1) What is the strongest current trend in payment processing?

Just as with many other industries, satisfaction and convenience are top concerns in ACH and credit card payment processing. Customers want to make payments quickly and easily, no matter what business they’re interacting with.

Your company should offer multiple channels and payment types to consumers. Online payment options should be friction-free and simple to navigate.

2) What new technologies are available in payment processing?

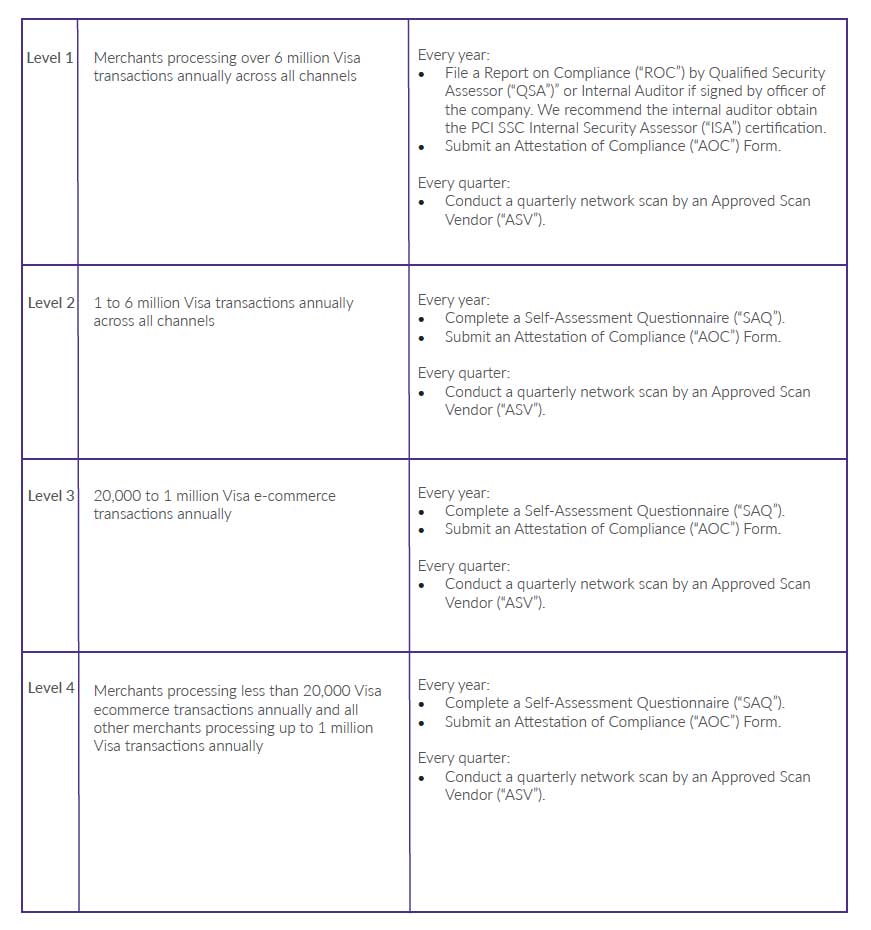

3) How can payment processors reduce risk and cost? How can they monitor compliance?

- PCI compliance - PCI compliance for credit card payments is a huge cost. Payment processors should be able to significantly reduce the scope your business needs to comply. This accomplishes both at once – reducing risk in your business and reducing costs of the audits and other associated expenses.

- Nacha compliance - For ACH payments, Nacha has created regulations your business must follow – including a recent rule regarding account validation. Your processor should be following these regulations and be aware of what you need to do as a company to comply. They should be approaching you with solutions that allow you to maintain compliance.

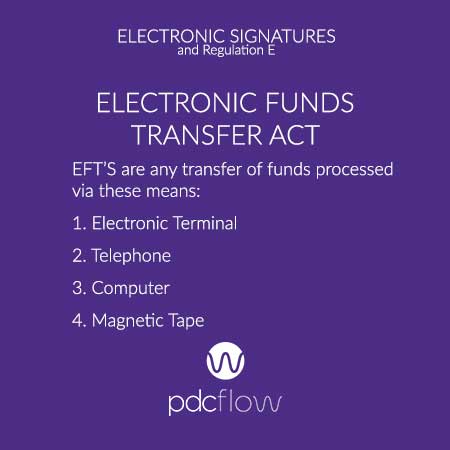

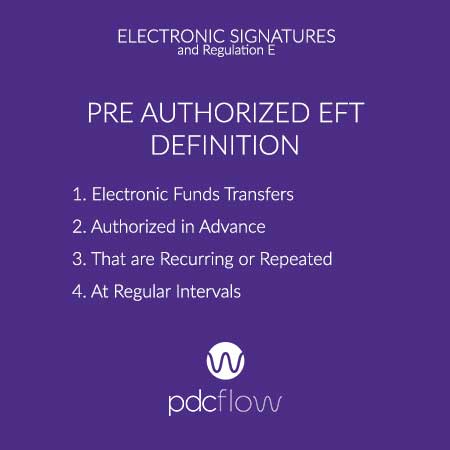

- Regulation E - Regulation E is the regulation within the Electronic Funds Transfer Act (EFTA) stating what EFT compliance is required according to the act. When taking EFTs, you’re required to gain proper authorizations from consumers, provide a payment receipt and more. Does your payment processor offer built-in Regulation E compliance functionality to speed up the payment process?

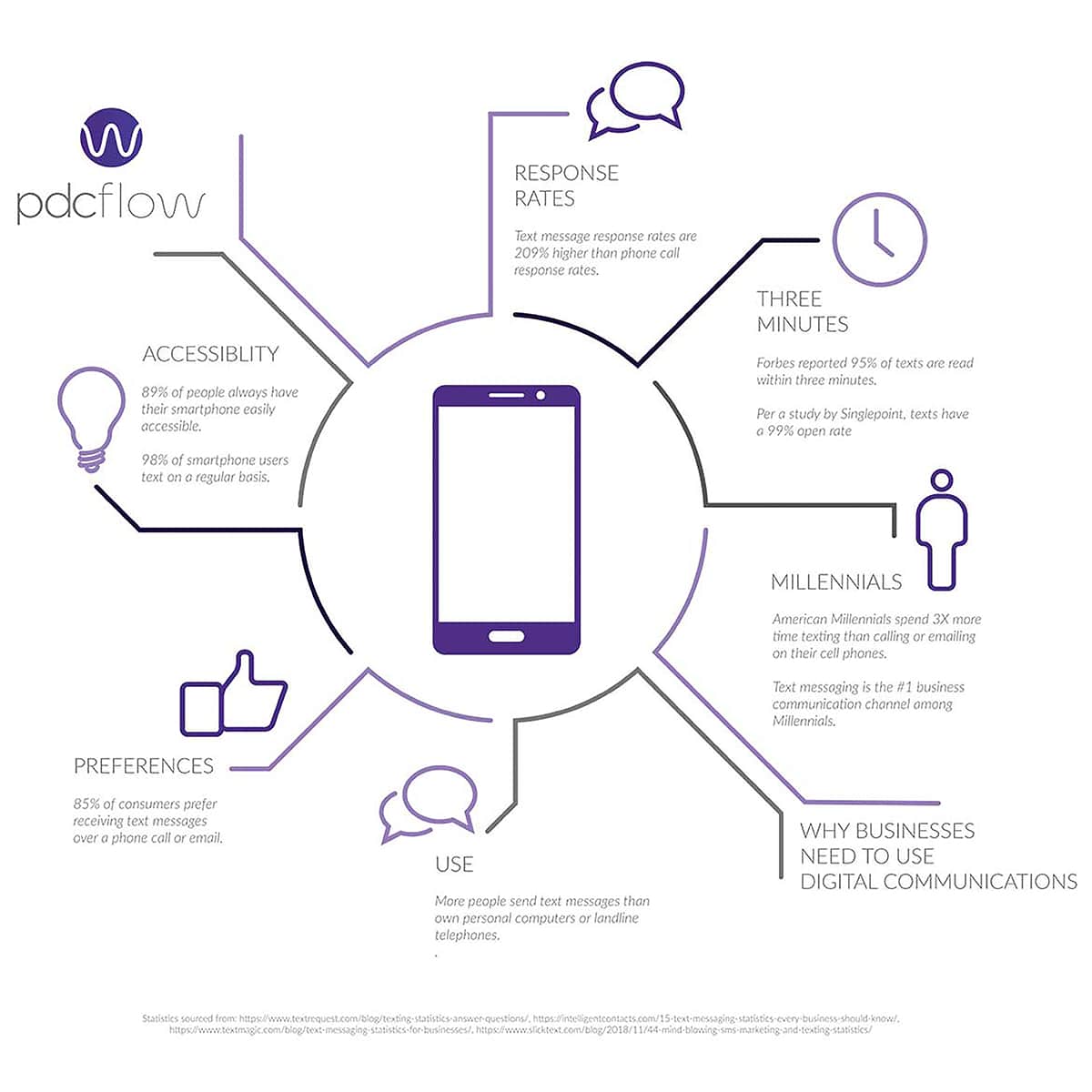

4) How can you use text and email to reduce costs?

Reduced mailing costs

Simplified training

Chargeback reduction

5) What new rules are currently impacting payment processing?

PCI compliance is the biggest compliance concern, but those who accept ACH payments also need to comply with Nacha’s rules, and there are also federal regulations surrounding the way electronic fund transfers are performed.

Of course, an industry regulation that also comes into play is Regulation F. This regulation has many guidelines around how email and text messaging can be used in debt collection when interacting with consumers, and much of that has to do with payment collection through those channels

6) How will the new NACHA account validation requirements affect payment processing?

Nacha recently enhanced bank account verification requirements to protect consumers from fraud and reduce the occurrence of failed ACH payments. For some companies, this rule may cause minor disruption when deciding the right features they should adopt to meet this requirement.

However, once companies have implemented their process, the impacts should be positive. There will be fewer returns from invalid accounts, which will lower return rates and save staff time trying to track down consumers for alternate payment information.

7) How will texting be used with payment processing going forward?

8) How should you approach texting opt outs?

Consent is critical. If a consumer has opted out from receiving texts from your company it will be important to get consent before texting them again. Be sure your technology is flagging opt outs by mobile number so you don’t inadvertently contact a consumer by mobile phone if they’ve opted out of receiving texts to that phone number.

But remember, many customers may want to opt back in if they speak to an employee and then decide that (a) the requests from your agency are legitimately important and (b) receiving updates by text is the most convenient method for them personally. Be sure you understand how that consumer can opt back into receiving text messages about any campaigns from your company.

If you want to learn more about how digital communication channels can enhance payment security, improve office workflows and save your company time and money, download this Traditional Vs. Digital Communication for Accounts Receivable comparison.

Download Traditional Vs. Digital Communication for Accounts Receivable Comparison

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles