Electronic Funds Transfer

Authorization Requirements Guide

With the introduction of online payments, digital wallets, and other new payment technology, electronic funds transfers (EFTs) are becoming more popular than ever with consumers and businesses (for both making and taking B2B payments). EFTs are gaining traction because:

- They are better for business - companies that operate without a physical location can easily serve customers and take payments.

- Typically don’t require fees for customers to use - customers that don’t like paying a fee to use a credit card often opt for eft transfers instead.

What are Electronic Fund Transfer (EFT) Transactions?

Any time money is moved through electronic means instead of a paper-based transaction, this is considered an electronic funds transfer.

Online self-serve transactions aren’t the only type of payment classified as an EFT. Payments made through any digital method (like over the phone) qualify as electronic payments. Some of the most relevant examples of types of EFT payments for merchants are:

- ACH payments

- Wire transfers

- Bank card (debit card) payments

- Phone system payments

- Electronic wallet payments

What is the Electronic Fund Transfer Act?

The Electronic Fund Transfer Act (EFTA) is an act signed into US law during the Carter administration. It was created to outline what protections consumers should have during an electronic fund transfer.

Regulation E is the regulation that implements the EFTA. It gives financial institutions specific rules to follow to make sure they are protecting consumer information during electronic transactions.

Electronic Fund Transfer Act Explained

What Does Regulation E Require?

What is a Pre Authorized Electronic Fund Transfer?

It is an:

1. Electronic Funds Transfer

2. That is Authorized in Advance

3. That is Recurring or Repeated

4. At Regular Intervals

A merchant’s responsibility when setting up a payment schedule is to:

- Authenticate the consumer

- Provide them with a copy of the authorization

- Be able to prove the consumer consented to the payments

What is a Legal Wet Signature?

When talking about gathering a signature from a customer, it’s common to require a legal wet signature. But what is a legal wet signature? It is a signature physically generated by the person signing.

This can be gathered traditionally through ink on paper, at a Point of Sales (POS) machine with an electronic pad and stylus, or even through an email or SMS request through software like PDCflow’s Flow Technology (signed with a finger on a touchscreen, or using a mouse or stylus).

EFT vs. ACH

What is the difference between an EFT and an ACH payment? While EFTs represent a wide variety of electronic payments, ACH payments are a specific type of EFT.

They are the transfer of money between bank accounts that involve electronic means rather than, for example, using a paper check. ACH payments apply to Regulation E and must adhere to the requirements the Electronic Funds Transfer Act (EFTA) outlines.

ACH payments are one of the most popular types of electronic fund transfers companies use. Merchants need to know how to comply with both electronic funds transfer regulations and ACH payment compliance rules created and enforced by Nacha.

What is Nacha?

One area of concentration for Nacha is keeping the number of disputed ACH payments to a minimum. This keeps the payment network reliable and holds businesses accountable to customers. According to Nacha, returned payment thresholds for merchants must not exceed:

- Overall return rate - 15 percent

- Administrative return rate - 3 percent

- Unauthorized return rate - 0.5 percent

The rules also state three acceptable reasons a customer may dispute an ACH charge on their account:

- If the charge was never authorized by the account holder or the authorization was revoked.

- If the payment was processed on a date earlier than authorized.

- If the transaction was processed for an amount other than the amount that was authorized.

A consumer disputing an ACH transfer must provide notice to the bank in writing that one of these three conditions exists.

ACH Payment Types

Just as with other types of electronic funds transfer, organizations should authorize ACH transfers ahead of time with consumers. The origin of the transaction will determine its payment type and what method of authorization is acceptable. Payment types include:

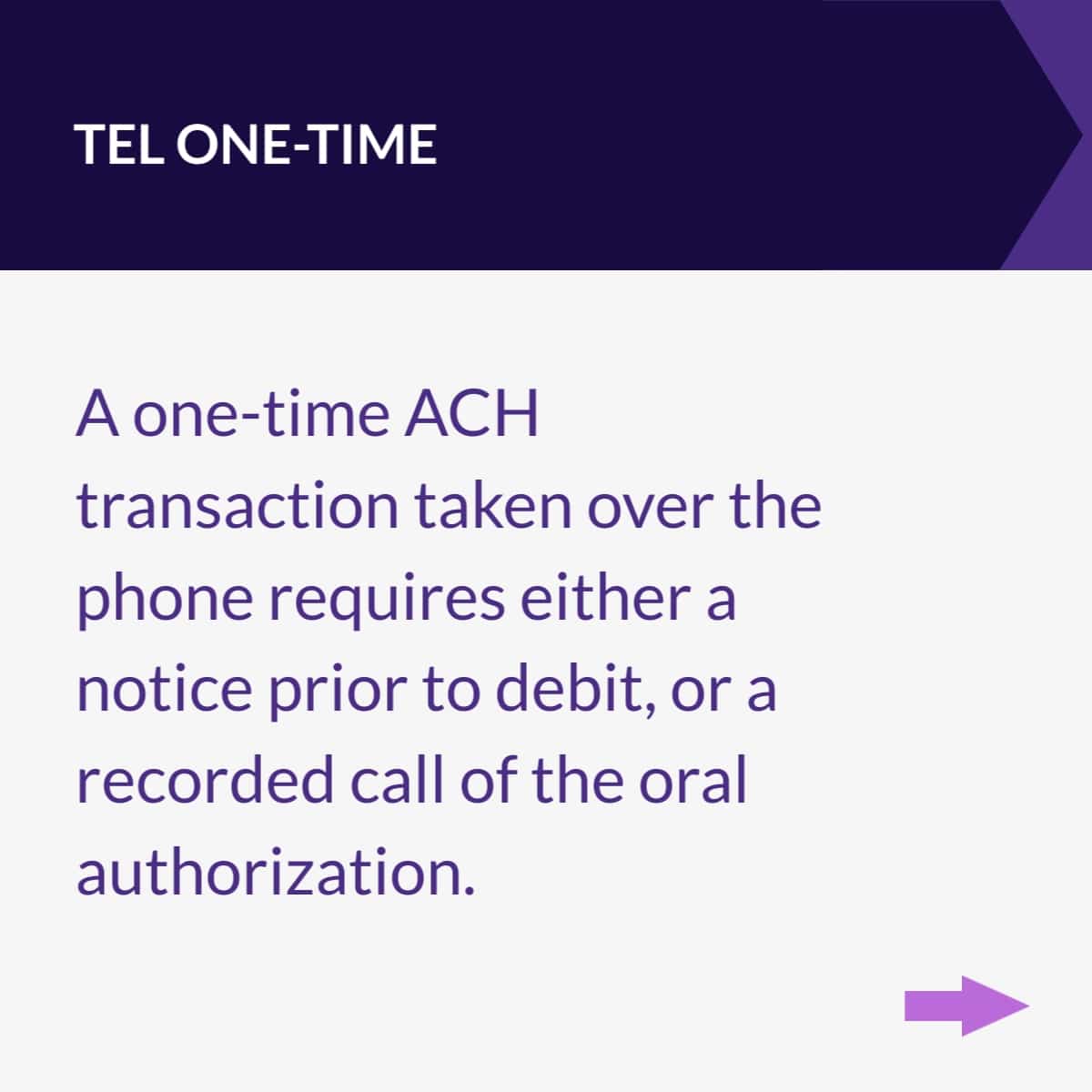

TEL one-time

A telephone initiated (TEL) entry is a one-time transaction to a consumer’s account. The authorization for a one-time TEL payment is obtained verbally over the telephone.

TEL recurring

Telephone initiated (TEL) recurring transactions are a schedule of repeating transactions to a consumer’s account. The authorization for recurring TEL payments is obtained verbally over the telephone.

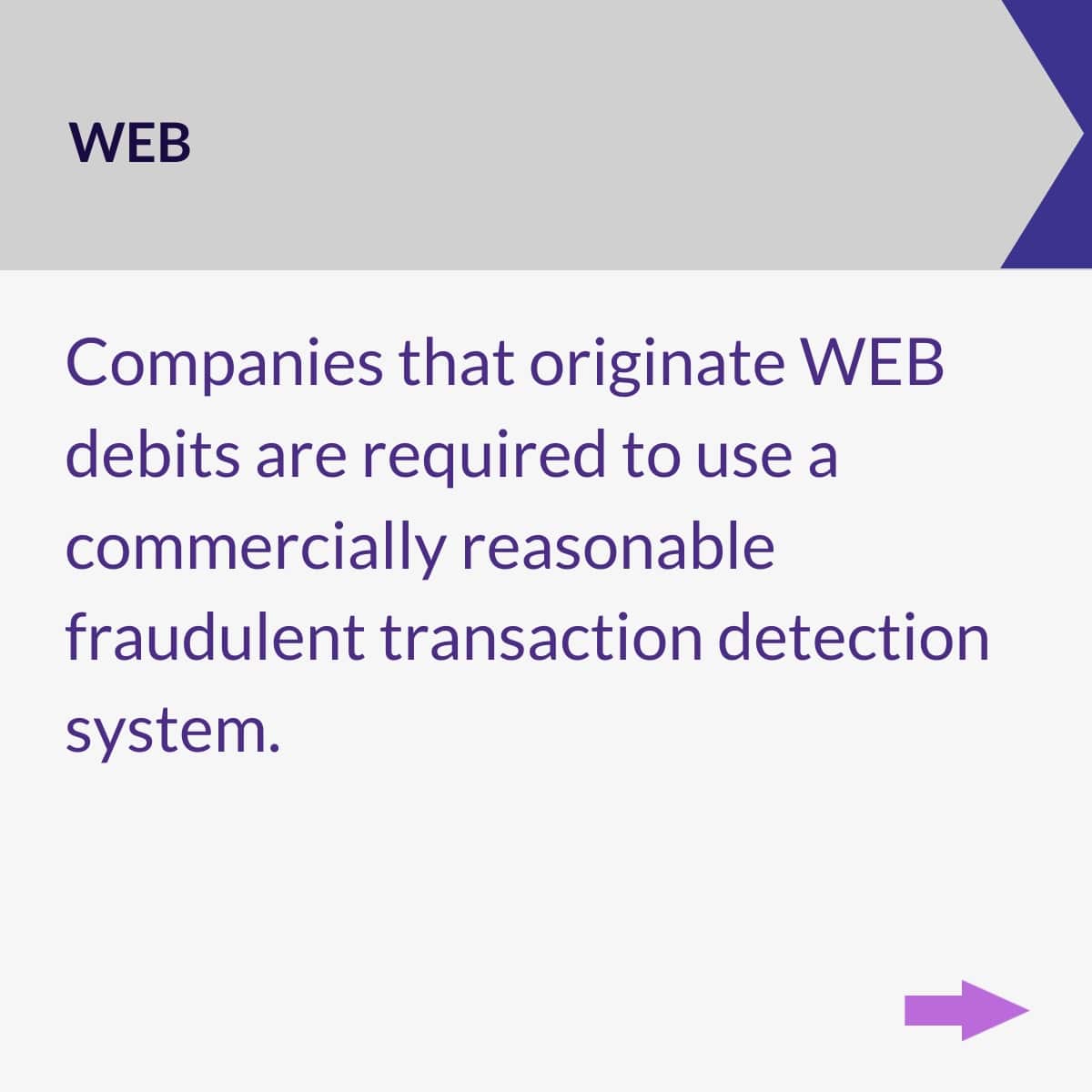

WEB

A one-time or recurring debit transaction that takes place online (for example, through an online self-serve payment page). The payment authorization for this transaction type is obtained via the internet.

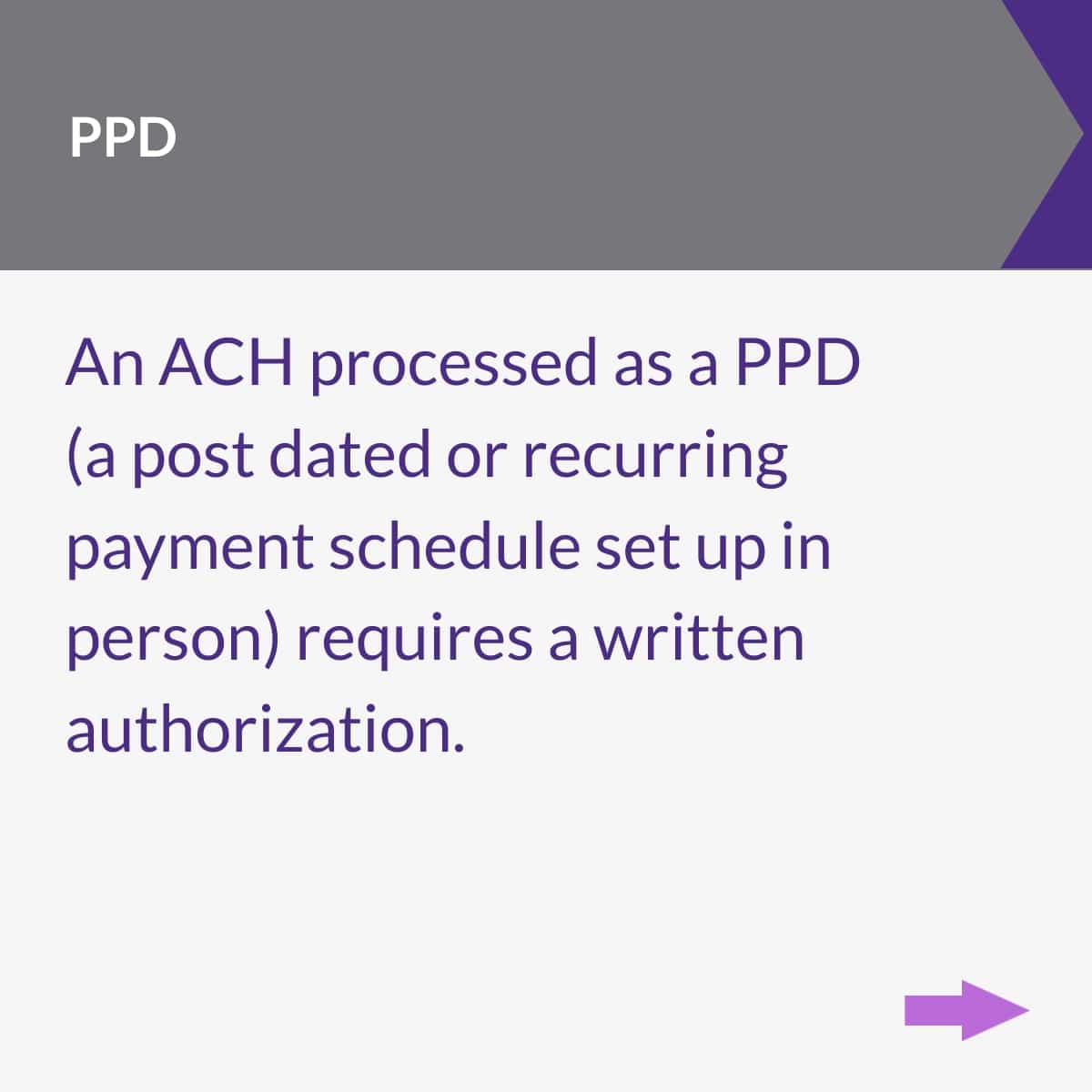

PPD

A prearranged Payment and Deposit Entry (PPD) is a single or recurring credit or debit transaction initiated by a business. A PPD authorization grants permission to debit a consumer’s personal checking or savings account.

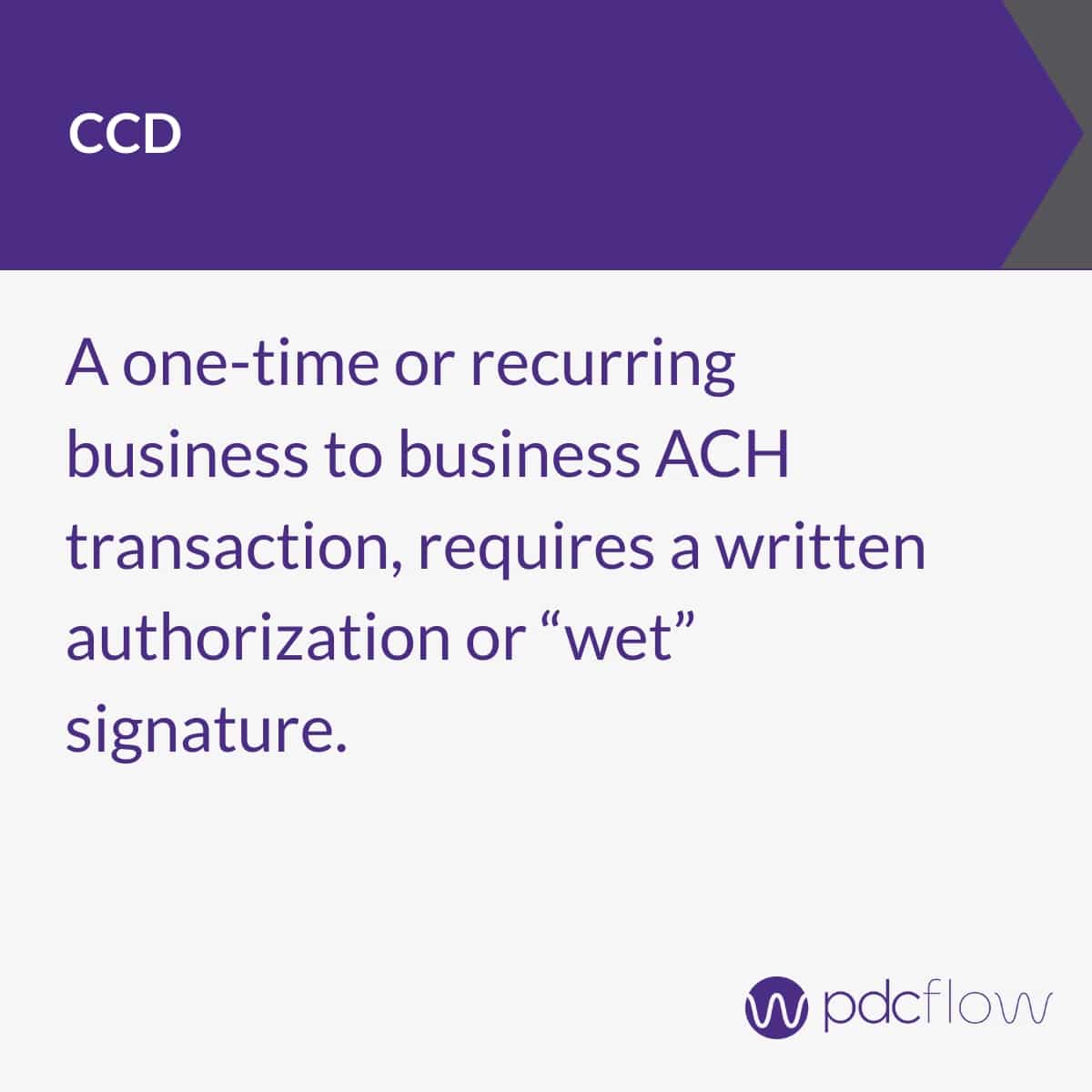

CCD

A Cash Concentration or Disbursement is a one-time or recurring ACH transaction that debits or credits a business account.

Occasionally, your ACH payment vendors may check to make sure a merchant is following these authorization guidelines correctly. Companies should be prepared to offer proof the customer consented to the payment (called a proof of authorization) at any time.

Authorization Requirements for Electronic Funds Transfers Through the ACH Network

TEL Transaction Authorization Guide

The Electronic Fund Transfer Act Requires

Preauthorized electronic transfers from a consumer's account may only be authorized by the consumer:

1. In writing

2. Signed or similarly authenticated by the consumer

3. Signed, written authorizations may be provided electronically, subject to the E-Sign Act

4. In all cases, the party that obtains the authorization from the consumer must provide a copy to the consumer.

How to Authorize:

1. Record the call and clearly state:

- The consumer is authorizing an ACH debit to his or her account

- The date the consumer’s account will be debited

- The amount of the debit

- The consumer’s name

- The date of the verbal authorization

- A phone number that is available for the consumer for inquiries

You must receive a clear “I agree” from the consumer for the authorization to be valid.

2. Send a notice prior to debit either via email, fax or mail, confirming the authorization and the payment amount. Make sure the notice contains:

- consumer’s name

- last four digits of the bank account number

- transaction amount

- date processed

- how the authorization can be canceled

- time frame a consumer has to cancel the authorization

- phone number the consumer can call to contact your office

You must be able to prove the notice prior to debit was sent, but you are not required to prove it was received.

3. A copy of the recorded oral authorization and/or the notice prior to debit must be retained for a minimum of two years from the date of the authorization.

4. For Recurring TEL transactions, if the amount of the debit entry to the consumer account differs from that of the original authorization, a new written notification of the new amount must be sent to the consumer a minimum of 10 calendar days prior to debit.

5. For Recurring TEL transactions, if the date of the debit entry changes, a written notification of the new date must be sent to the consumer. This must be done a minimum of seven calendar days before the date of the first payment in the updated schedule.

Sample Recorded TEL Authorization Script

Agent: Hello, is this M_________?

Consumer: Yes, this is M_________.

Agent: This is (Agent name) from (business name). Today is (Date) I have to advise you this is a recorded line (and any other compliance language required via your policies and procedures guidelines).

Consumer: Okay.

Agent: The (payment) I am calling on is for the __________________ who have turned over a debt in the amount of $_______________ to our agency for collection. We are calling in an attempt to resolve that.

Consumer: I cannot afford to pay all of that today. Can I make payments?

Agent: Absolutely. A recurring payment schedule can be set up and would work like this: You would agree to provide either checking or credit card information. You would agree to authorize (business name) to withdraw or charge your account with $___________ each month on a day that fits your budget. Will this type of payment arrangement work for you?

Consumer: Yes.

Agent: In that case, how much can you pay, and on which day of the month would you like this set up?

Consumer: I can afford $________ on the _______ of each month.

Agent: Now I will send you the payment schedule details for you to review, sign and enter your credit card or bank account information. What email or mobile number can I send this to?

If you would allow me to repeat your agreement and you could confirm the agreement, please? Today is (Day/Date) and you are agreeing to allow (business name) to withdraw $________ per month on the ______ of every month until you have fulfilled your obligation.

Now, if you could please state your name again and verbally confirm that you agree to the terms that we have discussed.

Consumer: Yes, my name is (Name) and I agree to these terms.

Agent: Please understand that this authorization will remain in full force and effect until you notify us that you wish to revoke this authorization. And we require at least five (5) business days prior notice in order to cancel this authorization. If you have any questions, you may also contact us at (xxx) xxx-xxxx.

WEB Transaction Authorization Guide

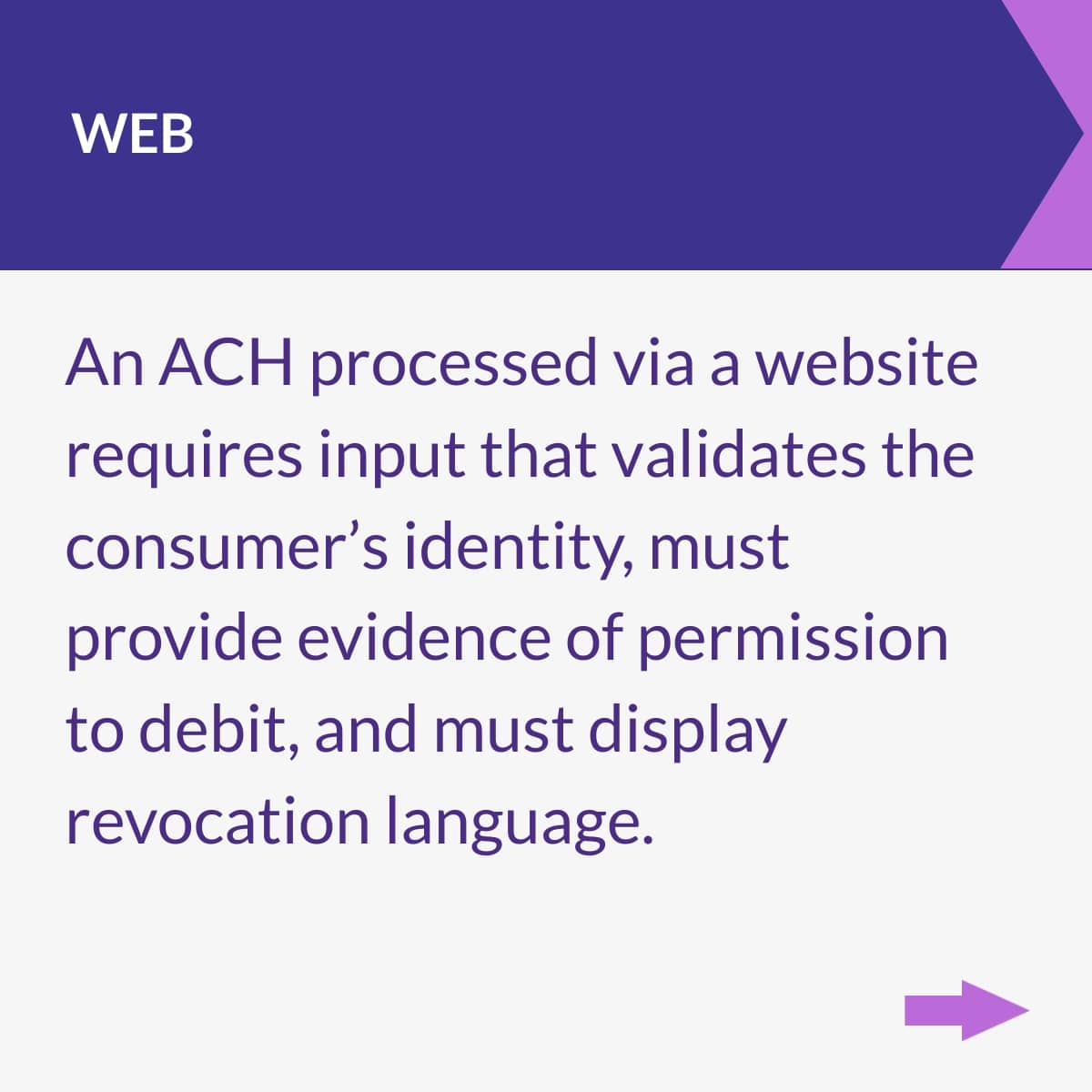

WEB transactions are authorized by a consumer entering payment information into a web form, actively checking a box to agree to the terms and conditions for the transaction, and clicking a “Submit” button.

How to Authorize:

1. Validate the consumer’s identity.

2. Receive permission to debit the bank account.

3. Display Revocation Language on the website or payment form using Nacha mandated language.

4. Give the consumer the ability to view, print or email a receipt.

5. For recurring WEB electronic transfers, if the amount of the debit entry to the consumer account differs from that of the original authorization, send a written notice of the new amount a minimum of 10 calendar days prior to debit.

6. For Recurring WEB electronic transfers, if the date of the debit entry changes, send a written notice of the new date a minimum of seven calendar days before the date of the first changed entry.

7. The authorization along with identity verification must be retained for a minimum of two years.

8. A copy of the authorization must be provided within 10 days if requested by the Originating or Receiving Financial institution.

Sample Revocation Language

PPD Transaction Authorization Guide

PPD transactions are single or recurring debit or credit entries to a consumer account, generally initiated in person.

PPD Recurring Electronic Funds Transfer Definition

Grants permission to debit a consumer’s personal checking or saving account:

1. For the same amount on a regular schedule, such as weekly, bi-weekly or monthly.

2. For different amounts on a regular basis.

3. For a payment plan for the payoff of a large debt.

How to Authorize:

1. Must be in writing.

2. Must be signed or similarly authenticated by the consumer. ‘Similarly authenticated’ allows written authorization to be provided electronically. The authorization must prove both the consumer’s identity and their agreement to the authorization.

3. Must be a legal “wet” signature.

4. Must provide the consumer with an electronic or paper copy of the authorization.

5. Must clearly state terms (amount, date, frequency of payment).

6. Must provide clear cancellation information.

7. Must provide evidence of the consumer's identity and consent to the transaction.

8. Must keep authorization on file for a minimum of 2 years after all payments have been completed.

9. Must send a receipt (mail, email, fax) for each transaction processed as part of the schedule.

10. For recurring PPD electronic transfers, if the amount of the debit differs from the amount stated on the original authorization, a new written notification must be sent to the consumer a minimum of 10 calendar days prior to debit.

11. For recurring PPD electronic transfers, if the date of the debit entry changes, a written notification of the new date must be sent to the consumer a minimum of seven calendar days before the date of the first entry affected by the change.

12. A copy of the authorization must be provided within 10 days if requested by the Originating or Receiving Financial institution.

Sample of Written Authorization

Name of Company _____________________________________________________________________________

CUSTOMER INFORMATION

I (We) hereby authorize Company as shown above, hereinafter called COMPANY, to initiate debit entries to my (our) bank account as detailed below, and to debit the same to such account. Should a transaction be returned, I (we) further authorize debiting this account for non-sufficient fund fees according to applicable State Law. I (we) acknowledge that the origination of ACH transactions to my (our) account must comply with the provisions of U.S. Law.

Full Name on Account: _____________________________________________________________________

Account #: ___________________________________

Routing #: __________________________________

Account Type (select one): □ Checking □ Savings

Account Class (select one): □ Consumer Account □ Business Account

Debit Payment Details: Payment Amount: ________________

Number of payments: _______________

Date of next payment: ________________

Frequency of payments: _______________ (example: one-time, monthly, etc.)

I understand that this authorization is to remain in full force and effect until Company has received written notification from me of its termination at least five (5) business days prior to the payment due date. I further understand that canceling my ACH authorization does not relieve me of the responsibility of paying my account in full and that if I cancel or revoke this authorization before any remaining debt is paid in full, the Company may take additional actions including legal actions to secure the debt.

Customer Signature: ____________________________________________

Date: __________________

Customer Printed Name: _________________________________________

Customer Contact Telephone #:____________________________________

CCD Transaction Authorization Guide

A one-time or recurring ACH transaction that debits or credits a business account.

How to Authorize:

1. Must be in writing (such as a contract between companies).

2. Must be a legal “wet” signature.

3. Must retain a copy of the authorization or agreement/contract for at least two years.

4. A copy of the authorization must be provided within 10 days if requested by the Originating or Receiving Financial institution.

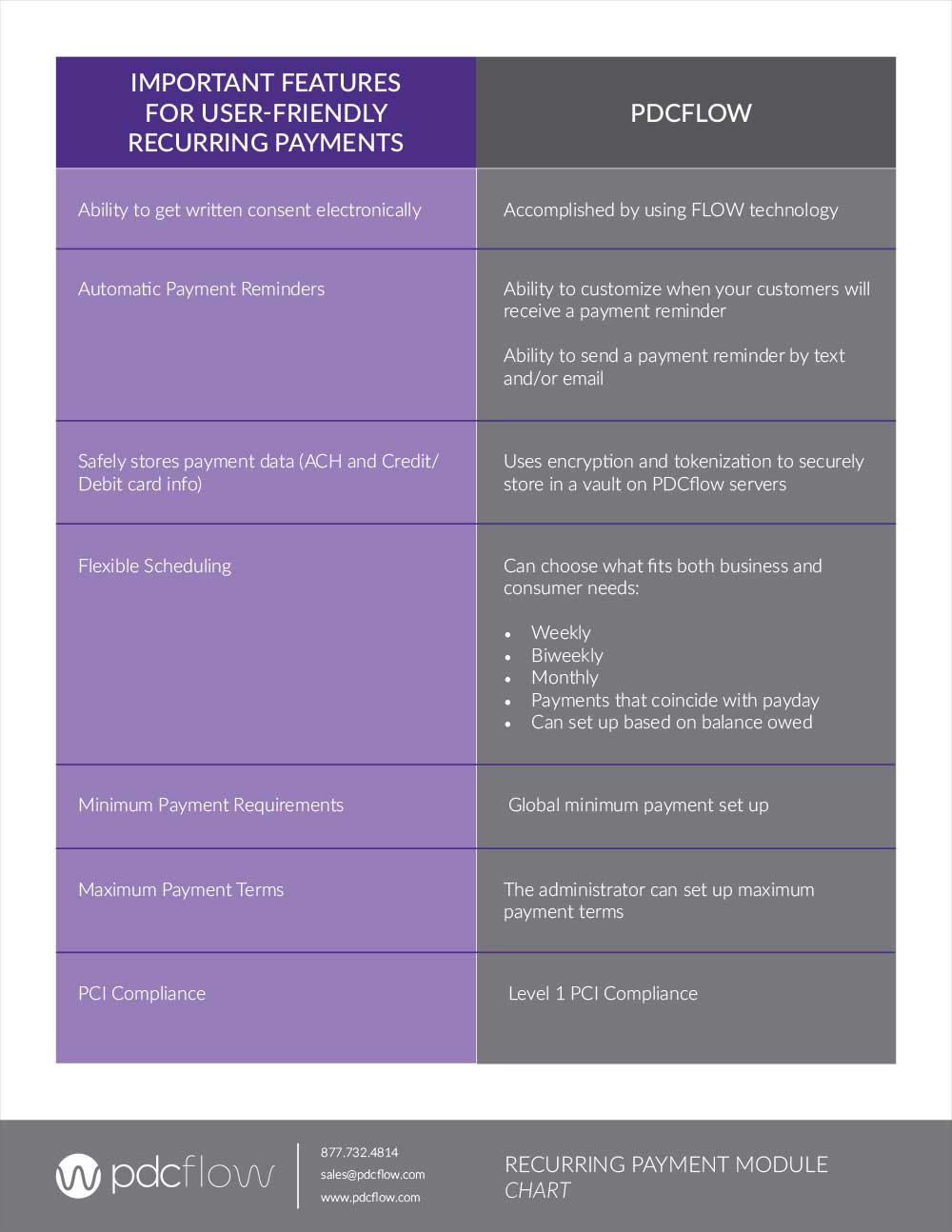

PDCflow for EFTA Compliance and a Better Payment Experience

PDCflow makes Regulation E compliance simple for you, your staff and your customers. With our Flow Technology, you can comply with Regulation E requirements without disrupting your workflow.

Negotiate a Payment Plan

Set up a recurring schedule that works best for you and your consumers. Flexible payment terms mean they can choose the time of month that works best for them, and control the minimum payment amounts they can pay to ensure the plans make sense.

Send Payment Terms Instantly

Send payment schedules, terms and payment consent forms to consumers through text or email. They can authorize the schedule with a legal, wet signature through email or SMS in just a few clicks.

Gain Authorization in Minutes

Ask consumers to authenticate their identity, review the information, sign, enter their payment information (credit card or bank account number) and send back an authorization with a completed payment in a single workflow – all within minutes.

Do you want to learn more about how PDCflow makes it easy to comply with EFT guidelines without complicating your workflows? Schedule a meeting with a PDCflow Payment Expert today.