Creating a digital omnichannel strategy for debt collection is essential for the future. Technology is readily available and there are compliant ways to use it to better connect with consumers. How do you know what you’re planning (or what you’ve already set up) is working as well as it could?

Three digital collections experts, Pran Navanandan, Halsted Financial Services, Dianne Harrell, Resident Interface, and Justin Franklin, Cedar Financial, recently paneled a webinar with Accounts Recovery to discuss what digital collection means and ways to monitor your efforts.

What Does Digital Collection Mean?

"Any collections as a result of electronic means."

PRAN NAVANANDAN

"For me, it's the ability to reduce the need for agent interactions and still be able to service the consumer."

DIANNE HARRELL

“We like to measure specifically how they’re engaged through our inbound channels – SMS, email, social media – and then, what channels are we using outbound to get them engaged?”

JUSTIN FRANKLIN

All of the panelists agree that both inbound and outbound efforts are included in an omnichannel strategy. The most common channels used for digital collection include:

- SMS

- Letters with QR codes

- Web chat or chatbot

- Online payment portal

- Voicemail drop

- Social media

- Digital ads

Omnichannel Strategy Data Points to Measure

Portal Metrics

You should be paying attention to the number of people that visit your website’s portal, where they originated from and why they are there.

“One of the most obvious [metrics] would be new users to your portal,” says Franklin. He encourages “tracking how many people are engaged – and through what channel.”

Following this trail teaches you people’s preferred methods of interacting with you. It’s also important to focus on your portal’s close rate, just as you would measure the effectiveness of an agent.

Abandoned payments or unresolved issues after visiting could mean your website is poorly designed or doesn’t include everything consumers are looking for.

SMS and Email Metrics

SMS and email are some of the most common omnichannel communication methods for merchants. Both are typically measured by how much engagement they’re generating and how many messages either failed to be delivered or caused someone to opt-out.

After all, you want to maximize the number of people who see and respond to your communications. Easy opt-out is essential. It narrows your company’s focus, allowing you to better engage with the people who want to resolve their accounts.

“The three biggest metrics that we look at on email are spam complaint rates, bounce rates and opt out rates,” says Navanandan. “At the most basic level, if your spam rates are above two percent, then your opt out buttons probably aren’t placed in the right place or the email addresses you are receiving and the business you’re working may not be the best business in the world for a digital effort.”

Self-Serve and Customer Satisfaction Metrics

Many pieces of omnichannel technology encourage self-serve actions like making an online payment, using a chatbot to get information or even filing a dispute through your portal. You should monitor how effective your digital channels are when your office is closed or no agent is involved.

Customer surveys can also give you insight into your digital customer journey, including what people like and what should be improved.

“We actually get a lot of feedback from consumers on our virtual agent, our portal,” says Harrell. “What could we do better? What do they want to see on there? Was it easy to use?”

Measuring the Negatives

The panelists all agreed that measuring negative feedback is just as crucial as identifying what is going well. When a consumer doesn’t answer your call, you will most likely never know why.

In gathering omnichannel customer engagement metrics like opt outs, disputes, and complaints, you can better understand why some accounts aren’t engaging. This saves money on future phone calls, letters and other collection efforts you would use to connect with someone who never intends to pay.

Heatmap Tracking

Heatmap software tools allow your company to watch who is on your website and where they are looking, scrolling or clicking on each page. The panelists all confirmed they use a tracking tool to monitor site activity. With heatmap tracking, you can:

- Monitor where people are clicking on pages to understand how easy your site is to navigate.

- See how far down consumers scroll, so you know if your website messaging is effective.

- See how long people stay on your portal to get a fuller picture of how hard it is to take the action they want.

- Identify who is abandoning payment, so you can follow up through email to offer extra help.

Does an Opt-Out in One Channel Mean a Total Opt Out?

As with most compliance questions in accounts receivable, there isn’t a definitive answer to what an opt out can mean. But there are some common scenarios that might cause you to act differently depending on each situation.

- If the issue is a wrong contact, they should be opted out of communications.

- If it’s a simple unsubscribe in one channel (like email) but they reach out later via another (like a phone call), you may just take that opportunity to verify and update their preferences.

- If the request is in the form of an angry or aggressive response, you may consider marking it as a dispute.

Remember, before deciding how to handle your opt out policies and procedures, you should consult with your compliance team.

