Being a merchant is expensive. Your mission is to save money or boost profits any way you can. After all, your bottom line is at stake. This concern for the health of your business can drive you toward long-term success.

If you’re wondering whether your own business can charge credit card convenience fees, the short answer is yes. But, there are a few things you need to know to keep your business out of trouble!

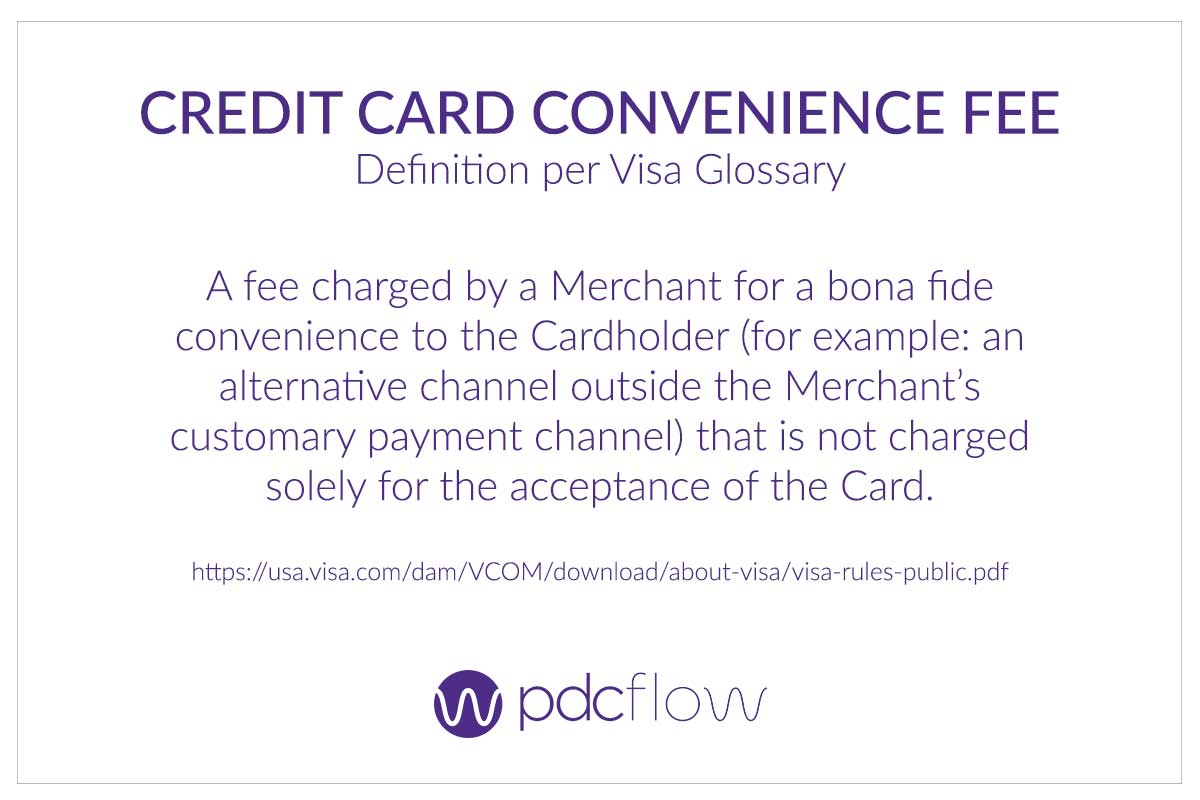

What is a Credit Card Convenience Fee?

A credit card convenience fee is an additional charge to your consumer beside the payment due. It is considered a convenience because your business has provided the consumer another avenue to make a payment (outside of the standard payment channels).

For instance, a card present merchant may accept primarily cash, accepting a credit card can be considered a convenience to the consumer, thus this merchant may be eligible to charge a credit card convenience fee.

For merchants in an exclusively Card Not Present (CNP) environment, charging a credit card convenience fee can’t be done, as it is no longer an added convenience to the consumer. For example, many businesses do accept in-person payments. This may allow them to charge a convenience fee when processing credit cards. If a business made it a policy not to accept in-person payments, however, they would be disqualified from charging a convenience fee.

It is important to remember that other factors also determine whether your business can charge this type of fee. Let’s take a look at some of those rules.

Rules For Charging Credit Card Convenience Fees

As a merchant, you can charge a convenience fee for credit cards under the following circumstances:

- Registration is not required by Visa, but merchants are required to follow card brand rules when charging a credit card convenience fee.

- The fee is indicative of an actual convenience, such as web or telephone payments, and must be charged for every type of payment in that channel. This means that if your business accepts ACH payments as well as credit cards, you must charge a fee for all web and telephone payments, whether they are paid with credit card or ACH.

- The fee cannot be charged to those paying in person (in a card present environment).

- The fee is explained to the cardholder in easily understandable language as a charge for the convenience provided to them.

- The business collecting the payment DOES NOT process exclusively in a Card Not Present (CNP) environment.

- The fee is NOT a percentage of the amount being paid, but rather a fixed amount.

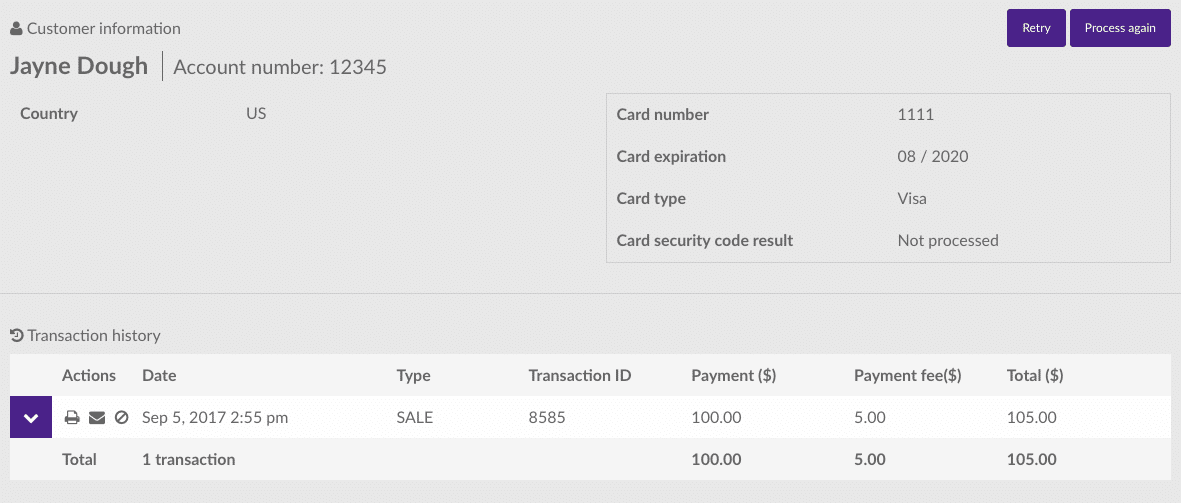

- The fee must be included as part of the total amount or displayed as one transaction.

- The consumers must be told before the time of the payment that they are being charged a convenience fee for using a credit card. They must also be given a chance to cancel the payment and pay another way if they wish.

- A credit card convenience fee may not be charged on recurring payments.

- State or local laws may prohibit businesses from charging a convenience fee on payments. Business owners should consult with their attorney before implementation.

Are the Rules Different for Each Credit Card Company?

Special Considerations For Collection Agencies

Because many consumers pay their bills in installments through recurring transactions, subscriptions, or monthly auto deduct, these business types should remember that according to Visa’s rules, convenience fees cannot be charged to recurring payments in a schedule.

Oftentimes, businesses collect in states outside their state of operation. Charging of credit card convenience fees may be acceptable where you are headquartered, but may be illegal in the state where your consumer resides. Understand how your payment processing software works, so you don’t unintentionally charge fees to those in protected states.

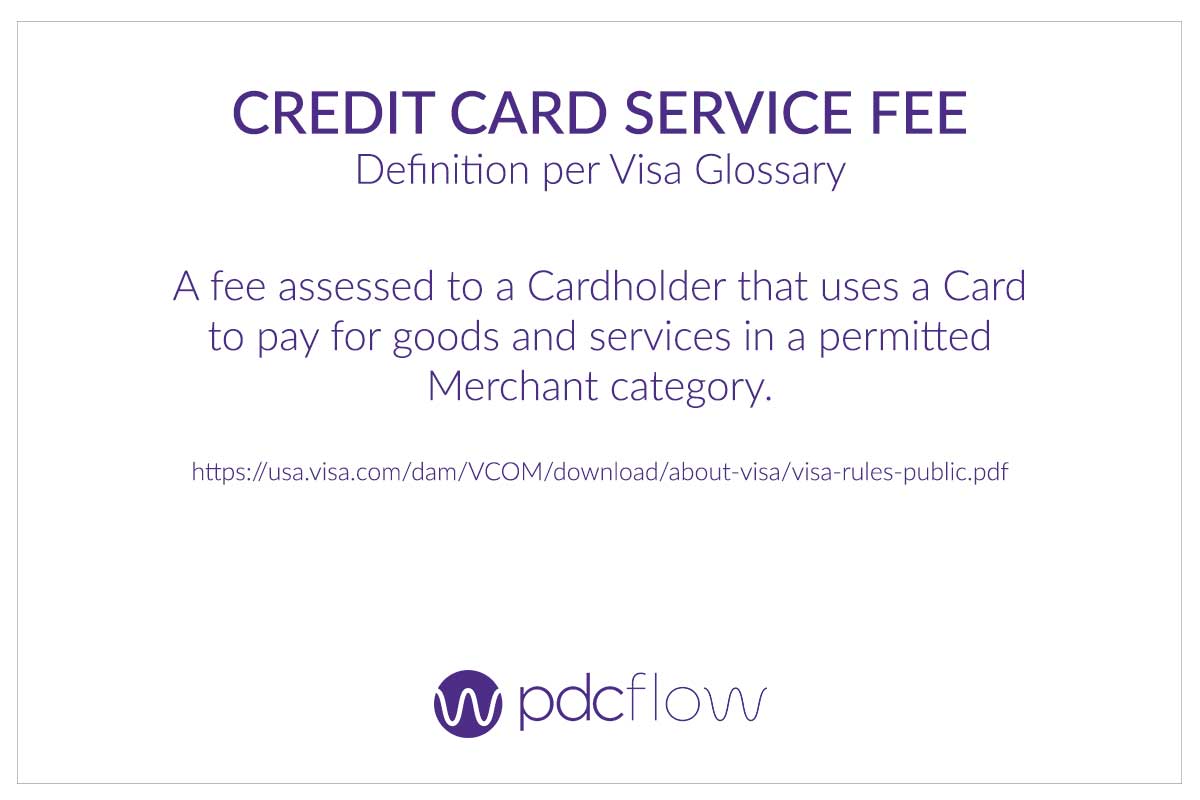

What is a Credit Card Service Fee?

Rules for Charging a Credit Card Service Fee

As a merchant, you can charge a service fee for credit card use. All the same rules above apply, with the addition of:

- Merchants must register with Visa.

- The service fee can only be charged by specific types of merchants with specific merchant category codes as determined by Visa.

- The service fee can be charged on in-person or card present transactions.

- The service fee can be charged on recurring payments.

- For Card Not Present (CNP) transactions, the payment and the credit card service fee must be submitted as two separate transactions when using a third-party to charge the fee.

- The fee can be a percentage, flat fee, or tiered, based on the transaction amount.

- The service fee can be charged by the merchant or a third party service provider.

- The fee can be different or adjusted based on payment type. For example, credit card, debit card, or ACH.

- The fee can be different based on the payment channel. For example, online, phone, or point of sale.

Is Surcharge Just Another Name for Convenience?

No! Surcharges, which only apply to credit cards, must be set up by the company providing the goods/services being charged. The business must also be registered with Visa for this purpose. A credit card surcharge can be added by a merchant for consumer payments made with credit cards, to cover the associated credit card fees charged by the merchant service provider.

Surcharges must also be included in the total the consumer is paying. For example, if the surcharge for a $100 payment is $5, the total should be $105, not $100, plus a separate $5. Also, just like many convenience fees, a surcharge cannot be used for a Card Not Present-only environment.

Understanding the difference between a convenience fee and a surcharge is very important. Surcharges cannot be placed on debit card transactions.

Because of this, merchants must be aware of how their payment systems work. Many payment systems are not able to differentiate between debit and credit charges, which can cause you to inadvertently violate surcharge regulations. Understanding how your payment system functions can help you avoid penalties for improper charges to customers.

Visa Rules for Charging a Credit Card Surcharge

Other surcharge rules that you should be aware of as a merchant:

- The surcharge amount is capped at 4% of the transaction amount.

- Any merchant can charge a surcharge regardless of Merchant Category Code.

- Consumers must be notified of the surcharge before they make a payment.

- State or local laws may prohibit businesses from charging a surcharge on credit card payments. Business owners should consult with their attorney before implementation.

- Surcharges are limited to USA card holders for both Card Present (CP) and Card Not Present (CNP) transactions.

- Surcharge fees must be shown on every receipt.

Options in Zero Cost Processing Solutions

Different merchant service providers (MSPs) have options in how they offer Zero Cost Processing merchant accounts to businesses. PDCflow has partnered with MSPs in order to support this type of fee-based processing model.

PDCflow software provides flexibility to merchants with the ability to utilize both a standard merchant account and zero cost processing account, so businesses can choose when to charge a processing fee to their consumers. Speak to a PDCflow payments expert to get more information on your merchant processing options:

Remember, it may seem difficult as a merchant to manage the processing fees related to credit card transactions, but not accepting credit cards can potentially lose you a lot of business.

Each payment channel a merchant provides makes it more likely that a payment will be collected. If you follow the rules, your business will be able to collect more and make paying bills more convenient for your customers.

For a concise breakdown on the information provided in this article, please download our Credit Card Convenience Fees Guide:

Download Credit Card Convenience Fees Guide

Want to know more about PDCflow Software?

Press ▶️ to watch our explainer video

ONE-STEP PROCESS

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles