There are countless risks associated with running a business and tactics for preventing or responding to them are always changing. Especially in the accounts receivable industry, there are many unpreventable risks that can become costly if not properly addressed.

Earlier this year, Performant Corporate Counsel Lauren Valenzuela and Finexus Insurance Agency CEO Katie Zugsay discussed new risks and better operational risk management in financial services. Zugsay explained that you’re likely to face unavoidable risks in your business but understanding your business insurance policy can help.

Anatomy of a Business Insurance Policy: Insurance Provisions

1) Declaration page

2) Insuring agreement

3) Exclusions

4) Conditions

5) Definitions

6) Endorsements

Claims

What is the claim and what is the basis and nature of the claim?

Consumers or plaintiffs’ attorneys or regulators may use a specific label to describe the situation in question. However, you shouldn’t feel stuck to a specific phrasing. What is the actual nature of the situation?

Zugsay offers this example: oftentimes, FDCPA cases allege improper third-party disclosure. They may add a breach of data and an “intrusion into seclusion” to this situation as well. This is an important time to speak to your insurance broker. You may find that the claim fits better under your cyber policy.

Additional coverages

Become familiar with any additional coverages your policy may include. Sometimes brokers won’t mention every additional coverage within a policy because they may not realize they are relevant to your agency. Agencies, likewise, may not think to look to their Errors & Omissions policy for these particular types of coverage, but nevertheless, they’re often there.

These additional coverages, such as licensing proceedings or subpoena defense, can provide you with money when you really need it. It’s also important to note that these additional coverages often don’t include a deductible.

Zugsay suggests you may ask your broker for a cheat sheet of these additional coverages, or you may want to create one yourself. Keeping a list of these easily accessible will help you identify them quickly if the need arises.

Timing

Occurrence policies vs. claims-made-and-reported policies

Under an occurrence policy, your company is protected from covered losses even if a lawsuit is filed years after the policy period ends, as long as the incident itself occurs during the policy period. The time of reporting (as long as you report it to the carrier timely after becoming aware of the lawsuit) would not be an issue in this situation.

For claims-made-and-reported policies, however, the claim must both arise and be reported within the dates of the insurance policy period. Zugsay warns that you must be aware of retroactive dates, which define how far back an incident can occur for it to still be covered under your policy.

Retroactive dates are important to understand especially when you are changing carriers. Depending upon the retroactive date in a new policy, past activities (calls, letters to consumers, credit reporting, etc.) may not be covered under the new policy. You must plan for this or negotiate with the new carrier to adopt your former date, to eliminate this gap in coverage.

What type of protection do I need?

What protection are you seeking?

What is the most important type of protection that will benefit your business? Debt collection agencies are likely to deal with the FDCPA, FCRA, TCPA and other regulatory issues at some point during operation.

Check the details of any defense protection included in a policy. Attorney’s fees are not always included, which could leave your agency responsible for a large expense in the event of a lawsuit.

Defense in a policy typically only covers legal defense costs. Indemnification, however, is a separate protection. Unlike defense, indemnity typically addresses settlements and final judgements. Often, insurance companies will also offer a combination of both protections.

Zugsay urges companies to think ahead about what’s important. Think about what you need, and ask for that coverage, and don’t forget to omit what you don’t need. Don’t get extra coverage that will never be relevant – you don’t want to needlessly pay more for your policy.

Related claims

Another little-known provision of many insurance policies is the ability to relate multiple claims under one deductible within your policy. This may apply, for example, to a single error that caused multiple lawsuits from consumers against your agency. If the provision applies, you would only have to meet your deductible a single time before receiving insurance benefits for multiple claims.

Zugsay warns, however, that this feature should be used with extreme caution. When negotiating with a new carrier, for example, this may make you appear to be a higher risk client than you are. She suggests to simply be aware of this provision and have an open conversation with your broker to evaluate all possibilities available to your business.

Traps for the Unwary

Telling the Story

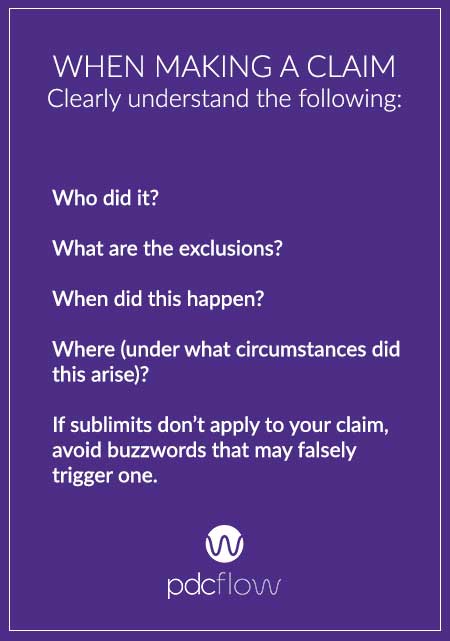

The care you take when communicating with your carrier is just as essential when making claims. Always be truthful and be sure you don’t mischaracterize events and timelines. Doing so may cause your claim to be mistakenly denied. When making a claim, clearly understand the following:

- Who did it?

- What are the exclusions?

- When did this happen?

- Where (under what circumstances did this arise)?

- If sublimits don’t apply to your claim, avoid buzzwords that may falsely trigger one.

Cooperation

Cooperation is essential for your insurance policy to work as intended. Be sure your reporting is timely and ask for bordereau reporting if needed. Bordereau reporting allows you to compile and send periodic summaries of claims and potential claims to your carrier, to simplify reporting if you have a high volume of potential claim activity. This must be negotiated ahead of time with the carrier.

Cooperation during settlements is also important. Look out for “hammer clauses” in your policy. A hammer clause may apply if your agency is offered a settlement you don’t agree with, but the insurance company feels is fair. In that case, you may find your company financially responsible for the entirety (or some larger portion) of the court case that follows the rejected settlement offer.

Next Steps

Now that you know the basics of an insurance policy and the considerations to keep in mind when looking for coverage, it’s time to identify the next steps in managing your risk. Does your current risk management program cover the risks you face? To find out if you’re prepared, you must:

- Identify your risks - What are the risks your organization faces? Are you prepared for these risks?

- Understand your documents - are you paying extra to shift risks that don’t apply, or aren’t a big threat to your business?

- Compare risks with your program and fill the gaps - are there new risks that you may be overlooking? What needs to be done to mitigate or shift these risks?

- Follow up on reservations of rights and pending claims - are you keeping track of your claims? Pay attention to pending claims in the event that they are denied, leaving you on the hook for the costs of an incident.

- Strategy for responding to claims - Are there risks you’re mitigating that your insurance carrier needs to know about?

For more accounts receivable content and news to help you win business, increase efficiency, and take more payments, subscribe to the PDCflow blog.

Subscribe to the PDCflow Blog

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles