INDUSTRY SOLUTIONS

Debt Collection

Payment and digital communication solutions. Turn a promise to pay into a resolved account.

Book Demo

HIPAA Compliant

HIPAA Compliant UPTIME Achieved

UPTIME Achieved SOC 2 Compliant

SOC 2 Compliant- LEVEL 1 Compliant

FEATURES FOR A DIGITAL WORLD

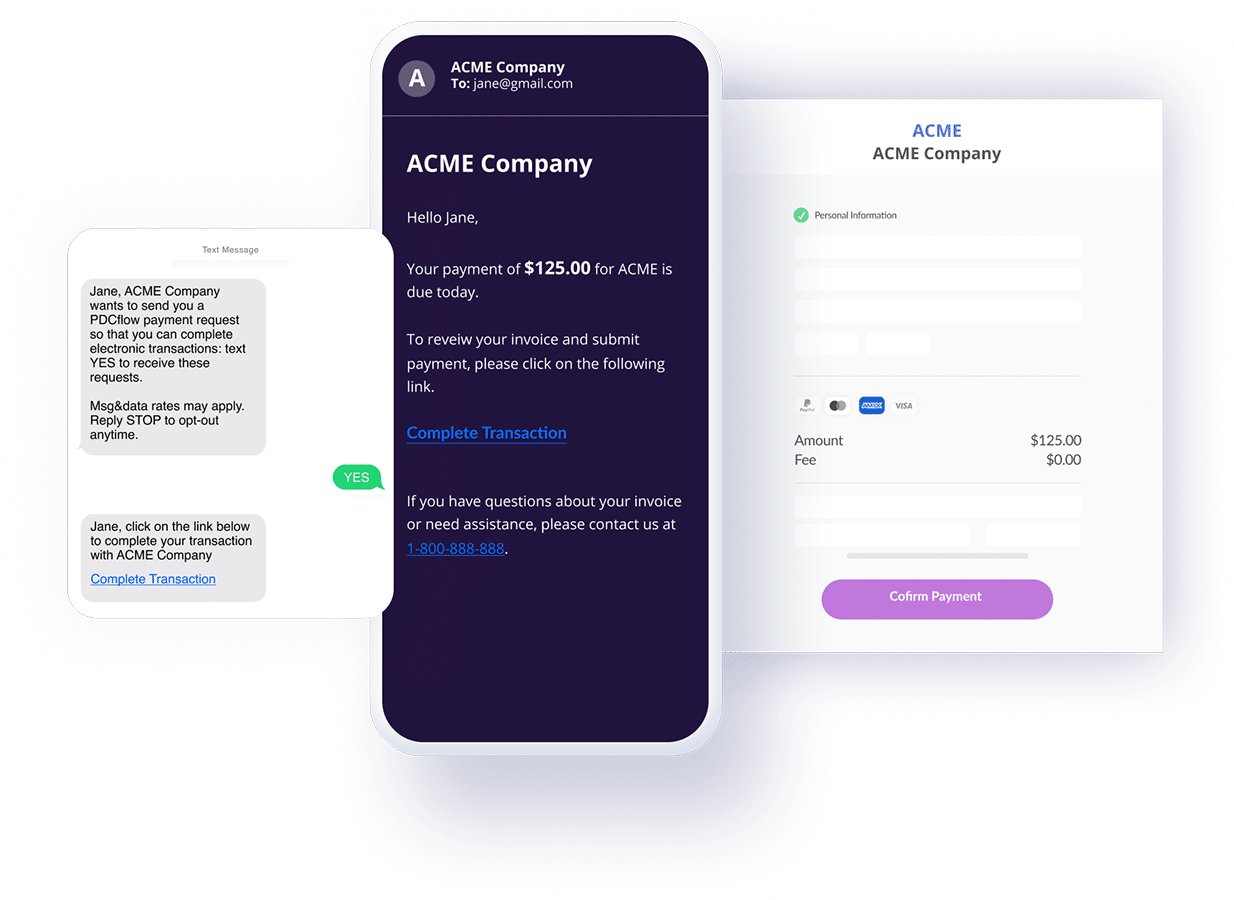

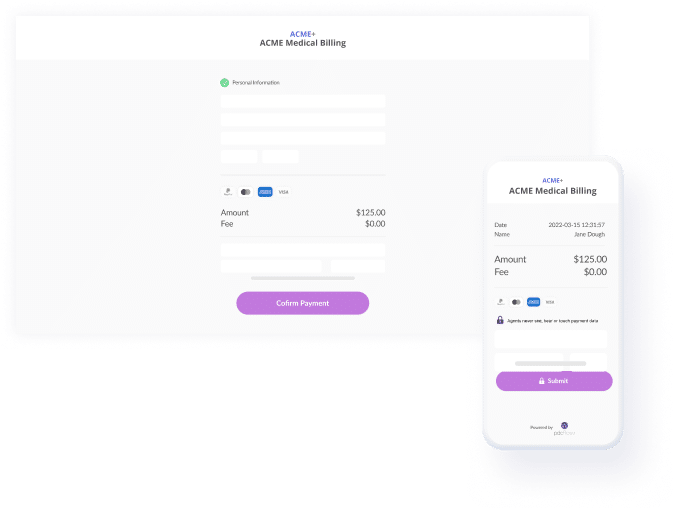

Use email and SMS to engage consumers. Reduce operational costs. Capture payments through the digital channels consumers prefer.

Send Documents

Send Documents- Send Payment Requests

- Gather Legally Binding Signatures

- Request Photo Uploads

Reduce PCI compliance scope

Agents can send payment portals to a customer's fingertips by email or text while on the phone with them. Consumers verify payment details and enter their own sensitive payment data.

Meet Regulation F compliance

Use email and SMS to engage consumers. Send letters, statements, settlement agreements, and payment schedules digitally. Have peace of mind that you are meeting CFPB requirements.

Streamline recurring payments

Set up recurring payments or process future payments with ease. Meet Regulation E compliance. Live phone agents can send payment schedules for review and consent with a wet signature. Enable consumers to set up their own schedules on your portal with payment terms you configure.

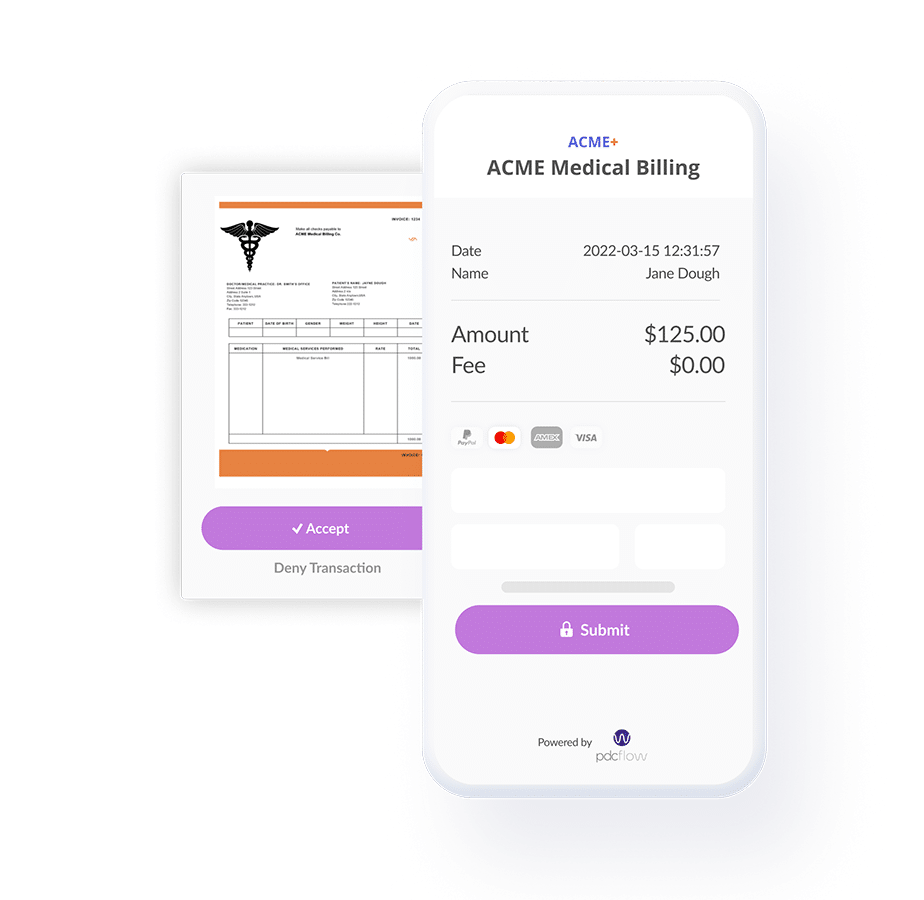

Reduce chargeback risk

Capture a signature on any payment to verify and document consent. One-time, recurring, and settlement payments. Digital audit trail with proof of identity and authorization can be retrieved at any time.

Open API integration

Open APIs make integrating documents, esignatures, and payments to your system of record easy. Receive dedicated integration support from the PDCflow development team.

Merchant account flexibility

Sign up with one of PDCflow's merchant partners. Process credit card payments through traditional or Zero Cost Processing merchant accounts.

HERE'S HOW IT WORKS

Create custom workflows based on your client's needs.

- Create custom workflows

- Accept multiple payment methods

- Allow flexible time frames

- Pull detailed audit reports

- Understand your payment data

Keep clients happy

- Customize portals and payments to process through multiple merchant accounts. Deposit into the bank account your client prefers.

- Send documents, capture signatures, and collect payments through a single vendor.

- Speed up payment collection with secure and compliant email and text messaging.

- Make it easy for your agents to stay compliant. Lock down the workflows they need through your admin configuration.

Give consumers options to resolve their accounts

- Take credit, debit, ACH, and HSA payments.

- Accept payments online, over the phone or through POS, web chat and mobile devices.

- Set up recurring payment schedules and enable self-serve payment options by balance owed: pay-in-full, pay-in-4, or payments of a minimum amount.

- Add custom and personalized QR codes on letters. Consumers only need to scan, click, and pay.

Make resolving past-due accounts easy and secure

- Allow flexible time frames for Flow smart request completion.

- Give your customers minutes, hours or days to review sign, and complete their payment form.

- Send validation notices, settlement letters, or recurring payment terms with a payment form through email or SMS.

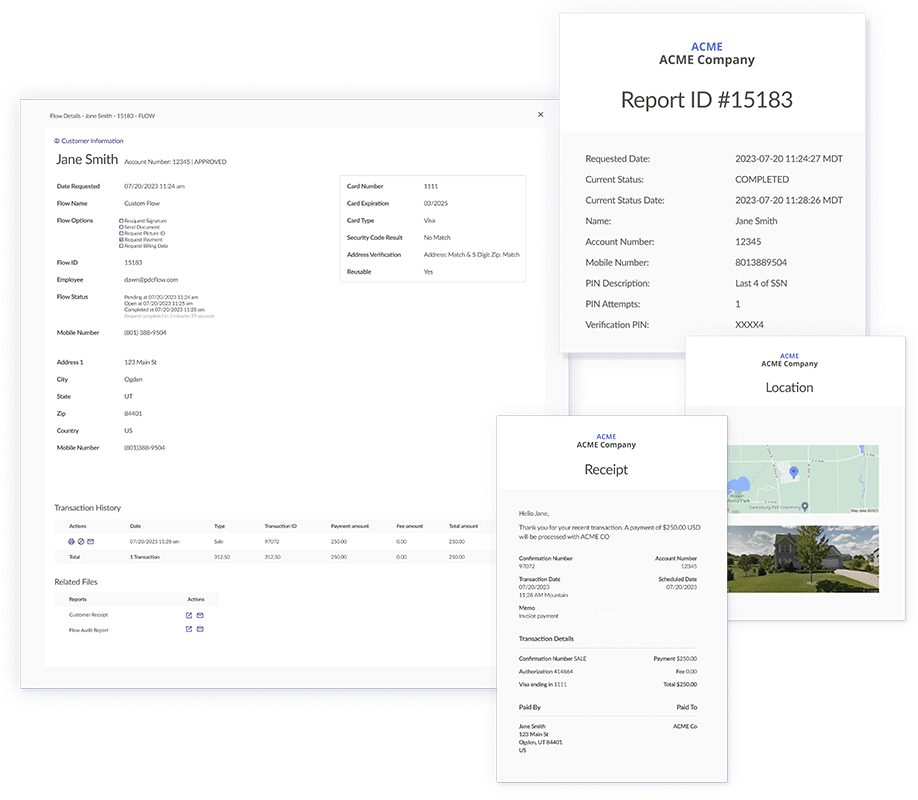

Prove payment consent

- Consumers and staff can access a detailed audit report or receive one via email after a Flow request is completed.

- Report includes: Dual authentication, date/time stamp, method of delivery (email address and/or cell phone number) and a legal wet signature.

- Retrieve at any time. Audit reports are stored for seven years.

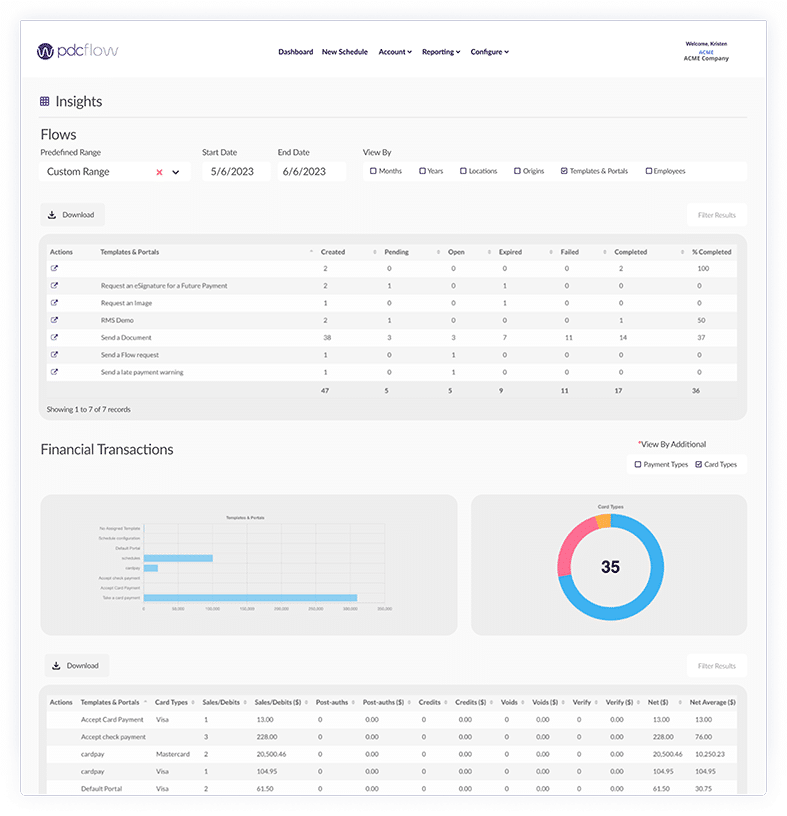

Track payment performance

- View payments and Flow totals in one place. Read consolidated reporting with daily, monthly, or yearly totals on a single report.

- Simplify end-of-the-month number-crunching. Teams now have better visibility over their account activity, including payments and Flows.

- Spot trends and anomalies in payments by monitoring transaction totals over time.

- Filter Flow totals by employee or origin so management can learn more about Flow Technology usage and monitor success rates.

A fully customizable and comprehensive billing solution for your business. Call 1.877.732.4814

LOOKING FOR SOMETHING SPECIFIC?

One system for all your digital payment, esignature, document,

and photo workflows

CASE STUDIES

See how PDCflow can work for your business

Bayview Solutions LLC

Reduced chargeback risk and increased card not present payment consent.

Read Case Study

RMS LLC, Debt Collection Agency

Improved payment compliance workflow and automation of payments.

Read Case StudyTHIRD-PARTY REVIEWS

Don’t just take our word for it.

“PDCflow has been working out great for clients and debtors! It is easy and convenient to use. And it allows debtors to make their own payments.”

Alison J.

Debt Collection Agency

4.6 (56+) Capterra Reviews

4.4 (50+) G2 Reviews

Integrate fast and easy with our open APIs

Explore API Integration

Set up better payment communication workflows

Consult with a Payment Communication Expert to learn how.

Get Started

Not quite ready?

Continue learning with PDCflow resources

Guide to Emailing Model Validation Notices

If your debt collection agency doesn’t use email to talk to consumers, you’re never going to

Read Blog Post