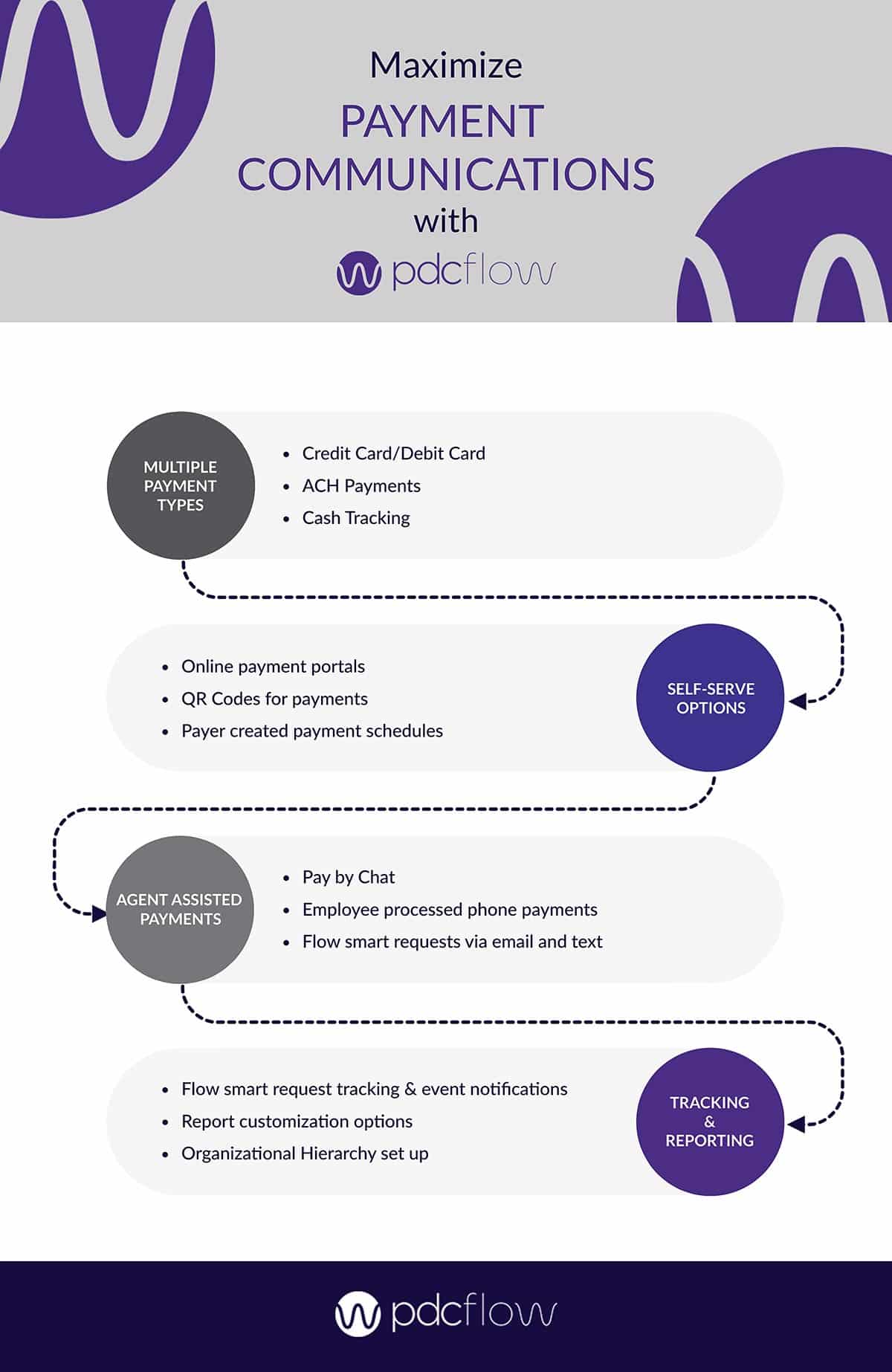

What to Offer on Your Portal?

Portals on your website are most known for self-serve payments but they can help your agency in your digital efforts in many ways. What else can your portal do for customers?

“Really anything they would do on the phone with your agent, there has to be a way for them to either perform that action that they want to do, or get the information they need on how to perform that action,” says Franklin.

Here are just a few of the common uses for an accounts receivable consumer portal:

- Payments

- Dispute processing

- Requesting you to stop calling/contacting them

- Managing preferences

- Attorney information

- Bankruptcy information

You want to learn as much as you can about why consumers are disputing a bill, why they aren’t engaging or other reasons for failing to pay. The information they provide is valuable, and can teach you how to create a better consumer experience in the future. Why not make the process as easy as possible?

How Much of Your Collection Activity Should be Digital?

In the last few moments of the discussion, the panelists covered their opinions on how much collection activity should come from digital or omnichannel strategies. “It’s important to start with a baseline and make sure you’re progressing from there,” says Harrell.

Is your agency making plans to increase your digital debt collection efforts? Are you adopting new software tools and strategies? These steps mean you are already trending in the right direction.

“I think more important than feeling good or bad about whatever level of digital activity that you have at this point, it’s more important to consider the direction that it’s going,” says Franklin.

There are two main factors that can impact your digital efforts:

- The product, client and inventory you are working

- Where your company is in the digital journey

Based on the type of debt you are working with, how old it is, or the type of client it originated from, you may not have the ability to use a full omnichannel strategy. Also, if your agency is new to digital collection, you may not be ready for extensive digital tactics.

Navanandan says that the most important thing to help you progress is simply getting started.

“Everyone has their different benchmarks. Everyone has their different goals. Again, if you’re trending in the right direction and the overarching goal is collecting more from your digital efforts on a month-to-month basis, it’s not going to happen without action.”

They all encourage agencies to begin using more digital tools and omnichannel strategies to increase collections, reduce manual work for agents and enhance the consumer experience.

No matter where you are in the journey to adopt digital tactics, PDCflow can help. Request a call from a PDCflow Digital Workflow Specialist to learn more.

Want to know more about PDCflow Software?

Press ▶️ to watch our explainer video

REDUCE RISK

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles