback Prevention Guide for a quick-glance guide to avoiding chargebacks in your business.

Download Chargeback Prevention Guide:

Want to know more about PDCflow Software?

Press ▶️ to watch our explainer video

ONE-STEP PROCESS

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles