Guide to processing ACH transactions

Many people have made a payment through the Automated Clearing House (ACH), whether they realize it or not. What is ACH and what are ACH transactions?

What is an ACH transaction?

“The Automated Clearing House (ACH) is the primary system that agencies use for electronic funds transfer (EFT). With ACH, funds are electronically deposited in financial institutions, and payments are made online.” ACH transactions are also known by other names:

- electronic bank transfer

- eCheck (or electronic check)

- direct debit

This network of payments is governed by Nacha, which creates and enforces operating rules for any organization that uses ACH as a payment method.

“Nacha governs the ACH Network, the payment system that drives Direct Deposits and Direct Payments with the capability to reach all U.S. bank and credit union accounts. We advance the nation’s payments system and deliver payments education, accreditation and advisory services.”

ACH transactions are a common way of sending money and are gaining even more popularity for a variety of B2C and B2B payments. Here are a few types of ACH payments that are seeing growth.

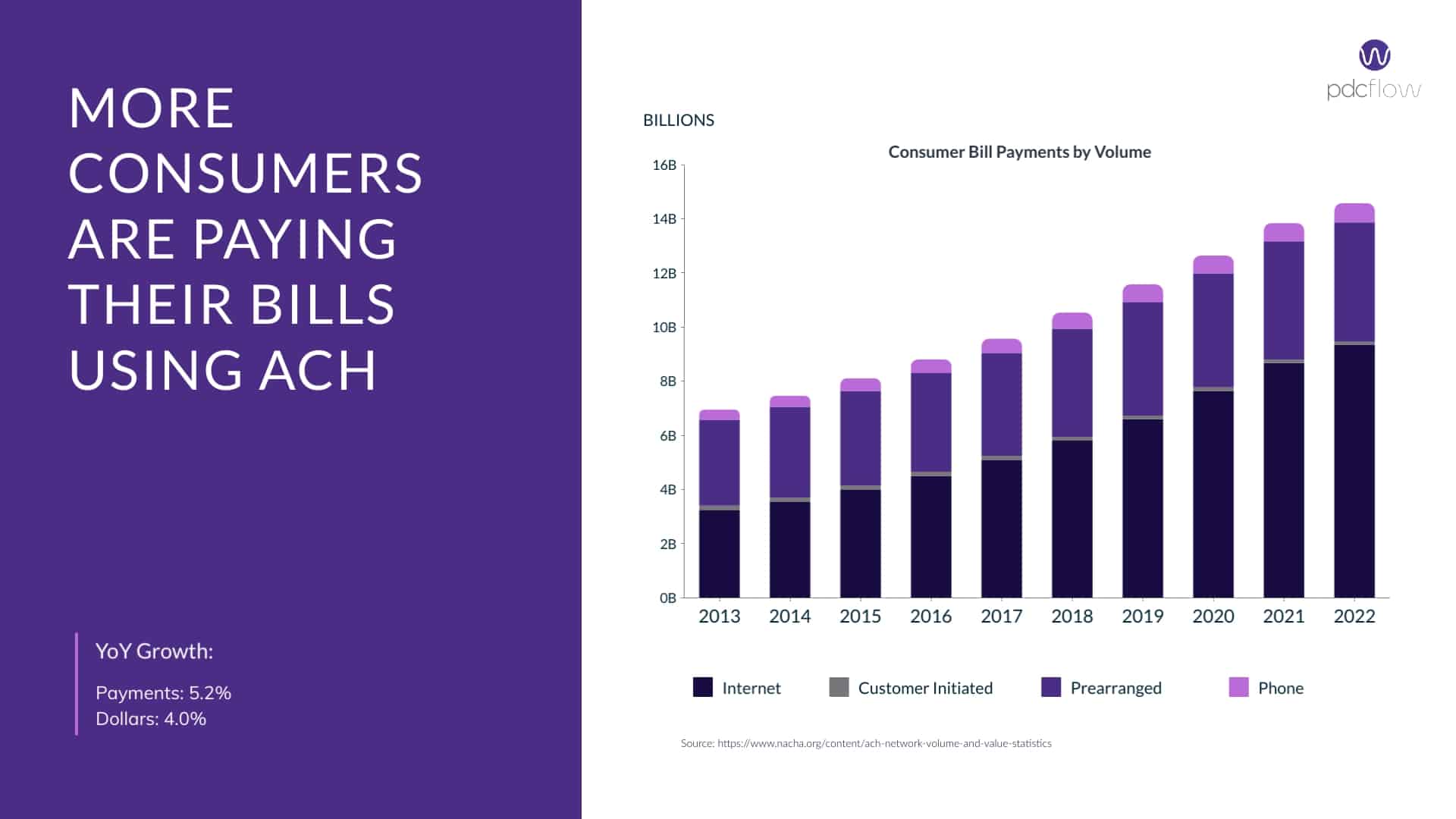

Consumer Bill Payments

The volume of consumer bill payments via ACH has climbed steadily over the past decade, with a 5% year-over-year increase.

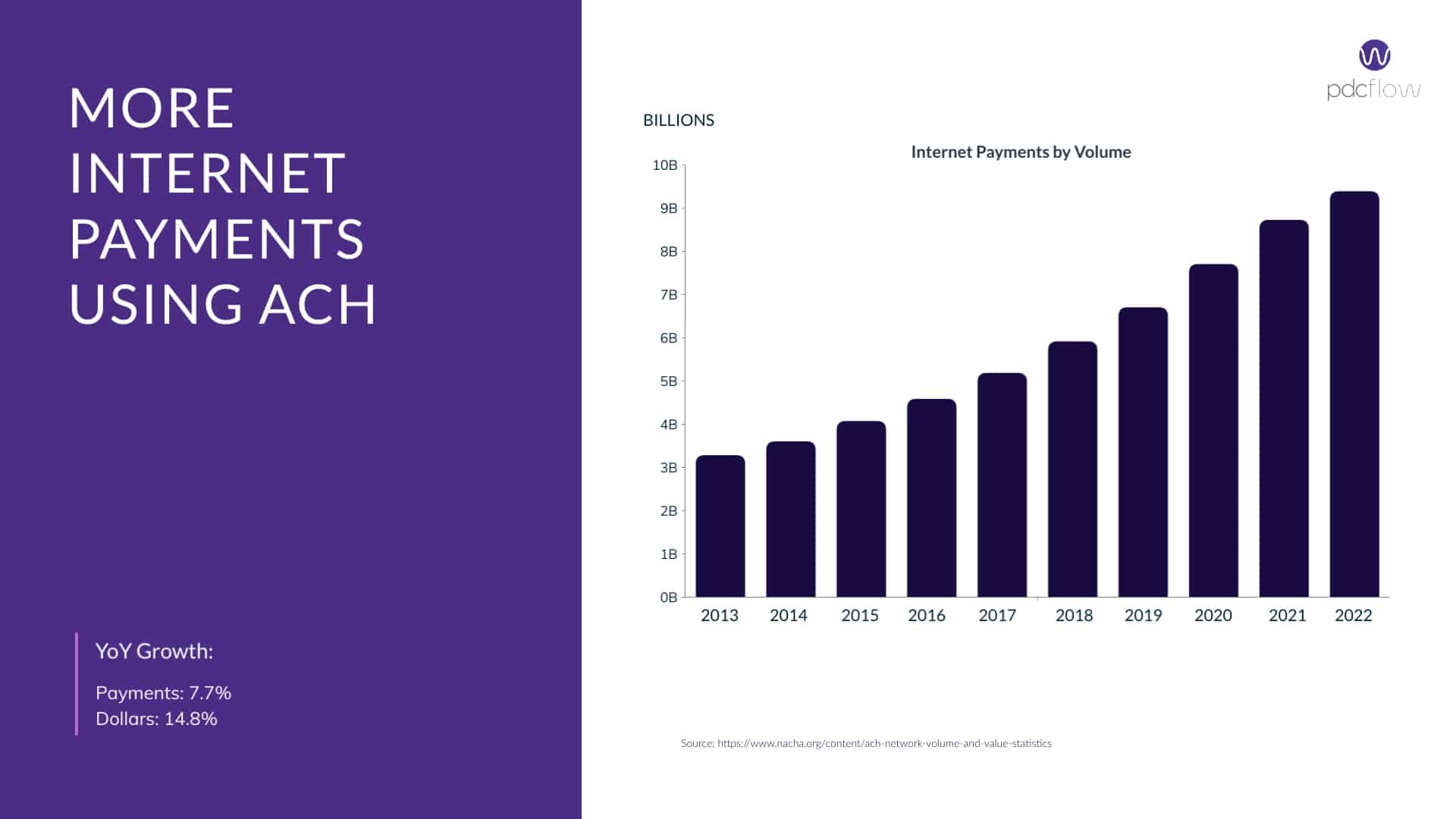

Internet Web Payments

The increase in web payments has contributed to the number of ACH transactions made each year. As companies make online payments easier, ACH electronic payments have become a more convenient way to pay.

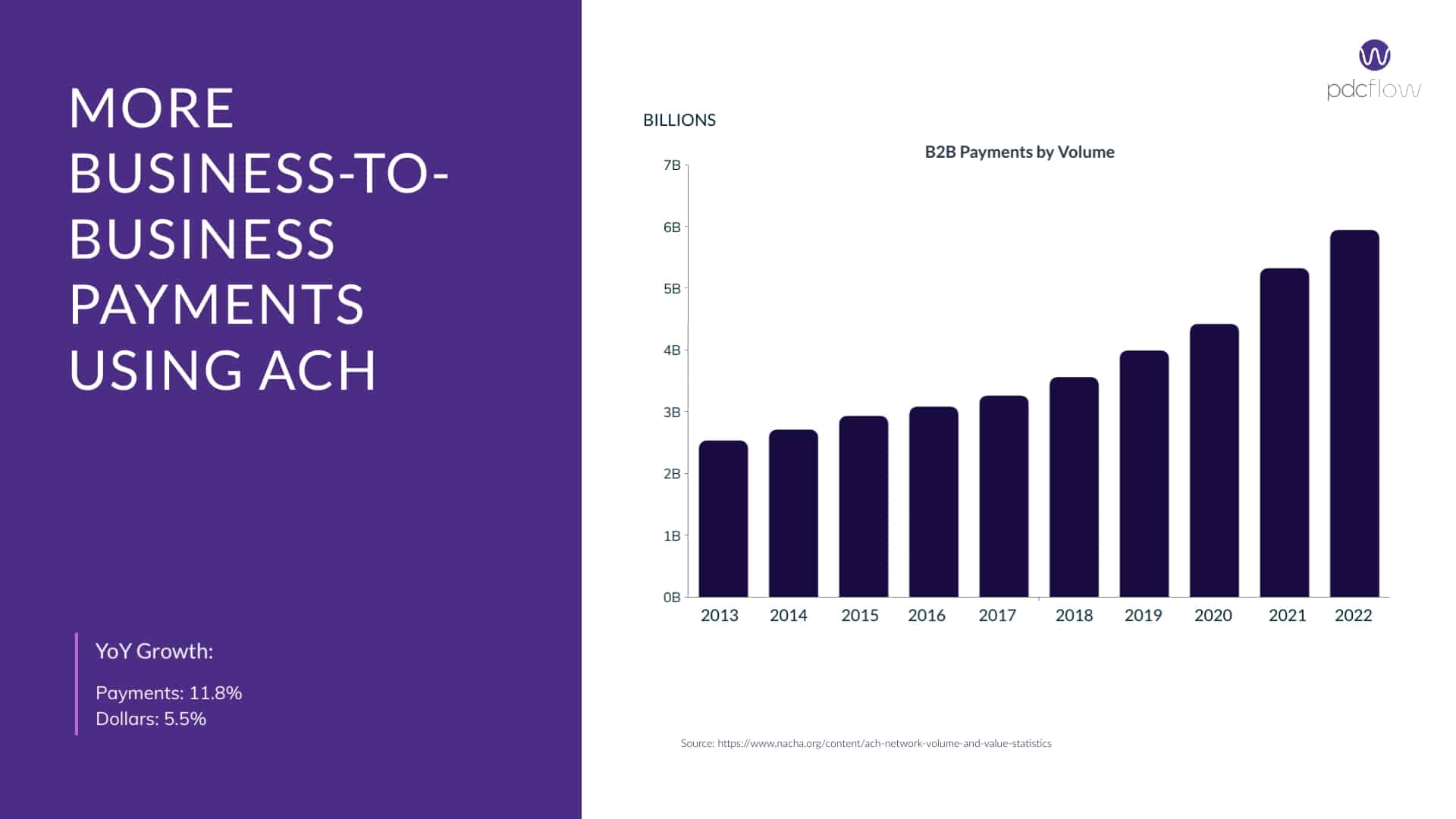

Business to Business Payments

It has been common for years to make B2B payments through ACH transactions. Just as with internet transactions and customer bill payments, business to business ACH has seen steady growth.

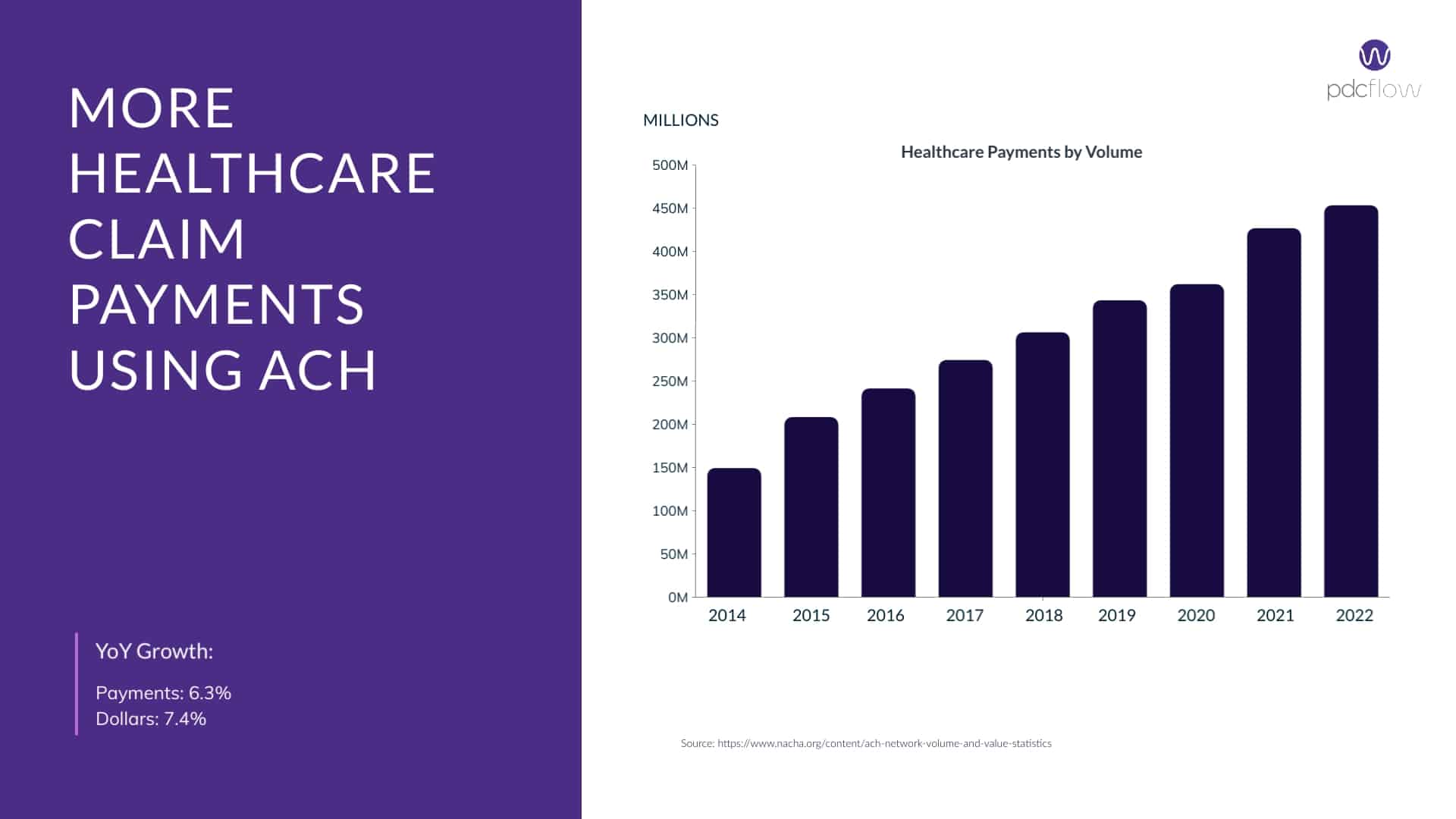

Healthcare Payments

With the rise of high-deductible healthcare plans, patients have taken on more responsibility for medical bills than was typical just a few decades ago. Greater patient responsibility and more choice to pay with a bank account online has caused an increase in ACH healthcare payments.

ACH glossary

ACH transactions come with their own set of terms to describe the parties involved, and the stages and situations that may arise during the course of taking an ACH payment. Here are some common terms you may need to know:

- Chargeback - Sometimes, a customer disputes an ACH transaction on their bank account. This type of return is called a chargeback.

- Credit - If a batch has already been submitted to the ACH network but a transaction needs to be stopped from processing, you must credit the customer rather than voiding a payment. Crediting an ACH transaction requires the merchant to have a reserve of funds in their merchant ACH account. If a company can’t keep reserve funds in their merchant account, they cannot perform credits and instead must cut a paper check for refunds, offer discounts on future purchases, etc.

- EFT - Electronic Funds Transfer. ACH debits, like those initiated through the phone or online, count as EFTs.

- Hold - When a payment is authorized by the owner of an account and the bank in charge of that account reserves (or holds) the specified payment amount.

- ODFI - Originating Depository Financial Institution. The originator is the individual or institution that initiates a transaction.

- Proof of authorization - To comply with ACH payment requirements, merchants must obtain authorization from consumers that they approve of the funds being charged. Proof of authorization is the signature, voice recording or other assets you use to gather that consent.

- RDFI - Receiving Depository Financial Institution. The receiver is the individual or financial institution that is on the receiving end of a transaction (either receiving debited funds or having funds removed at the request of the originator).

- Return - ACH transactions can be returned for many reasons. Often, this is because of a lack of funds in an account or some other problem with the customer or their financial institution.

- Return rate - Large amounts of returned payments cause risk to financial institutions. In addition, companies with too many returns indicate there are inappropriate business practices happening, causing too many customers to dispute their transactions. To keep customers safe and hold businesses accountable, Nacha has created a return rate threshold companies must stay under if they wish to keep taking ACH transactions. There are three types of return rates:

-

- Overall return rate - 15 percent

- Administrative return rate - 3 percent

- Unauthorized return rate - 0.5 percent

- Void - An ACH payment void stops a transaction from being submitted to the ACH network. You can only take this action before a payment batch is sent to the ACH network.

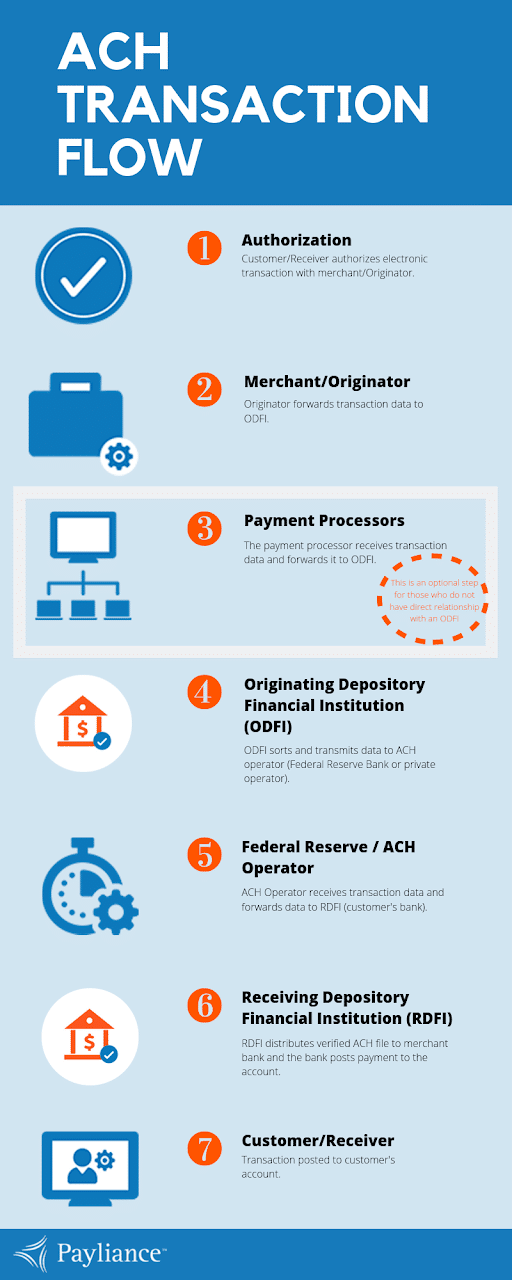

How ACH processing works

The most important thing merchants need to understand about ACH transactions is that they aren’t submitted in real-time as your business takes each payment. The transactions are gathered throughout each business day and sent to the ACH network in a batch.

After this, transactions follow several additional steps before they can be processed and funded into a merchant account. Here is how it works:

1) Authorization - ACH transactions must be authorized by the payer. Make sure to gather the proper consent from customers when you submit a transaction.

2) Merchant/Originator - Once a company submits the ACH transaction, the details are forwarded to the ODFI.

3) Payment Processors - Many merchants use a payment processor to manage their transactions. If this is the case, the processor is the party responsible for submitting payment details to the ODFI.

4) ODFI - After payment details are received, the ODFI sorts and transmits necessary data to the ACH operator.

5) Federal Reserve/ACH Operator - the ACH operator (either Federal Reserve bank or private institution) receives the information and sends it to the RDFI.

6) RDFI - Posts the payment to the necessary account.

7) Customer/receiver - finally, the transaction is posted to the customer/receiver’s account.

ACH vs. credit card processing

When deciding what payment types to offer customers, merchants – especially small to midsize businesses – may not know there are some major differences between offering card payments and ACH to customers.

Each payment type has advantages and disadvantages. Here are a few pros and cons of ACH transactions vs. credit card payments.

Pros

- Lower fees - ACH transactions come with fewer fees than credit cards.

- Good for high ticket items - Customers sometimes prefer using a bank account number to pay for high ticket items. This can be because they don’t want to accrue interest on a credit card for a large purchase or because there are additional fees charged to them for using a credit card to pay. Merchants often prefer ACH for large bills too. Because credit card payments typically charge processing fees by the percent, the bigger the invoice, the more money a company will have to pay to process the payment. For example, a $1,000 ACH payment would cost a company around $0.35 - $1.00, whereas a credit card payment with a 3% merchant service provider fee would cost $30 to accept.

- Easier merchant account approval - Despite underwriting asking for more documents from merchants, it's easier to get approved for ACH than cards. Especially for a startup.

- Security - It is harder to commit fraud through ACH transactions because it is typically more difficult for fraudsters to find a consumer’s bank account number and routing information than a credit card number.

Cons

- Longer funding times - Because payments are typically batched and sent once per day, it takes longer for the money to end up in a merchant account. Companies should plan on a four day hold until money will be funded.

- More documents during underwriting - Although it can be easier at the end of the process to get approved for ACH payments, the application usually requires more documentation.

- High risk merchants require more documents - Those in high risk industries may find themselves providing even more information to ACH vendors than the typical merchant. For example, debt collectors must submit a collection license for every state they operate in, which some may see as a deterrent if they don’t have their documents easily accessible.

- Fewer consumers prefer ACH transactions - Most people who don’t use a credit card opt instead for a debit card. Although the money comes from a bank account during these transactions, they are not considered ACH debits and can only be processed with a credit card merchant account.

ACH frequently asked questions (FAQ)

ACH payment processing works differently from credit cards. There are different fees and funding times to be aware of, unique return rates to monitor and codes to understand. Here are some of the frequently asked questions merchants have about ACH.

What is an ACH debit transaction?

An ACH debit transaction is an electronic transfer of funds, typically taken from the payer’s checking account. Once funds are removed, they are transferred to the recipient’s account.

How long do ACH payments take to process?

Standard ACH processing services use a four day hold system before funds are available in a merchant account. This only includes business days, so funds are typically available within a calendar week of the transaction.

How much does a returned ACH payment cost my business?

ACH transaction fees vary depending on the reason for the return. Basic returned payments can cost between $5 and $10 each. The typical return fee for an unauthorized ACH payment (or chargeback) can be as high as $25. These fees add up fast and also negatively impact your company’s return rates.

How can I avoid returned ACH payments?

- To decrease ACH disputes, let consumers know what your company’s descriptor will look like on their bank statements and provide a customer service number on your receipt. This is typically done through your ACH payment gateway.

- To avoid administrative returns, require customers to enter their account number twice for online payments (to avoid error due to mistyping a number). Tools like PDCflow’s ACH Verify enhance this process by validating account information before transactions are submitted and providing a notification for invalid accounts.

- Properly train your staff on company policies to reduce errors.

- Gather the required consent before running transactions, so you know you’re covered in the event that you must produce proofs of authorization.

- Educate customers on company policies regarding payments, so there are no surprises when it’s time to pay.

What is a proof of authorization?

A proof of authorization is how you prove that a customer authorized the transaction you intend to run. Nacha has designated different transaction types, determined by the way your customer pays. The most common ACH transaction types that apply to merchants are:

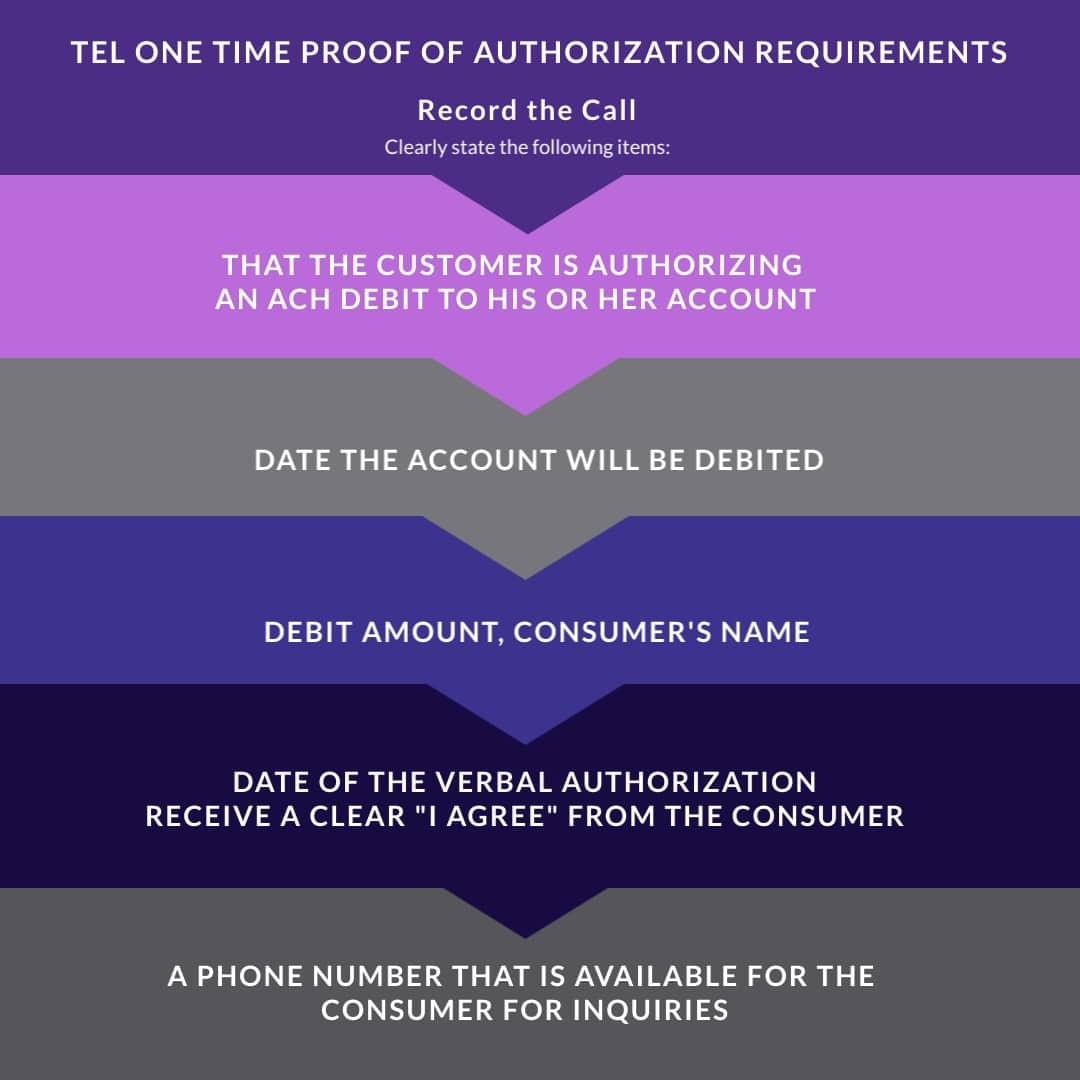

TEL One-Time transaction type

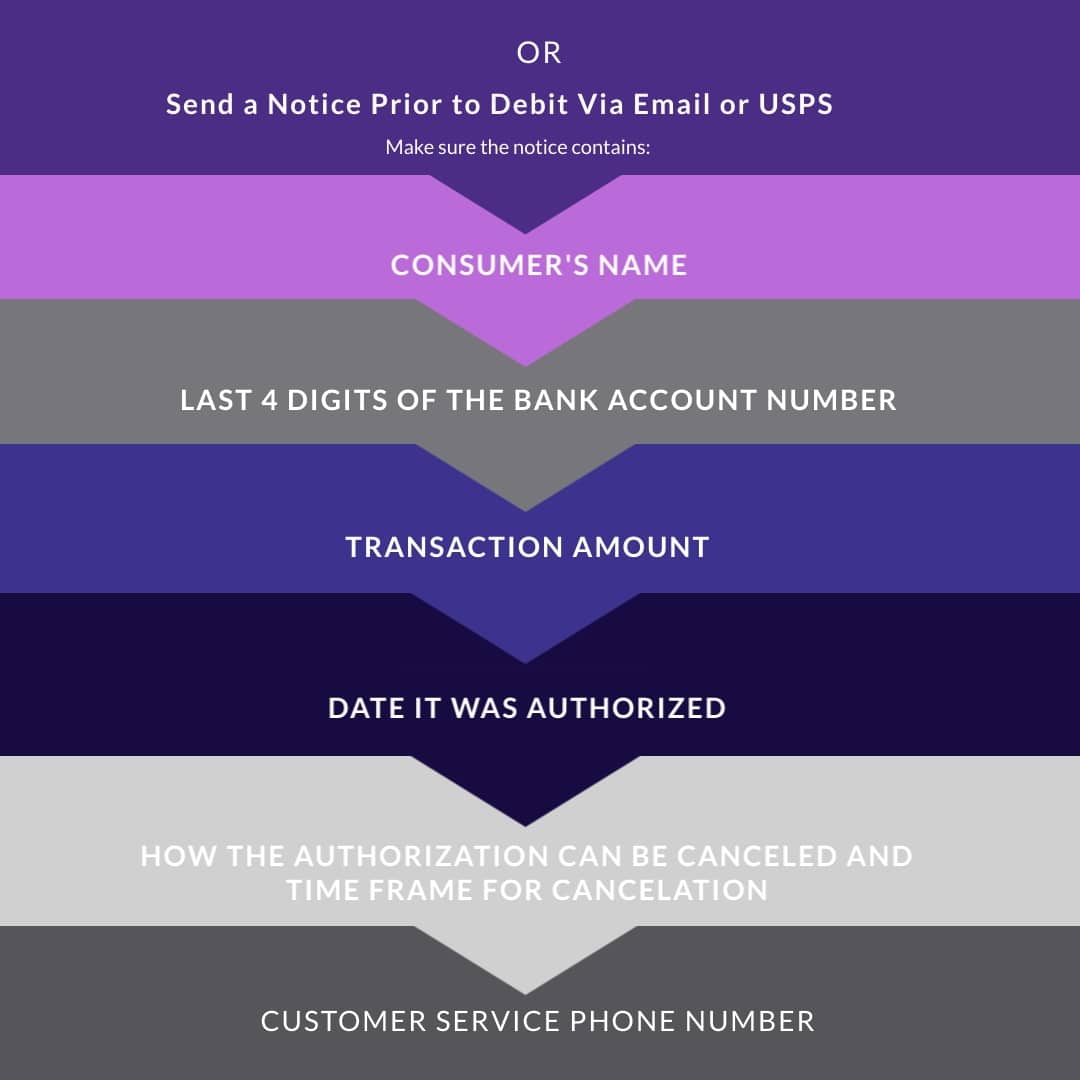

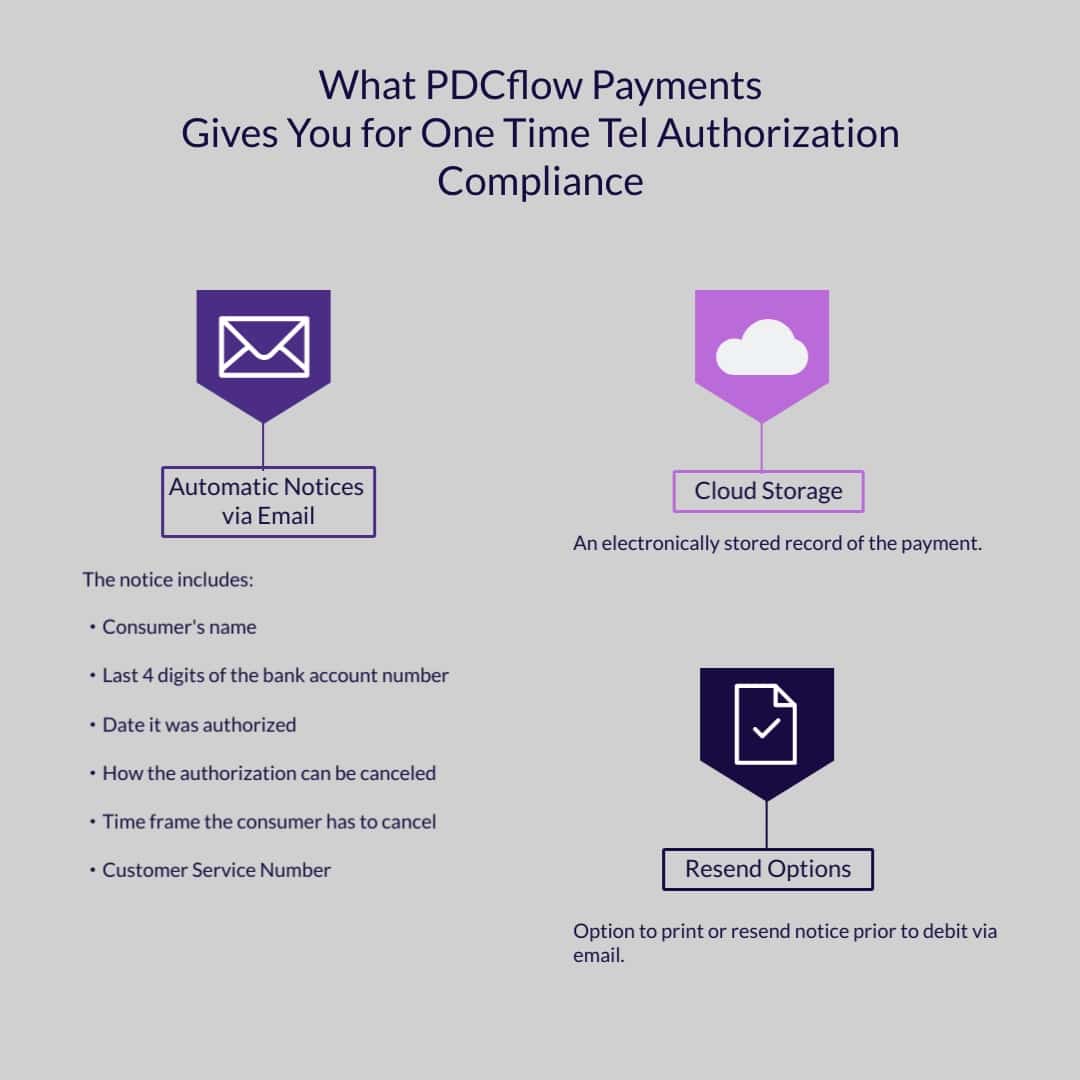

Telephone initiated (TEL) transaction is a single entry (one-time) transaction to a consumer’s account based on the authorization obtained verbally from the consumer via the telephone. A one-time ACH transaction taken over the phone requires either a notice prior to debit, or a recorded call of the oral authorization.

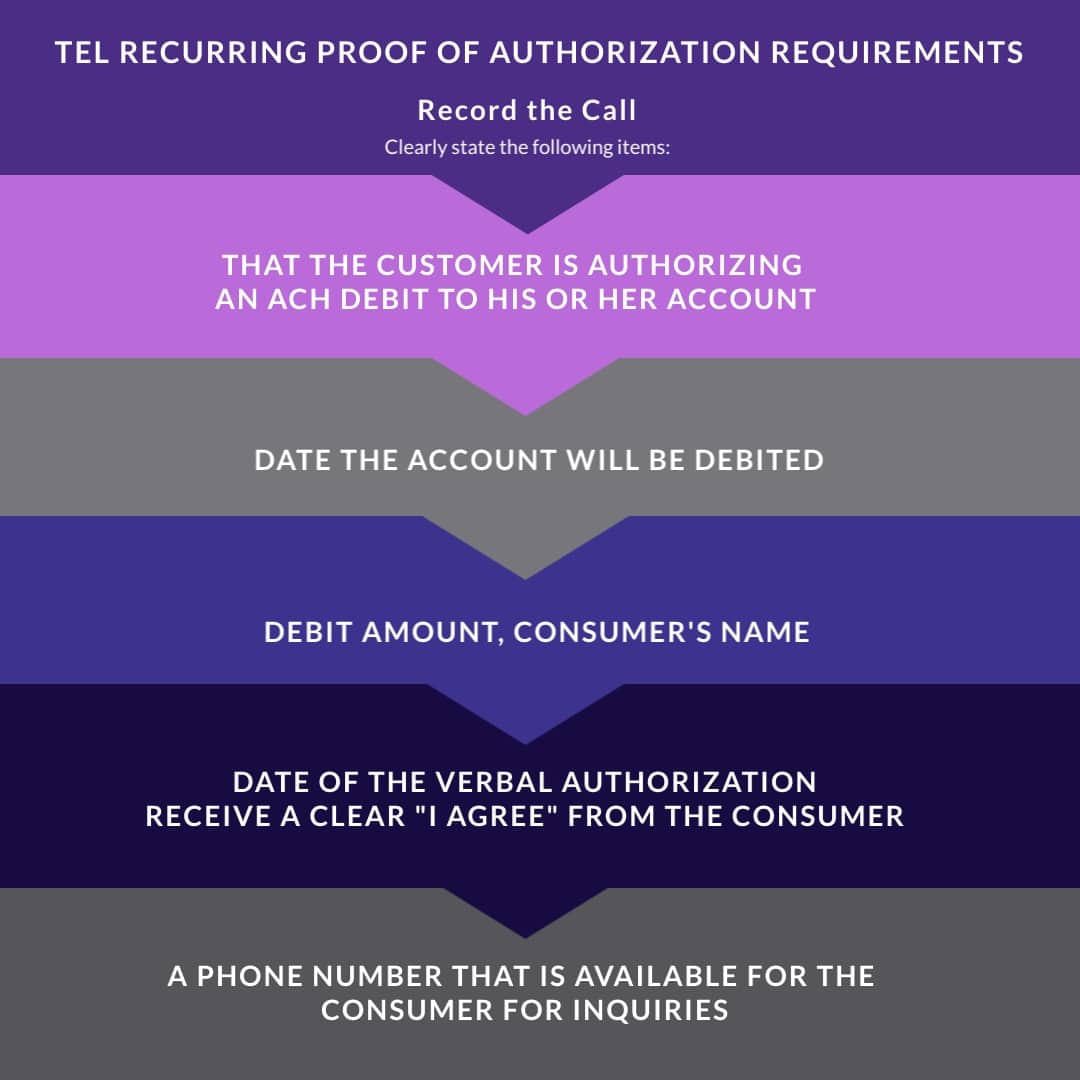

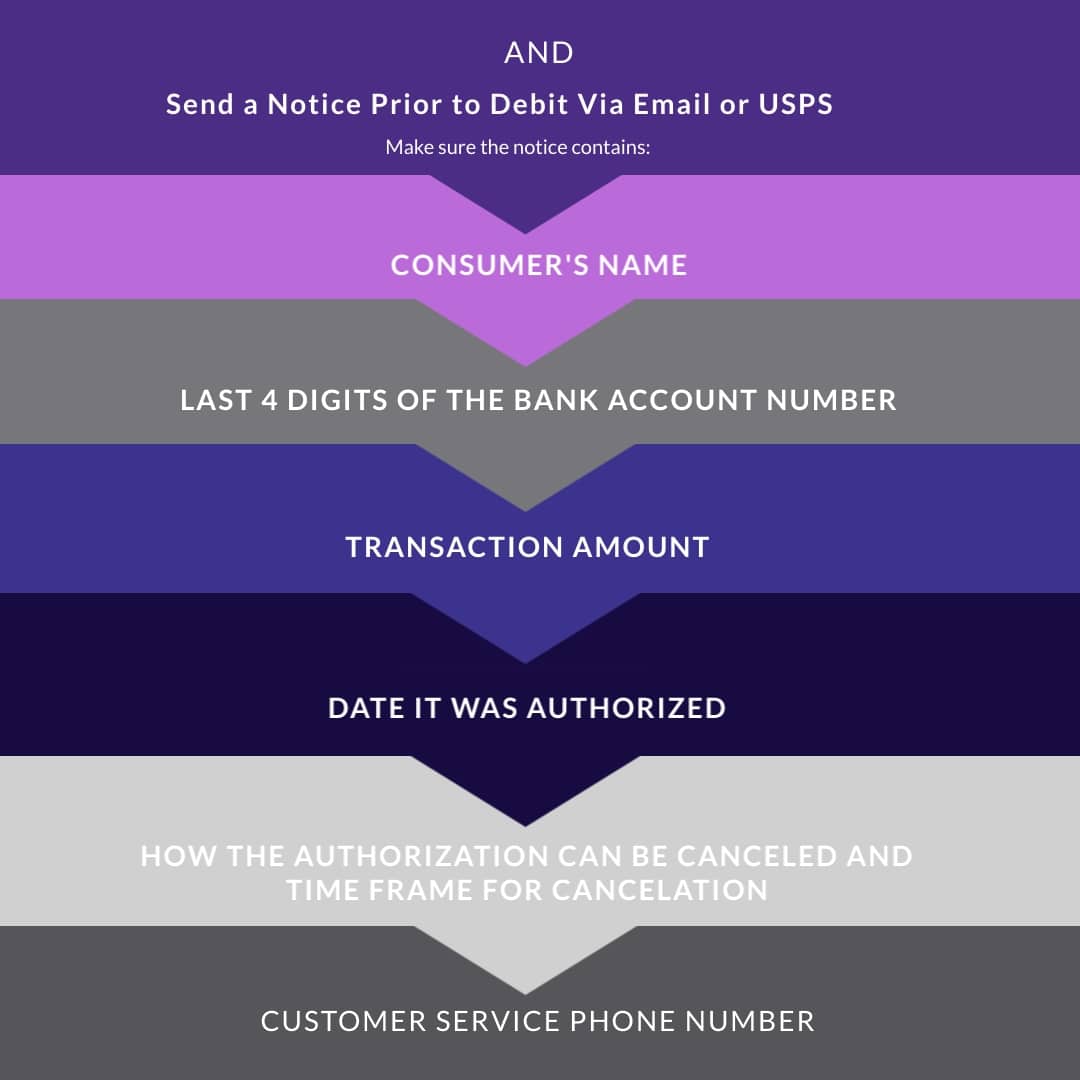

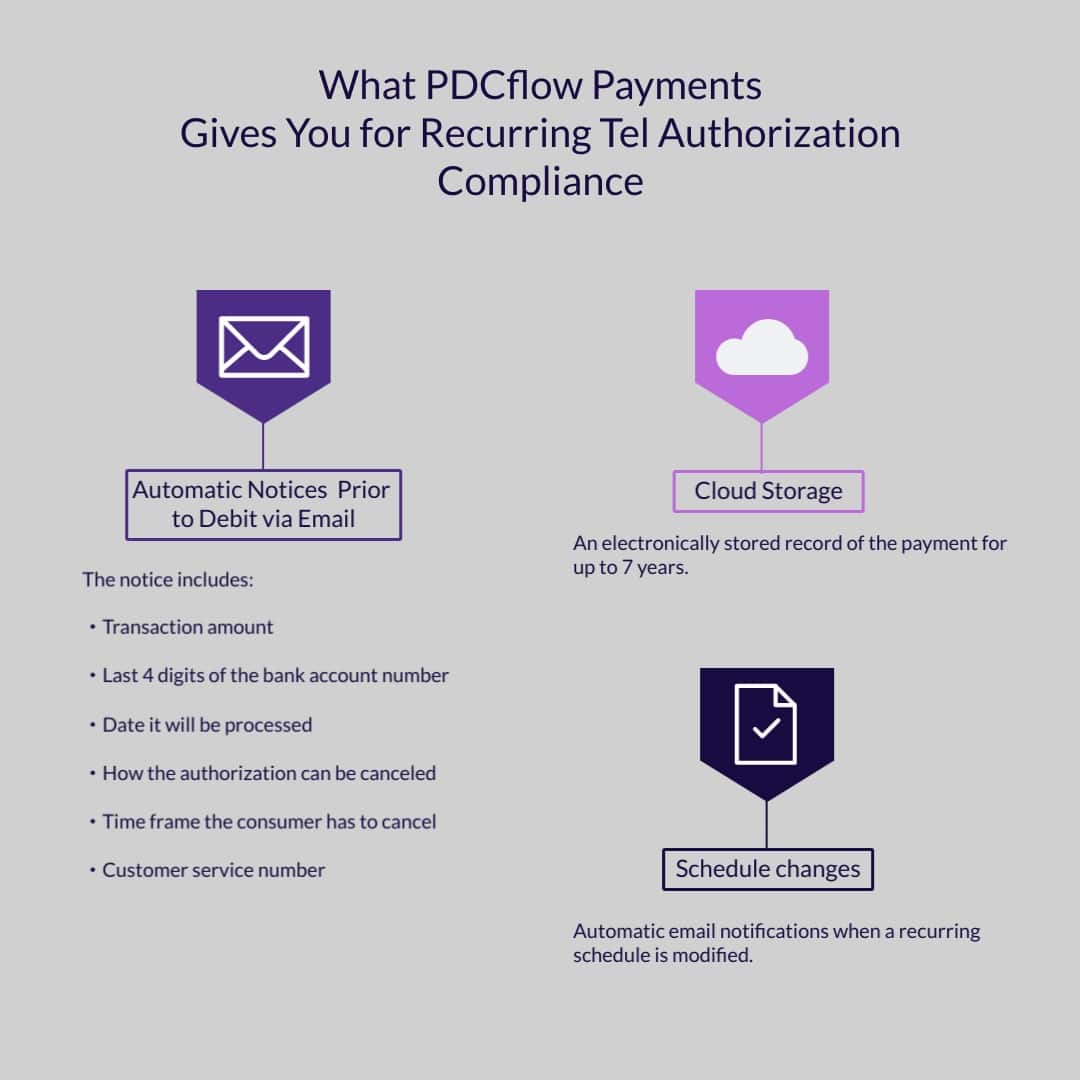

TEL Recurring transaction type

Telephone initiated (TEL) transaction is a recurring transaction to a consumer’s account based on the authorization obtained verbally from the consumer via the telephone. A recurring ACH transaction taken over the phone requires a notice prior to debit AND a recorded call of the oral authorization.

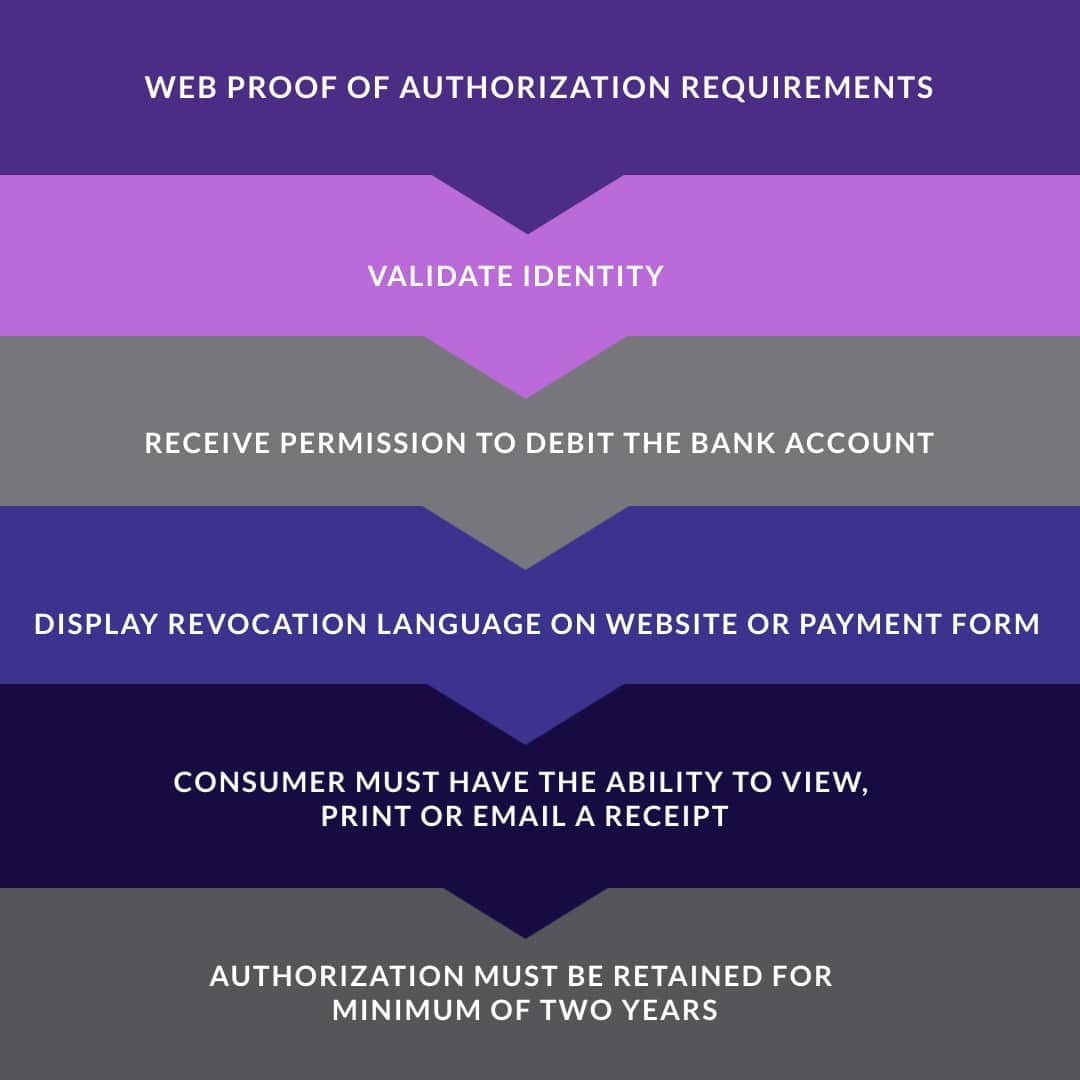

WEB transaction type

One-time or recurring debit transactions where the consumer authorization for the payment was obtained via the internet. Companies that originate WEB debits are required to use a commercially reasonable fraudulent transaction detection system (PDCflow offers ACH Verify services for this.)

An ACH processed via a website requires input that validates the consumer’s identity, must provide evidence of permission to debit and must display Revocation language.

PPD transaction type

Prearranged Payment and Deposit Entry (PPD) is by definition a single or recurring credit or debit transaction initiated by a business that grants permission to debit a consumer’s personal checking or savings account. An ACH processed as a PPD, a post dated or recurring ACH payment schedule set up in person, requires a written authorization.

CCD transaction type

A Cash Concentration or Disbursement is a one-time or recurring ACH transaction that debits or credits a business account. A one-time or recurring business-to-business ACH transaction, requires a written authorization or “wet” signature.

How can an ACH return impact my business?

A few returns won’t have a lasting impact on your business. However, too many returns can disrupt the payment services you offer customers and cost your company time and money.

- Impacts to service: if your company exceeds the return rates established by Nacha, your ACH vendor may decide your organization is too big of a risk to work with and revoke your ability to process ACH payments.

- Impacts to the bottom line: every returned transaction costs your company money. Too many returns will start to impact your revenue as you rack up return fees.

ACH return codes

Most companies want to keep their PCI compliance requirements to a minimum. Using a payment processor that limits PCI scope is the best way for businesses to keep their customers safe while minimizing their own risk.

The responsibilities for each PCI compliance level are as follows:

- Level 1 Service Provider or Level 1 Merchant: certification requires an on-site assessment by a qualified security assessor.

- Level 2 - 4 Merchant: certification can be attained by self-assessment via the Self Assessment Questionnaire (SAQ).

Many companies fall under the rules for a level 2 - 4 merchant. However, the simple Self Assessment Questionnaire (SAQ) compliance is only available under a few conditions:

- The merchant has never experienced a data breach.

- The merchant must be using a Level 1 certified payment processor (like PDCflow).

- The merchant must process fewer than 6 million transactions per year.

When an ACH payment is returned, it comes with a corresponding ACH transaction code to explain what went wrong. There are different types of ACH return codes:

- Ones caused by administrative failures

- Those that apply to your overall return rate

- Those applied to your unauthorized ACH debit entries return rate

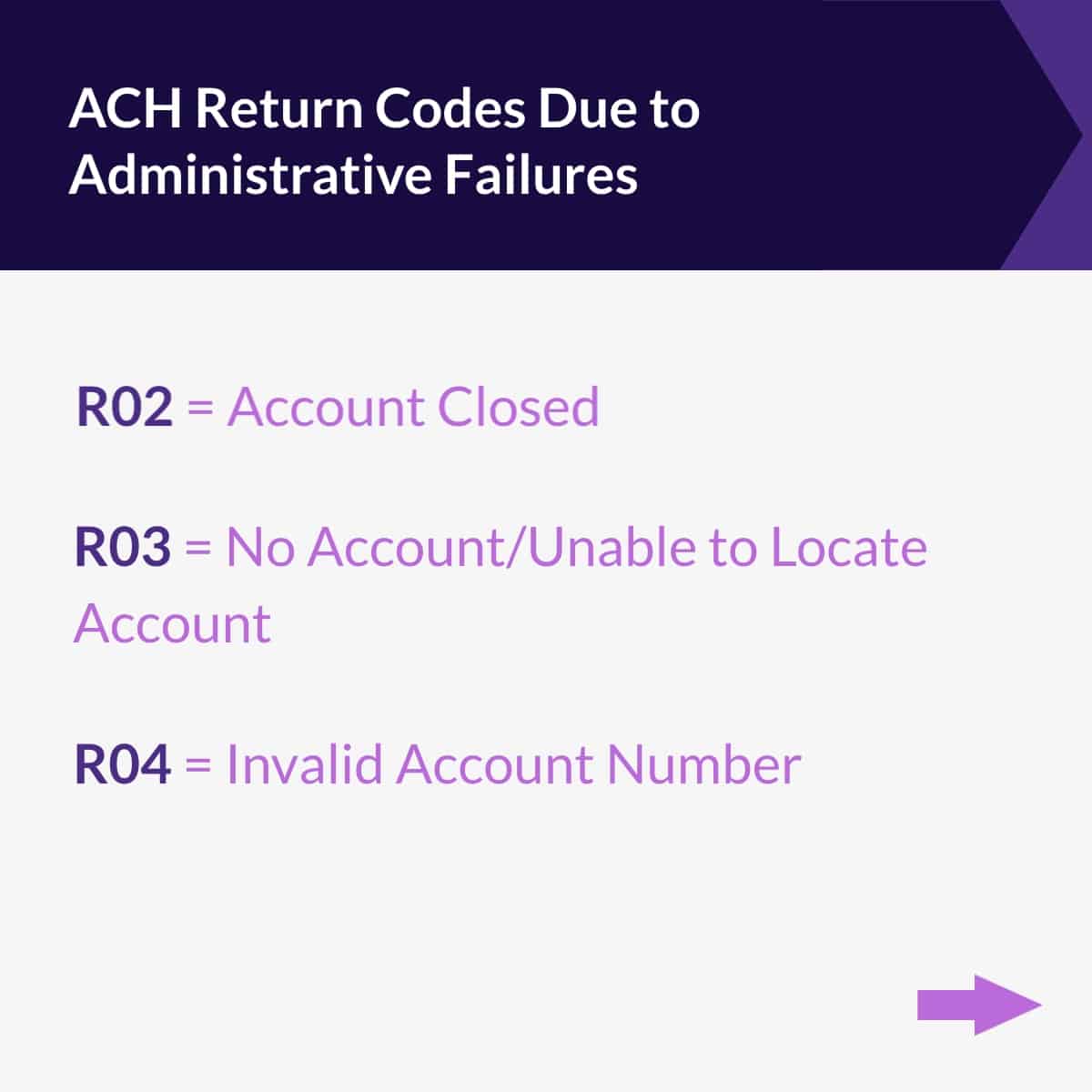

Administrative failure codes

ACH administrative failures usually occur when there is a problem with the account number used to make a payment. The most common administrative codes an organization will see are:

- R02: Account Closed

- R03: No Account/Unable to Locate Account - Name on banking information doesn’t match customer name or account number doesn’t match an open account.

- R04: Invalid Account Number - Bank account information is incorrect (ex: wrong number of digits)

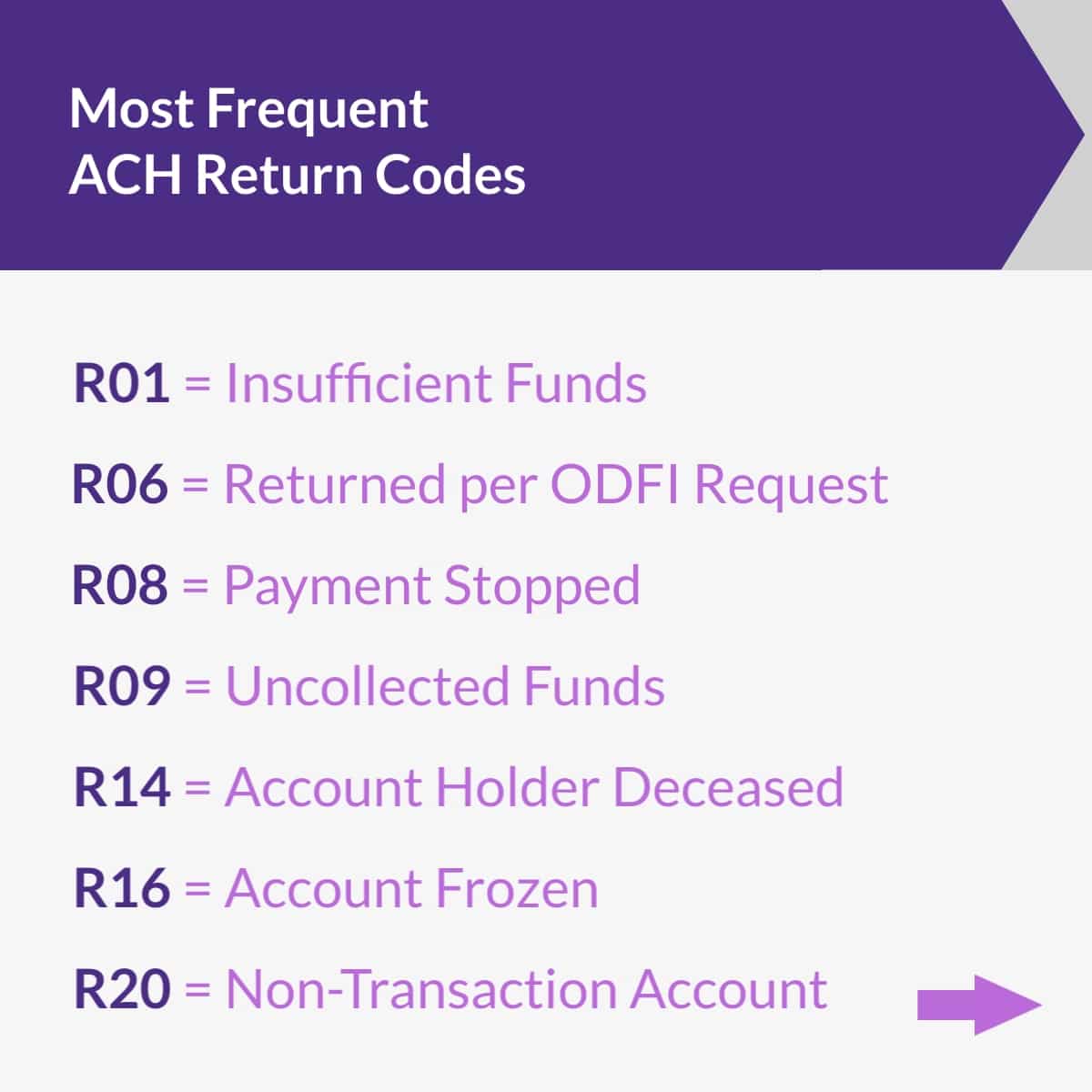

Overall return rate codes

Every returned payment will count towards your overall ACH return rate. The codes below are the most common reasons an ACH payment is typically returned.

- R01: Insufficient Funds - Not enough funds in an account to cover the transaction.

- R06: Returned per ODFI Request - ODFI requested RDFI return the ACH entry.

- R08: Payment Stopped - Receiver of a recurring debit transaction stopped payment on a debit. May indicate authorization for payments has been revoked.

- R09: Uncollected Funds - Money in account is not yet available to use for a transaction.

- R14: Account Holder Deceased - Account holder is deceased.

- R1: Account Frozen - Funds not available due to RDFI or legal action.

- R20: Non-Transaction Account - Account provided is not set up for transactions, transaction type an account can perform isn’t the type being submitted (ex: using savings account instead of checking).

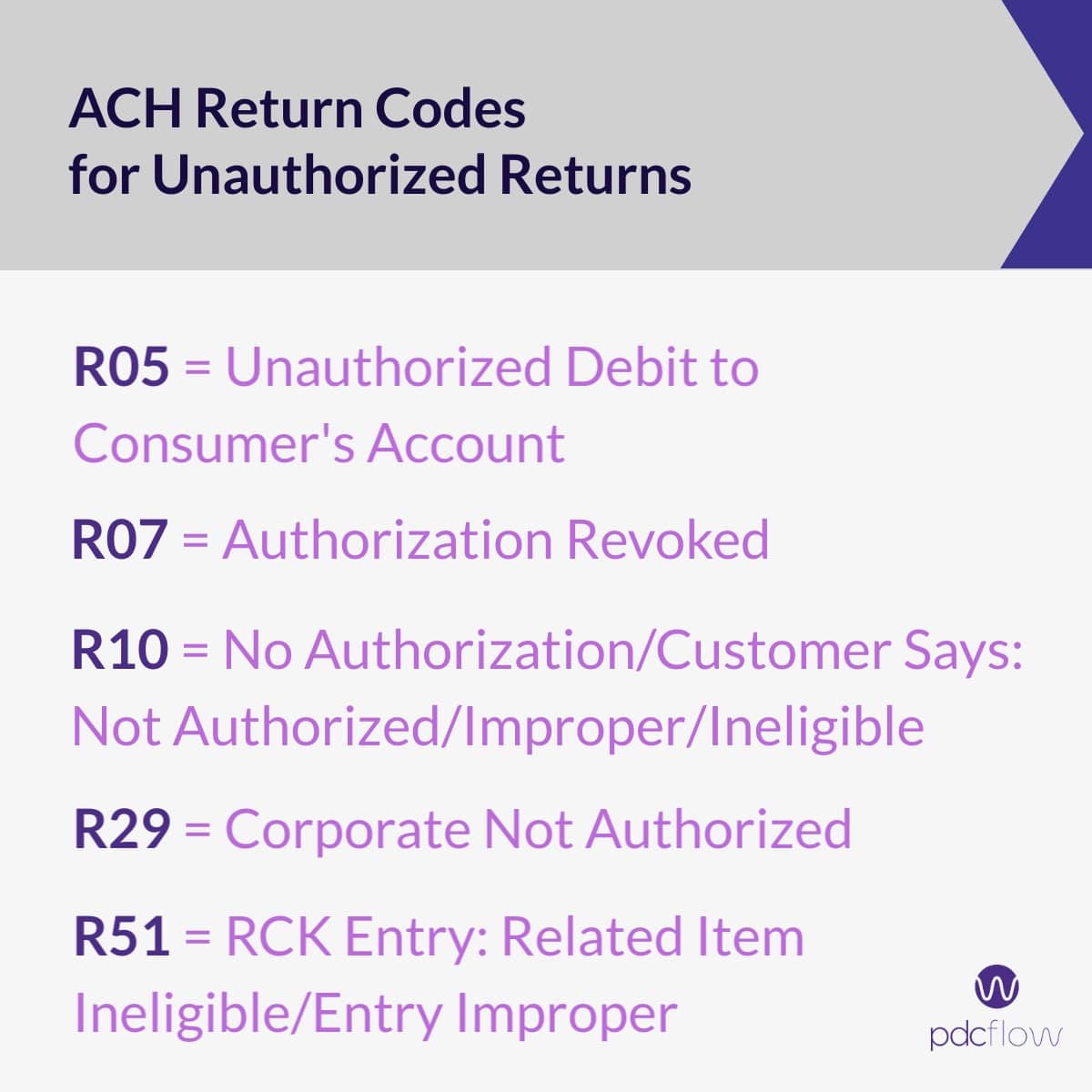

Unauthorized debit entries return rate

Unauthorized debit entries are blocked payments. These types of returned payments are considered chargebacks and usually cost your business the most in return fees.

- R05: Unauthorized Debit to Consumer's Account - Account number structure not valid. The debit presented used a Corporate SEC code.

- R07: Authorization Revoked - ACH debit authorization has been revoked. Funds must be returned no later than 60 days from settlement date and the customer must sign an affidavit.

- R10: No Authorization/Customer Says: Not Authorized/Improper/Ineligible - Consumer advised RDFI the originator of a transaction is not authorized to debit the account. Funds must be returned no later than 60 days from the settlement date of original entry and the customer must sign an affidavit.

- R29: Corporate Not Authorized - RDFI has been notified by the receiver (non-consumer) an entry wasn’t authorized.

- R51: RCK Entry: Related Item Ineligible/Entry Improper - Item is ineligible, notice not provided, signatures not genuine, item altered or amount of re-presented check entry (RCK entry) not accurately obtained from the item.

What to do when you experience ACH returns

If your company experiences too many returns – especially those that count as chargebacks – you should make adjustments to your practices that reduce the likelihood of future returns. Here are some things to consider:

- Customers often dispute a charge if they don’t recognize where it’s from. Your company’s bank statement descriptor should match your business name, so customers don’t dispute an ACH transaction in error.

- Your staff should also inform customers of how your descriptor will appear on their statement during every transaction.

- Your payment receipts and other communications should include a customer service number and your business name. This will make it easier to address customer concerns internally instead of receiving a returned payment.

- Ensure your customer service line is reliable. Answer calls promptly and have a clear voicemail message for when representatives aren’t available.

ACH transaction compliance and security

Nacha

As mentioned, Nacha is the main rulemaking body over ACH transactions. They create guidelines for ACH transactions, so EFT payments remain secure. As technology changes, rules will continue to be updated.

You should have a good relationship with your payment software vendor so you can rely on them to stay in compliance, even as the ACH rules change.

The Electronic Funds Transfer Act and Regulation E

Regulation E is part of the Electronic Funds Transfer Act that outlines the government expectations for how to manage electronic funds transfers.

Among other requirements, Regulation E states that an organization must obtain authorization before charging recurring payments, offer receipts to anyone who has made an EFT payment and renew consent any time a change is made to a recurring payment schedule.

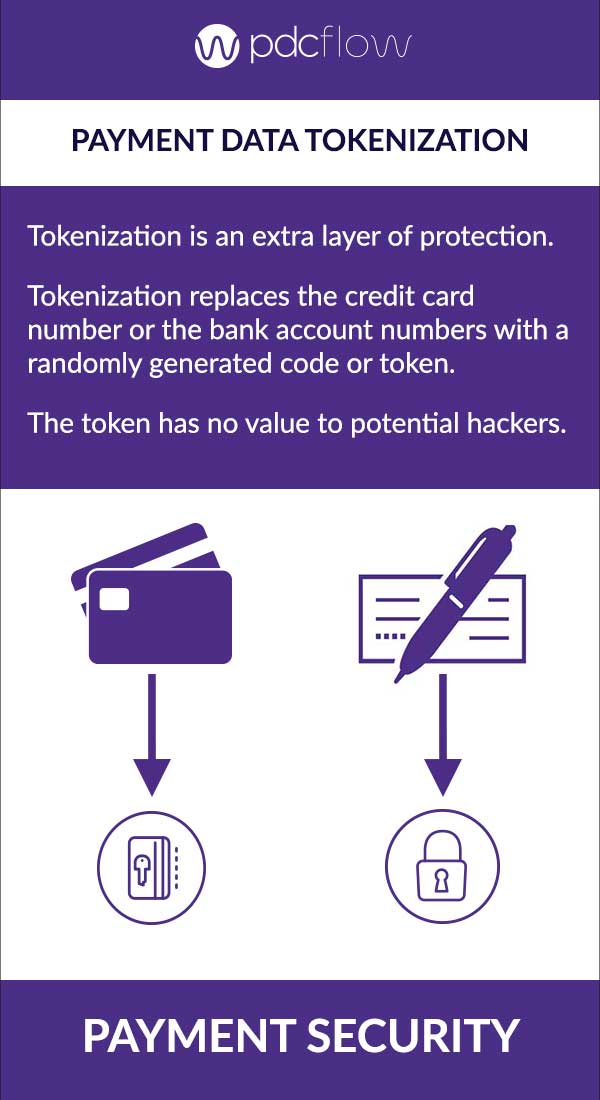

Encryption and tokenization

Encryption is a common practice that scrambles digital information. Payment software should encrypt all customer payment data both in transit and at rest.

Tokenization is similar to encryption, in that it masks important payment data from being seen and stolen. A token is a random placeholder created to represent the real bank account information your customers provide.

ACH payment reconciliation

Once funds are in your account, it’s important to make sure every payment went through. This is sometimes hard to do with ACH transactions because many payments can show up in your account together as a single deposit of money.

Reconciliation can seem intimidating, but luckily, with the right tools and knowledge about ACH batching, the process becomes a lot simpler. Best practices for easy reconciliation:

Know your batch closing time

ACH transactions are not submitted one-by-one. Instead, all ACH payments processed in a day are added to a batch and submitted all at the same time.

If your company takes an ACH payment after your batch has been submitted for the day, that transaction will be included in the next day’s batch.

If you don’t know what time your ACH batch closes, it will be difficult to sort out what day money will end up in your merchant account.

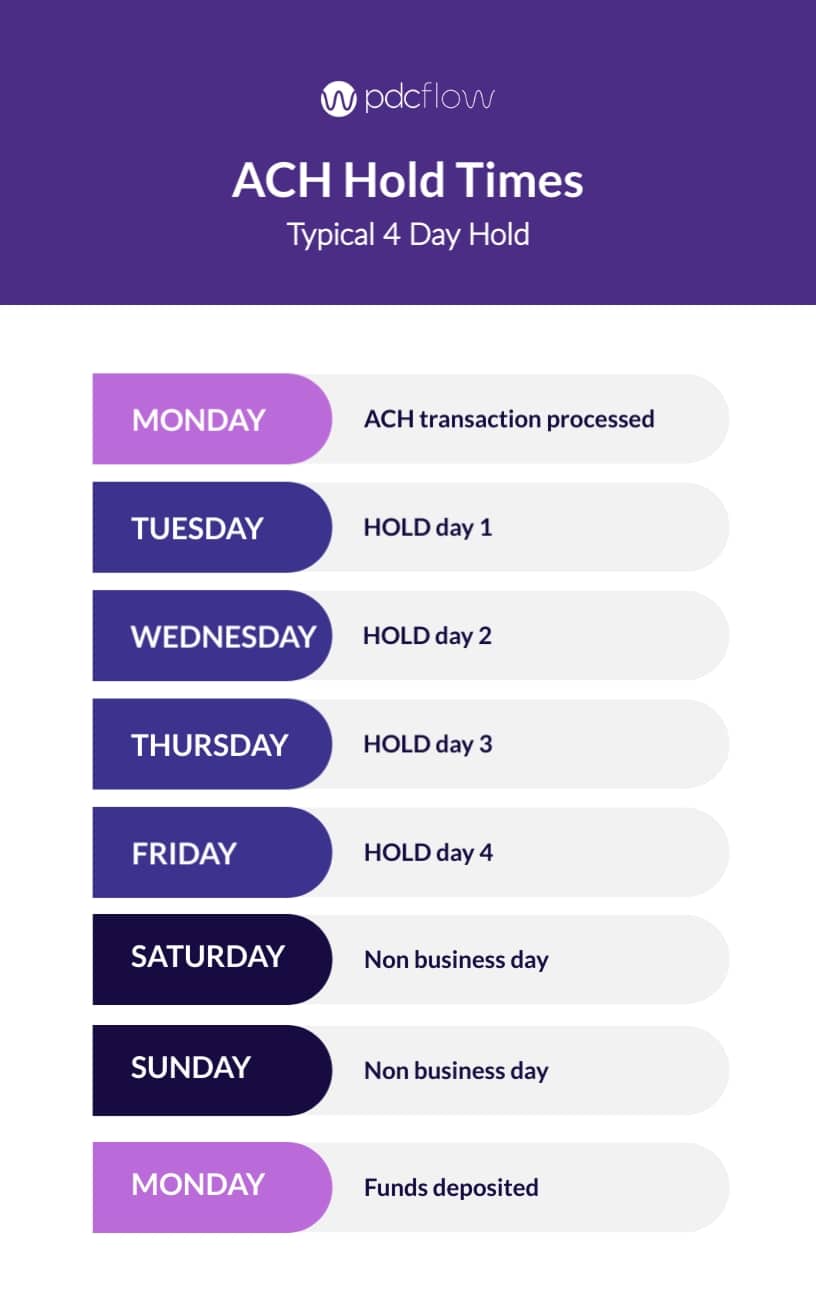

Understand hold times

It takes a typical ACH payment four business days to be processed. Factors like batch closing times, weekend days or federal holidays impact when funds actually end up in your account. For example:

1) Your company takes an ACH payment on a Monday before the ACH batch is sent for processing.

2) The first hold day for that payment begins the next morning, Tuesday, and the hold period ends Friday of the same week.

3) Because Saturday and Sunday are not business days, the funds will not be released until the next business day – the following Monday.

4) If a federal holiday is held on a weekday, no processing will take place until the next business day, which will delay funds an extra day.

5) If a payment is taken on a Monday after the batch has already closed, the payment will be included in the next business day’s batch, which will delay funds an extra day.

ACH vendors sometimes offer shorter funding periods (usually 2-3 days), depending on how much risk the business poses. A company’s hold time is typically established during underwriting or shortly after.

Read your failed payment reports

Before reconciliation, it’s important to know which payments did not go through. Your payment processing software should offer a report that lists all failed ACH payments (also referred to as an exception report) for any given batch.

Without checking your exceptions, ACH reconciliation may become hard (or even impossible) because the funds you expect to receive will not match the balance in your merchant account.

Understand authorized vs. unauthorized returns

Payments can be returned for any number of reasons. Common causes – like insufficient funds in a customer’s account – are detected during a hold period. These returns prevent funds from ever reaching the company’s bank account.

However, there are times that an ACH return will not be discovered until funds have already reached the merchant’s account. In the case of these unauthorized returns, money will have to be debited from the company and given back to the consumer.

These unauthorized returns are yet another complication when reconciling your account. For the easiest reconciliation possible, follow best practices for preventing unauthorized returns:

- Make sure your company name is clearly listed on bank statements and receipts, so customers aren’t confused later about what the payment was for.

- Require dual entry (typing the account number twice) when entering bank account numbers This prevents staff and customers from accidentally typing the wrong account number during payment.

- Create a solid procedure for gathering payment authorizations, so there is no doubt your customers approve of the payments you are submitting.

Processing ACH transactions: final thoughts

ACH payments are part of a multi channel payment strategy and can help your business reach a wider customer base. Digital payments are becoming more popular each year and a variety of payment options is essential to serving all types of customers.

PDCflow makes it simple to set up ACH processing to your payment offerings. With ACH payments through PDCflow, you get:

- Help getting started - PDCflow’s payment experts can put you in touch with an ACH payment vendor to apply for an ACH merchant account.

- Compliance - Our software offers Regulation E and Nacha compliance features, like automated receipts for customers and ACH account verification.

- Security - PDCflow encrypts and tokenizes bank account details to keep payments secure.

- Reporting - PDCflow’s exception report tells merchants which ACH transactions have been returned, so it’s easy to reconcile.

For more information on PDCflow’s ACH payment processing and other payment communication features, request a meeting with a payment expert today.