Accepting credit cards for your business has many advantages. One of the most convenient aspects is knowing instantly whether a payment was approved or declined.

Rather than waiting days and dealing with a returned ACH payment, your business can know within seconds whether a credit card declined or was approved.

When a card has been declined, the most common credit card decline codes can give you some idea of the reason the payment was unsuccessful. However, the world of credit card payment processing is complicated.

There are countless reasons for a declined credit card that are not so easy to figure out.

The most common credit card declines are due to low funds (Insufficient Funds) or are a general decline from the cardholder’s issuing bank (Do Not Honor). Some others have nothing to do with the consumer.

These require you to understand a bit more about the payment process and how your company’s merchant account is set up.

SIC Codes and Credit Card Declines

Do you know enough about your SIC code to troubleshoot why it's causing a credit card decline?

Along with issuing bank and consumer issues, Standard Industrial Classification (SIC) codes can cause a card issuer rejection. A decline of Restricted SIC or Restricted Card may indicate the cardholder’s bank has deemed your business unsuitable for the type of card being used.

SIC credit card decline codes don't happen often when accepting payments, which is why some merchants may not think to research theirs. But just one declined payment can be a frustration when you’re focused on the bottom line.

One of the most common examples of an SIC code causing a card decline is the use of a Health Savings Account card. If your business is not coded properly to accept a card from a Health Savings Account, the payment will not go through.

Sometimes a merchant will be set up with a generic SIC code of 7299 (especially when a business doesn’t fall neatly into a category) and many issuing banks will block a customer transaction from businesses with this type of generic category code.

When you see a card was declined by the issuing bank, but need to secure payment immediately, it is best to have your customer choose a different way to pay.

However, this does not solve the underlying problem. To find out why the SIC code and card are incompatible, contact your merchant service provider to make sure you’re categorized correctly.

If you're in the right category, there is nothing you can do to fix the incompatibility causing some credit card declines. If you are not in the correct merchant category, your merchant service provider can help you get the proper SIC code for your business.

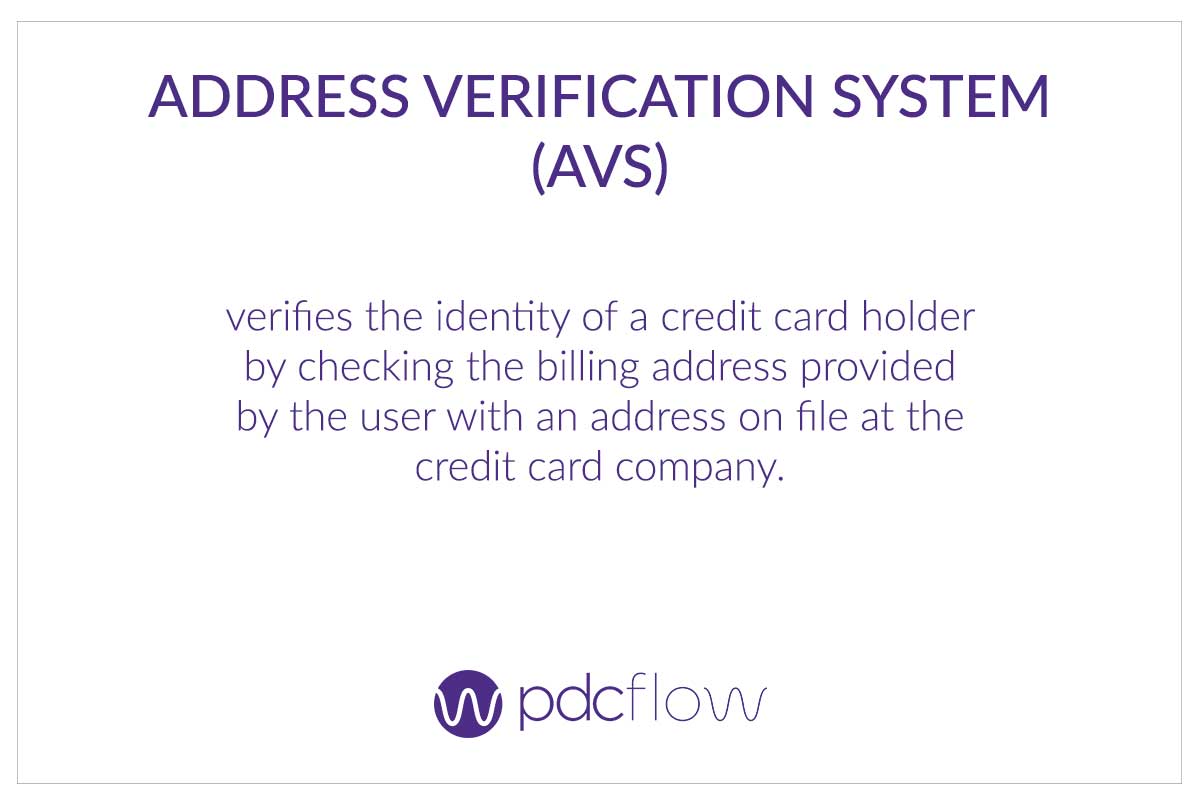

Card Declined by Issuer: AVS and CVV Mismatch

AVS is an address verification system that deals with two fields a merchant can require on their payment forms.

- Street Address

- Zip Code

The street address entered during payment should match the billing address the cardholder’s issuing bank has on file. Because the system was set up several decades ago, it only reads numbers. Therefore, the important element in an address match is a correct street number and zip code.

If the card declines due to AVS mismatch, the cardholder must call their bank to verify the address listed is correct. This is because the issuing bank (cardholder’s card provider) is the origin of this particular type of card decline.

CVV, card verification value, is sometimes also referred to as CVC, card verification code or “security code”. All refer to the same item - the three digits found on the back of all Visa, MasterCard and Discover Cards. For American Express, the CVV is a four-digit code located on the front of the card.

A merchant has the ability to set up their merchant account to check for CVV verification from the issuing bank in order to approve a credit card transaction.

If you receive a CVV mismatch decline message, make sure you haven’t entered the number incorrectly. If you continue to get a decline upon re-entering the CVV, the transaction might be fraudulent. You may advise the cardholder to call their issuing bank and will need to ask for a different form of payment.

Most merchants can use their card association’s AVS and CVV filter options to help prevent fraudulent transactions and chargebacks. These filters can usually be set up through your payment processing software or gateway.

Be aware, if these modules are not set up in your system, mismatched addresses will not cause a card decline.

Credit Card Decline Codes: Voice Authorization Required or Voice Call

Occasionally you may get a response of Voice Authorization Required or Voice Call. This does not always mean the credit card will be declined. Rather, the card issuing bank wants you, the merchant, to authorize the credit card transaction through a telephone call.

This is sometimes required when a cardholder is close to their spending limit. In this case, you have a few options:

- Treat the credit card transaction as a decline and request another form of payment.

- Choose to call the card’s voice authorization line. You must provide your merchant ID number (found on the statement you receive each month from your merchant service provider) and the card details. If the transaction is approved, you will receive the authorization code over the phone, and must process a post-authorization. Your payment processor can give you instructions on how to do this.

The card association voice authorization telephone numbers are as follows:

- Visa or MasterCard: 800-228-1122

- American Express: 800-528-2121

- Discover: 800-347-1111

Addressing a Credit Card Decline

If you are certain that you have the correct address, and have verified the card type, the most effective way to get to the bottom of a credit card decline is to ask the consumer to contact their issuing bank for further explanation.

There is little that can be done for a card decline if the bank is not consulted. If you understand what caused a decline, but it can’t be addressed immediately, it may be best to simply ask your consumer for a different form of payment.

If all else fails, you may also consult your payment processor about the common reasons for the codes you are seeing.

Keep in mind, however, although your processor may be able to help investigate why the credit card decline codes are occurring, the customer contacting their issuing bank is frequently the only way to resolve a credit card decline.

Credit Card Decline Codes You Should Know

Error

What it means

What to do

Error

What it means

What to do

Error

What it means

What to do

Error

Restricted SIC

OR

Invalid Service Code

What it means

What to do

Error

What it means

What to do

Error

What it means

What to do

Error

What it means

What to do

Error

What it means

What to do

Download Guide:

Want to know more about PDCflow Software?

Press ▶️ to watch our explainer video

ONE-STEP PROCESS

Updated Dec 2022

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles