Does your business still take traditional paper checks?

Waiting for payments in the mail makes it harder to reconcile accounts, stalls work, and impacts cash flow. Echeck is a faster, more modern way to take payments.

If your company wants to speed up payment cycles and make paying easier for customers, accepting eChecks is the way to go.

What is an eCheck Payment?

They are digital payments that function the same way as a traditional paper check. Bank account and routing numbers are used to transfer funds from one account to another.

They are processed electronically through the automated clearing house (ACH) network. This is the national network that facilitates electronic funds transfers (EFTs).

Typically, companies use eChecks to offer another payment method to customers who don’t want to pay by credit card.

eCheck vs ACH: What’s the Difference?

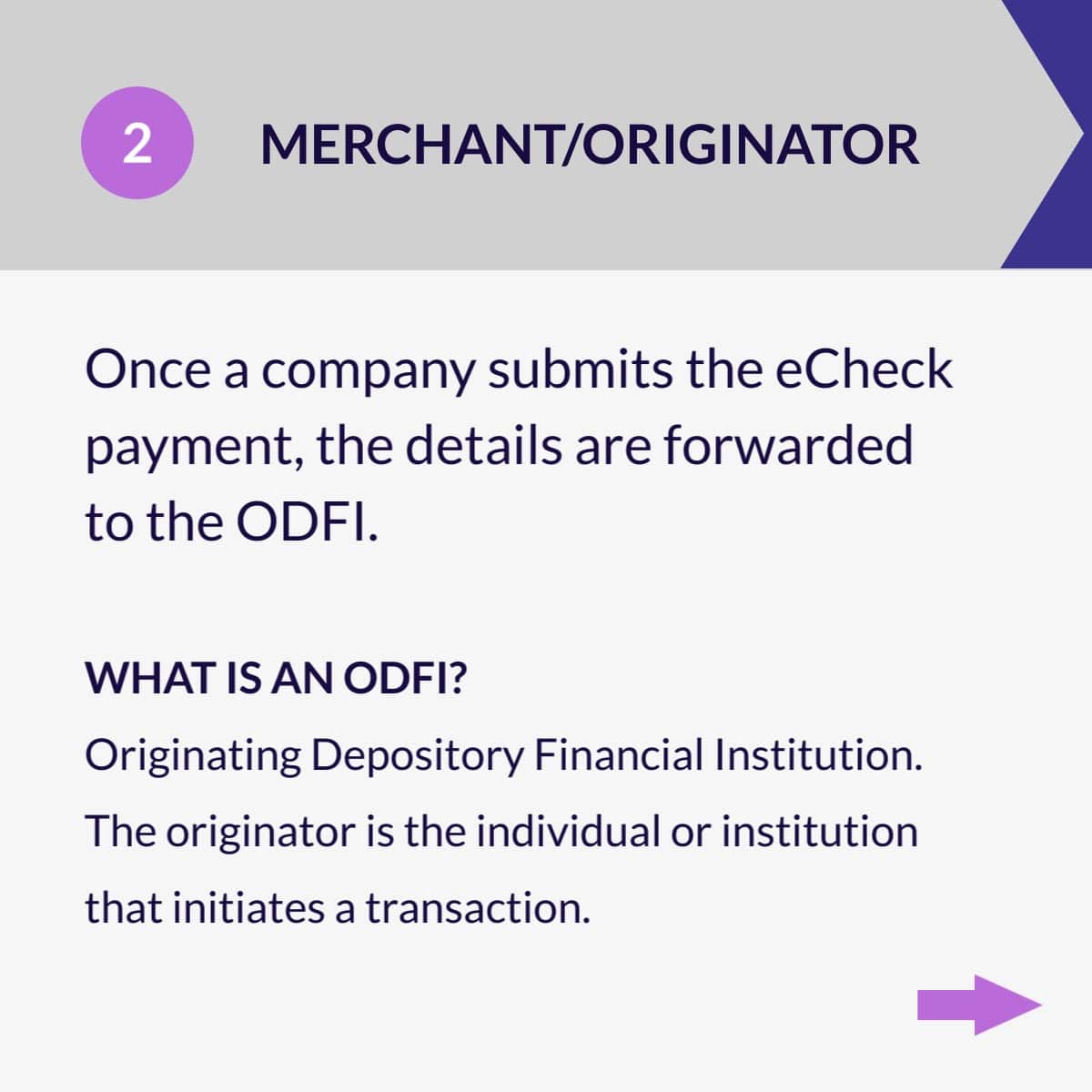

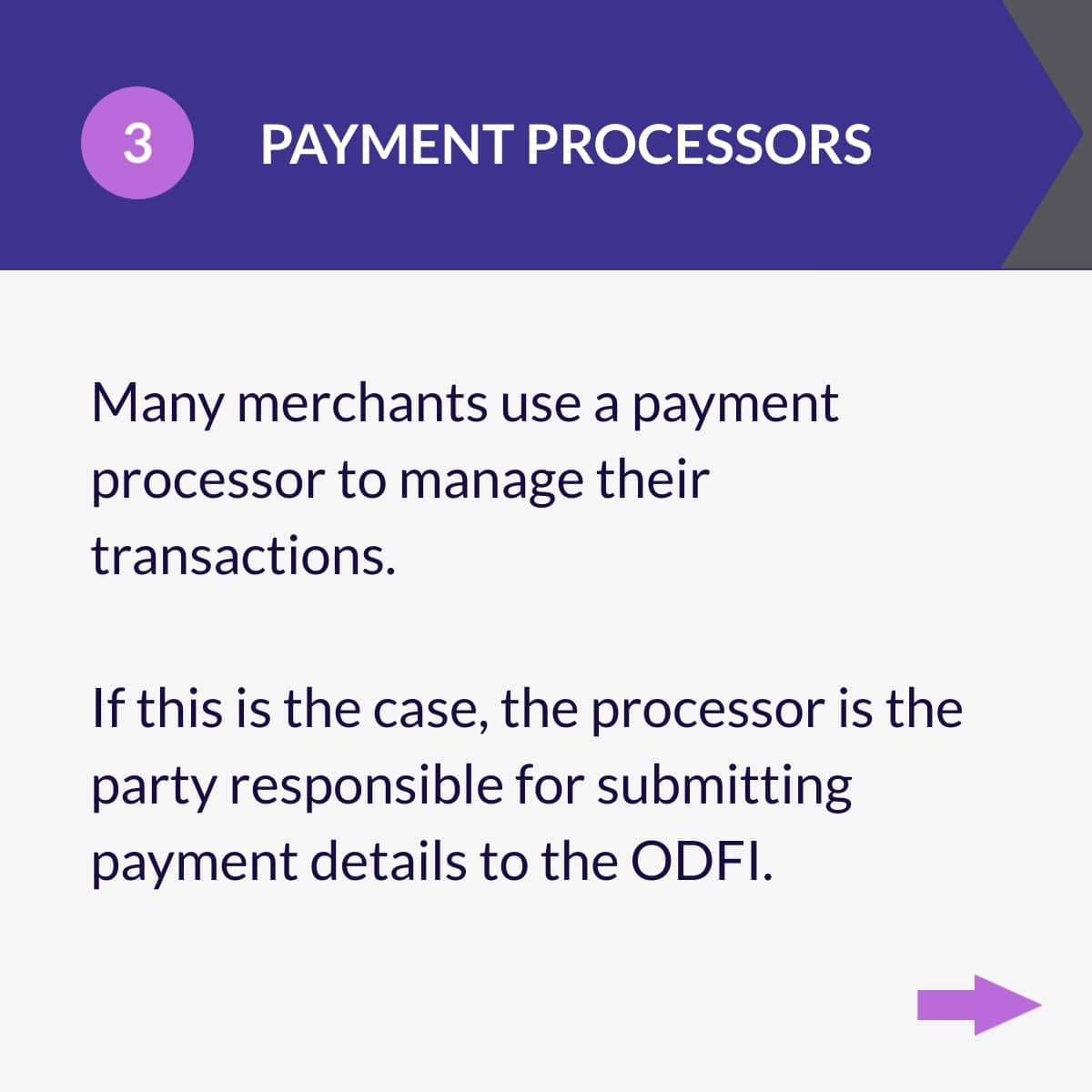

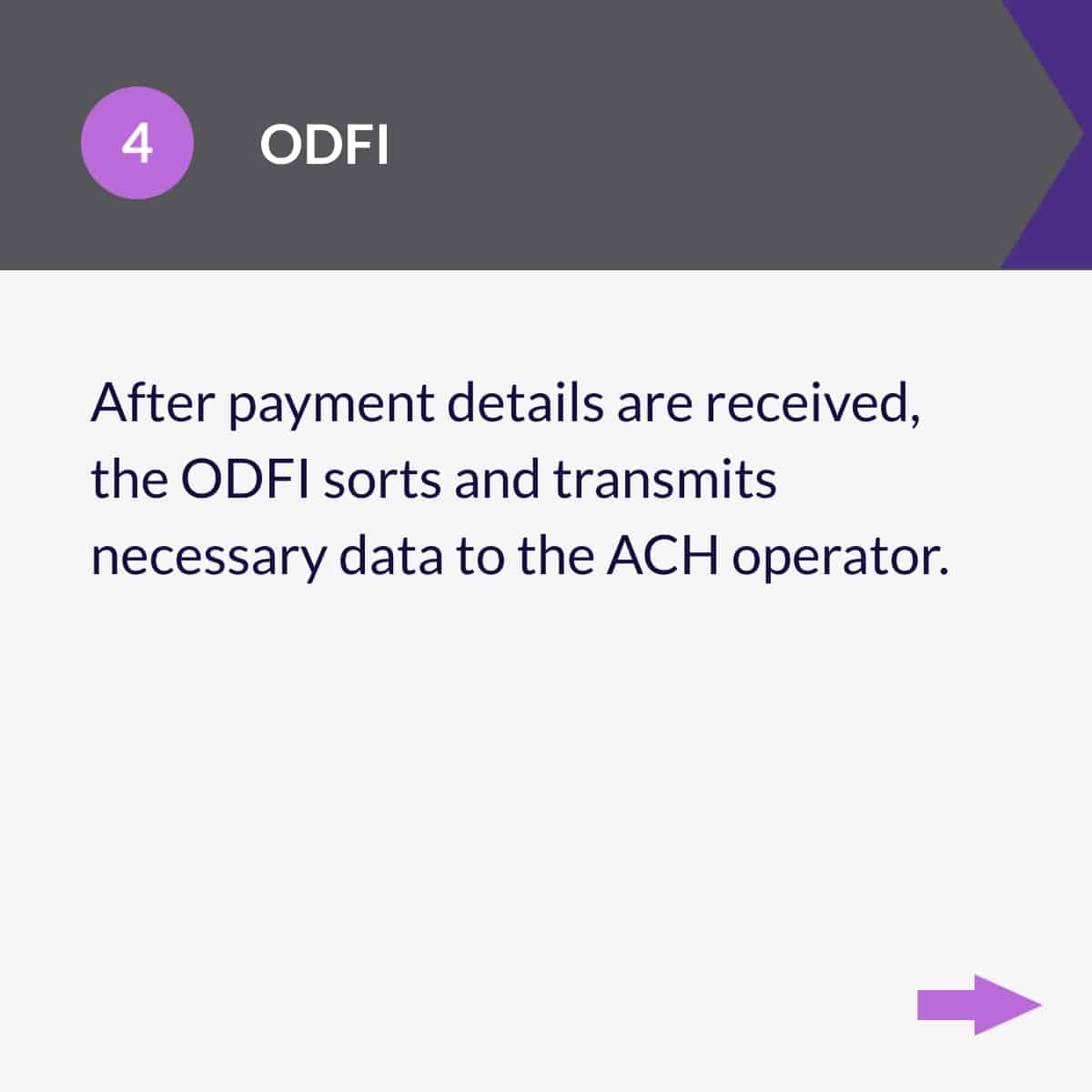

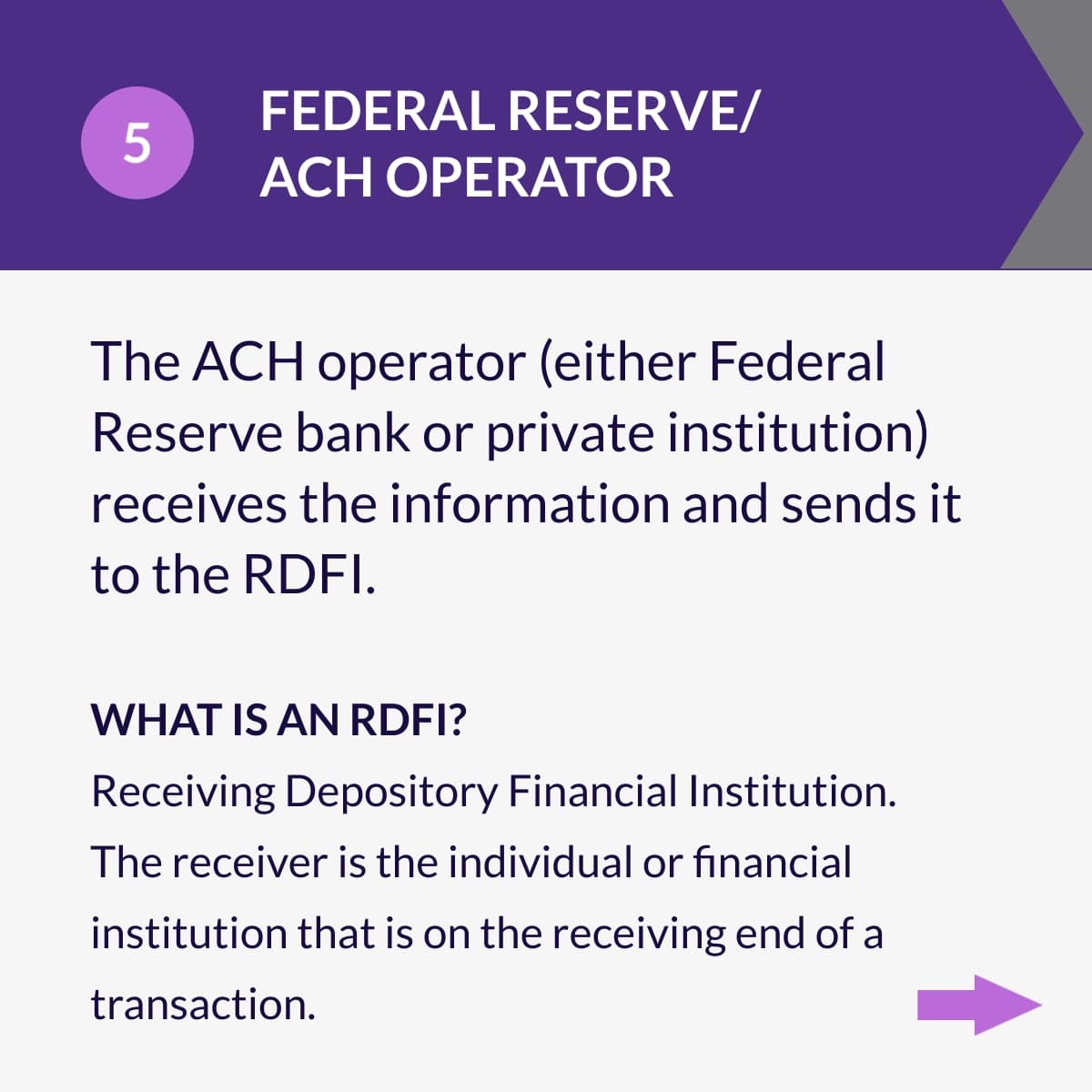

How does eCheck Payment Processing Work?

As far as the ACH network is concerned, eChecks are processed the same way a paper check would be. For companies and customers, though, the process is much less hassle.

- Get authorization - The first step of an eCheck payment is to get authorization from the customer to run the transaction. It is important to gather authorization to fulfill Regulation E and Nacha compliance requirements. PDCflow offers authorization requests you can send by email or text message, so customers can sign them right away.

- Take the payment(s) through your software - Input payment information in your payment processing software. PDCflow offers online payments, email or text payment requests, and employee-initiated payments. Details are added according to the channel used (either by the customer or your employee) then submitted to be processed.

- Receive funds - After the eCheck payment is verified, submitted, and processed, the funds are placed into the desired merchant account. For businesses with complicated rules on where funds must be deposited, PDCflow can accommodate multiple accounts.

How Long Do eChecks Take to Process?

Some companies don’t anticipate how long it takes to process an eCheck payment and aren’t prepared to reconcile their accounts.

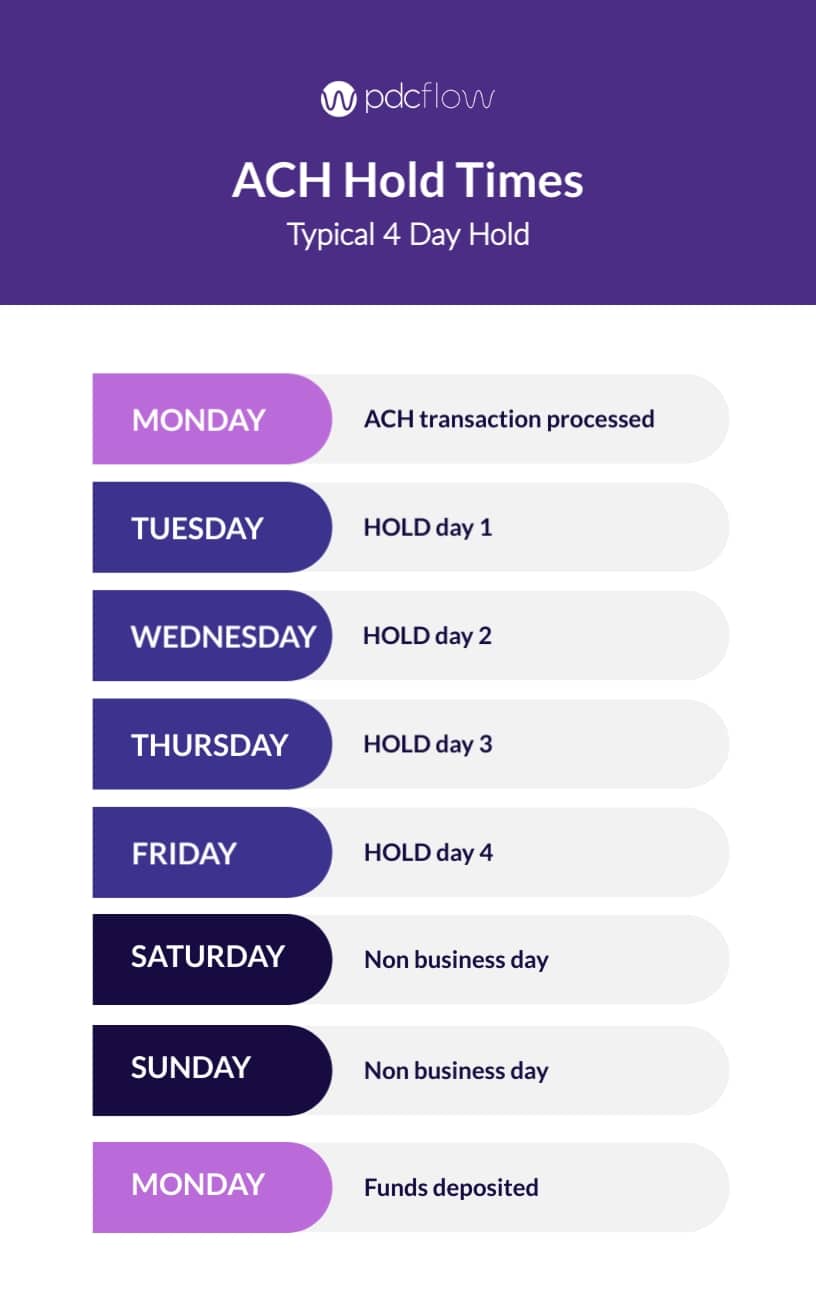

Usually, eCheck funds have an average hold time of around four business days. This means that it’s typical to see funds about a calendar week after the transaction was submitted.

With this timeline, it’s important to note: transactions that use the ACH network for processing are submitted as a batch, often at the end of the business day.

This means, when estimating funding times, the hold window calculation must begin the day after a transaction is posted.

eCheck Payment Processing Time

Are eChecks Safe for Businesses?

Yes, eChecks are safe for companies. In fact, eCheck payments can be even safer than a traditional check payment.

Digital transactions mean no one from your organization needs to worry about transporting a check to the bank to be deposited.

Your payment software should also offer payment security features that keep transactions even safer. When you take ACH payments with PDCflow:

- Companies can use ACH Verify to validate bank account information before a transaction is submitted, so you don’t experience fraud or returned payments due to mistyped details.

- PDCflow tokenizes and encrypts all payment information so it is kept safe during processing and storage.

- PDCflow securely stores customer eCheck payment information, so your company doesn’t have to manage this burden.

Should my Business Accept eCheck Payments?

Many companies aren’t sure if they are a good fit for eCheck payments but the reality is, customers expect this faster, easier, more secure option. If you’re not offering what they expect, you’ll create roadblocks to payment.

ACH transfers are also good for office processes across the board. Here are some perks of electronic check payments:

- Customers don’t want to mail a check. Making it more convenient to pay increases prompt payments and reduces abandonment.

- Echeck transactions eliminate excess trips to the post office or bank, because everything is taken care of within your payment software.

- Digital payments are also easier to track. The person who signed an agreement or contract isn’t always the one who writes their checks. Digital payments through your processing software associate an account number with the payment, so you always know where a payment should be attributed.

- When you take payments all from within one payment system, it becomes easier to reconcile each month. All transactions are recorded automatically, so reporting doesn’t rely on staff input and can give you a fuller picture of your company’s financial performance.

PDCflow ACH Payment Services

PDCflow offers eCheck payment processing services for a better customer experience. With our software, you can take ACH payments in several ways:

- online

- by email

- by text

- employee-initiated through a virtual terminal

- through web chat

- through recurring payments

Along with ACH payment processing, we offer credit card payments, and the ability to send digital communications to customers.

Take control of your business today by sending documents, requesting payments and getting esignatures all in a single message to customers, through email or text.

If you are interested in taking ACH payments for your business, sign up for a meeting with a PDCflow Payment Expert today.

Request a Demo:

Want to know more about PDCflow Software?

Press ▶️ to watch our explainer video

ONE-STEP PROCESS

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles