FAQs

What is an ACH payment gateway?

Just as credit card payments are processed through a gateway, ACH payment gateways facilitate moving funds from one party to another. An ACH payment gateway is typically the payment processing software vendor that lets a company initiate ACH transactions.

In addition to the ACH payment gateway, businesses need to secure an ACH merchant bank account to take payments from customers. Your payment processor should have existing Merchant Service Provider relationships you can lean on to get your account set up.

Why use an ACH payment gateway?

Why should your business take payments using an ACH payment gateway? It’s important to offer ACH payments so customers have more ways to pay.

Along with catering to customer preferences, ach transfers can be an advantage to your business through:

- Seamless security - It is harder to commit fraud through ACH payment gateway transactions.

- A cost-effective solution - ACH transactions come with fewer fees than credit cards.

- Easier merchant account approval - It is often easier to get approved for an ACH merchant account than a credit card account.

PDCflow’s ACH payment gateway

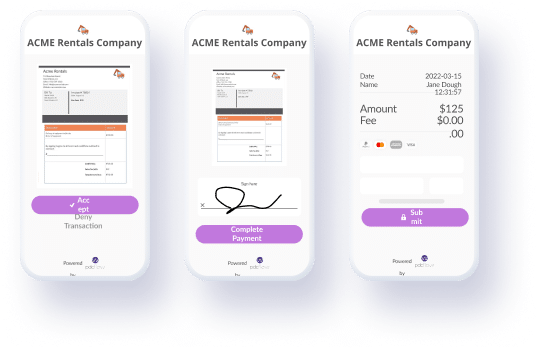

Our ACH payment gateway simplifies payment processing, builds trust with customers, and increases engagement. With PDCflow ACH payments, you can:

- Accept ACH payments through an online payment page

- Automate recurring payments

- Send ACH payment requests through email and text

- Send recurring payment schedules to be approved through email and SMS

ACH payment gateway APIs

Companies can take ACH payments through a front-end application, through an integration offered within a current system of record, or through ACH payment APIs.

For companies that need to monitor their ACH payments from their system of record, ACH payment gateway APIs are a fast, simple way to make that possible.

What to look for in your payment APIs:

- Drop-in options

- Low-code components

- Support from software developers

ACH payment gateway costs

ACH payment gateway FAQs

What information is required to process ACH?

Routing and account number of the account to be debited or credited.

What if the consumer does not have the routing and account number?

When will the merchant be funded?

The merchant will see their settlement in 1-5 days typically.

How much does a returned ACH payment cost?

What is a proof of authorization?

A proof of authorization is how you prove a customer has authorized or provided consent for the transaction you intend to run.

Who governs ACH transactions?

Nacha is the governing body that creates rules to guide safe, reliable ACH transactions. Nacha creates, maintains, and enforces the ACH network rules.

What does NACHA stand for?

Nacha stands for National Automated Clearing House Association.