Giving your customer more choice and an easy-to-use payment system can remove most of the objections that cause your business to lose out on money. These choices can mean types of payment or a preferred payment channel.

Credit card, ACH and cash payment types aren’t enough on their own. Your business should also have:

- An online payment portal so customers can pay without the help of an employee

- Mobile-friendly payment workflows so people can take care of bills from anywhere

- Outbound payment communication tools, so you can send email/SMS reminders and requests rather than slow, inefficient paper bills

Payment Types

Every modern business should accept the most common payment types through a multi-channel payment solution so the process is as simple as possible for customers.

For those expanding their payment offerings or getting ready to modernize, here are the basic pros and cons of the most common payment types – and how payment communication software can tie your digital customer journey together.

Why Use Credit Cards

Accepting credit card payments is an easy way to make customers happy. Credit cards are popular and customers assume they will be able to use a card to pay almost anywhere.

If your business isn’t using credit card processing services, it is creating inconvenience, low customer satisfaction and more abandoned payments.

Credit card payments are also good for merchants who prefer fast payment funding. Cards are usually funded within 24 to 48 hours of approval, while ACH payments can take up to four business days to fully process.

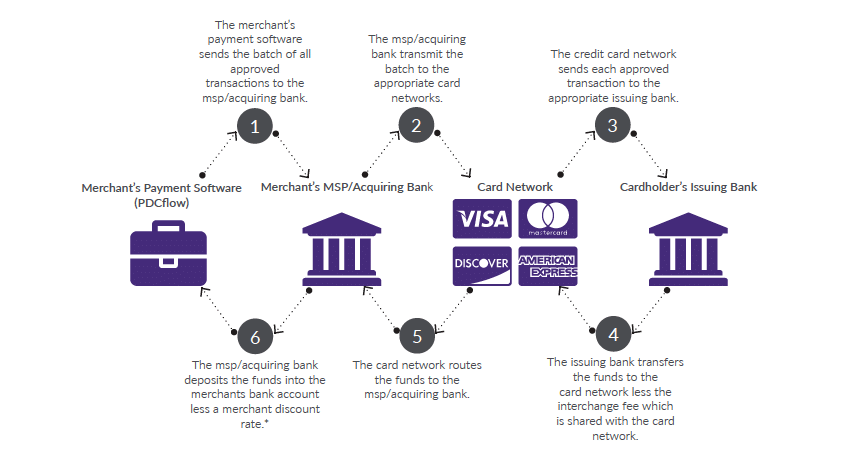

Credit Card Batching and Funding Process

What to Know First

Accepting every type of payment comes with positives and negatives. Some small to midsize businesses hesitate to take card payments because they don’t know what fees to expect from a merchant service provider or how to handle Payment Card Industry (PCI) compliance.

High risk businesses like debt collection can also make it harder to obtain a merchant account and come with rules about how to maintain chargeback ratios.

How PDCflow Can Help

PDCflow offers credit card processing that makes it easy to verify valid card numbers and take secure payments. Some features of PDCflow credit card processing include:

- Merchant Service Provider (MSP) relationships to help you get a merchant account for your business.

- Security - customers key in their own payment information, reducing PCI compliance scope. Information is then tokenized and encrypted, keeping card numbers secure.

- Automated fraud prevention through Card Verify technology, which checks that a credit card is good before a recurring payment schedule runs. Validating the card upfront can help scheduled transactions run more smoothly by flagging avoidable errors before storing.

Why Use ACH Payments

Not every consumer wants to pay with a credit card. Using ACH payments along with credit cards gives people the choice to pay the way they want, which opens your business to a wider range of customers.

If your company charges fees for credit card payments or works under a zero cost processing merchant account model, you may also want to offer ACH processing as a fee-free payment option for customers.

What to Know First

ACH funds typically take up to four business days to process, which can make reconciliation difficult if you’re not used to longer funding times.

It’s also important to know that ACH payments can be subject to fraud, just like credit cards. Merchants need to follow guidelines put out by Nacha (National Automated Clearing House Association) to keep customer bank account information secure.

How PDCflow Can Help

PDCflow’s ACH payment processing allows companies to:

- Get a merchant account to process ACH payments through one of our vendor partners.

- Comply with Nacha through ACH Verify technology to validate a bank account before payment is processed. This prevents fraudulent transactions and catches wrong numbers typed in error before a transaction is submitted.

- Keep bank account information secure through tokenization and encryption.

Accepting Cash Payments

How PDCflow Can Help

How Payment Channels Impact Customer Experience

- Online payments: customers need a way to pay online, without the help of an employee. Use a branded payment portal so customers know they’re in the right place.

- QR codes: printing a QR code to your portal on a paper statement directs them exactly to where they need to go, saving customers time.

- Recurring plans: for big ticket items, you should have flexible options to create a payment schedule, either with a staff member or on their own through your portal.

- Mobile friendly: using a phone is the easiest way for many people to pay. The mobile view of your portal and other payment workflows should be good looking and simple to navigate.

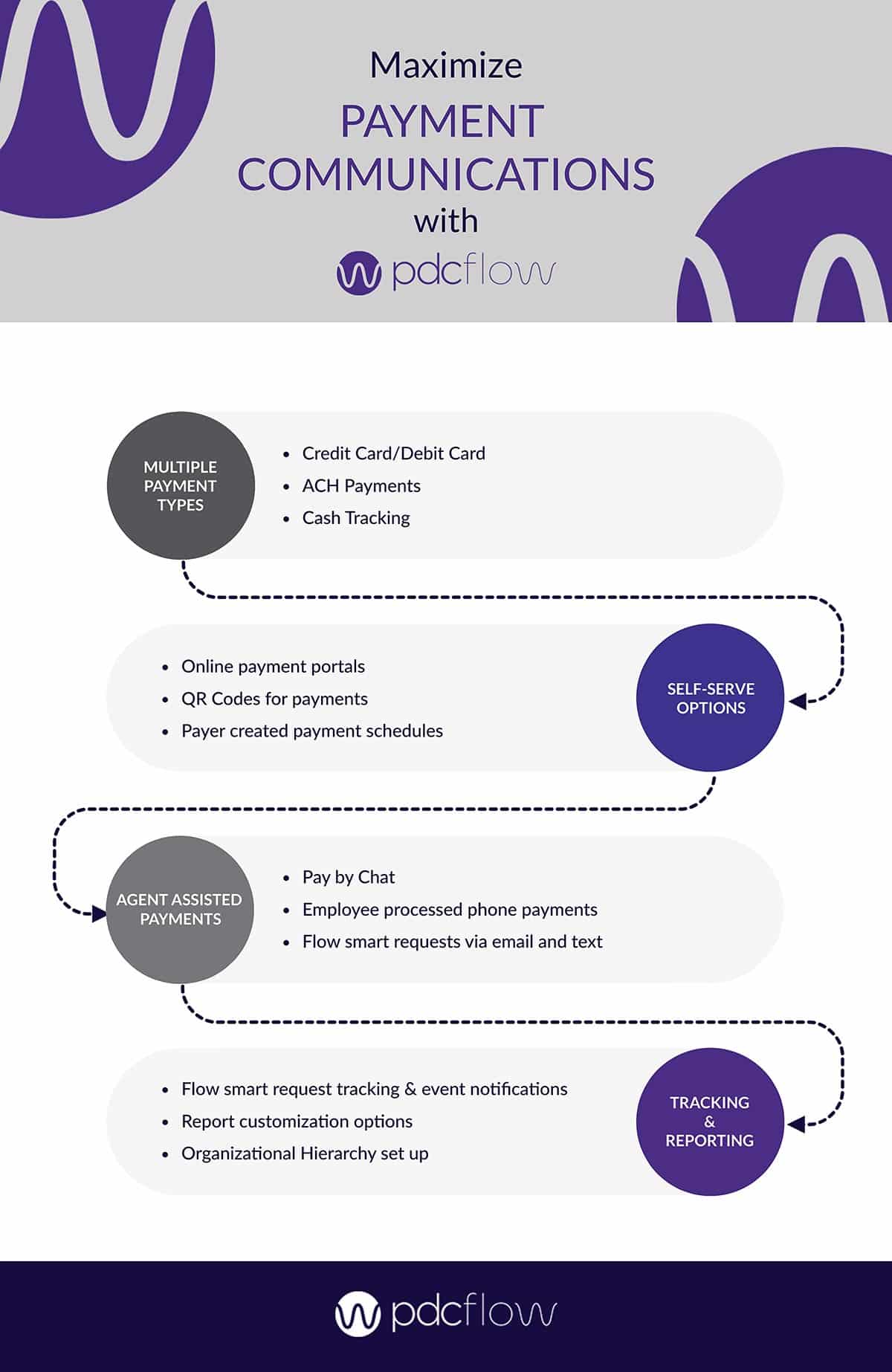

PDCflow Payment Types, Channels and Workflow Management

PDCflow offers credit card and ACH payments along with cash tracking, so companies can manage all of their transactions in one place. These options work together with our unique, proprietary software (Flow Technology) that makes it easy to engage customers and simplify how they can pay.

PDCflow’s Flow Technology is a delivery system that uses email and SMS to help companies:

- Send payment requests to a phone or email address, so a customer can click a link and pay immediately.

- Send recurring payment schedule details to a customer and gather authorization to begin taking payments.

- Send payment reminders of an upcoming scheduled payment to stay compliant with regulations and help customers plan for future payments.

- Send a contract to be signed along with payment request, so both items can be completed in a single transaction.

Managing Payments Through Organizational Hierarchy

PDCflow’s software allows administrators to control employee access by different segments – group, location or department. This lets businesses:

- Manage multiple merchant accounts in one software

- Separate transactions by group or location

- Designate account access controls for staff members to reduce human error

Providing your customers with choice is essential to collecting the most payments possible. For more information about PDCflow’s payment management features, request a demo today.

Book Demo:

Want to know more about PDCflow Software?

Press ▶️ to watch our explainer video

ONE-STEP PROCESS

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles