Updated June 2022

The Consumer Financial Protection Bureau (CFPB) is responsible for maintaining the safety of customers who interact with financial businesses. Because they create and enforce the regulations that govern the credit and collection industry, collection agencies know this organization well.

But do you know the best way to handle a complaint about your business filed directly with the CFPB?

CAC Collection Boot Camp panelists and collection experts Kelly Parsons-O’Brien, June Coleman, Shawn Suhr and Courtney Reynaud shared their thoughts on addressing CFPB complaints. If you don’t know how to handle CFPB complaints, or want to learn better ways to handle them, take a few moments and check out these tips from collection industry experts.

Are You Registered with the CFPB?

As the Bureau’s social media presence grows and more consumers are aware of their ability to make complaints, your agency will begin to see more claims against you in the CFPB database. Parsons-O’Brien states that in her own agency, she has seen a substantial increase in CFPB complaints. “In 2013 we got seven. This year so far, we’ve had 25.”

If your agency isn’t already signed up to address these complaints, visit the CFPB’s website. You can fill out their registration form and learn more about the CFPB complaint process as well as your rights to respond as a merchant.

How to Handle CFPB Complaints

Once you’ve registered, you will be able to respond to complaints aimed at your business. But there are a few steps you may take first. It is important to prepare yourself and ensure you’ve done all you can to satisfy your consumers. Here’s Parsons-O’Brien’s advice for dealing with a CFPB complaint:

- Investigate - It’s important to thoroughly investigate disputes. While you may already have a stringent process for disputes in your office, a mishandled issue linked to the CFPB can lead to a lawsuit. This means it is vital to be extra cautious in addressing these issues.

- Get your ducks in a row - A dispute response in writing is important to addressing CFPB consumer complaints. You don’t want to respond only to find out you are wrong. Be ready to cancel any account if your documentation and documented procedures are not ironclad. Return the funds and move on.

- Reach out - Parsons-O’Brien also urges an often overlooked step in the process – contacting the consumer directly. You can resolve many issues simply by having a top member of your leadership reach out. Ensure your representative is polite and interested in the consumer’s concerns. A genuine and helpful manner will go a long way towards finding a solution. Try to resolve the dispute if you can reach the consumer. If that’s not possible, extend an invitation for them to contact you.

Prepare a Response to the Complaint

If reaching out to the consumer directly doesn’t work, you should prepare a response to provide to the CFPB. When drafting your statement, here are a few things to keep in mind:

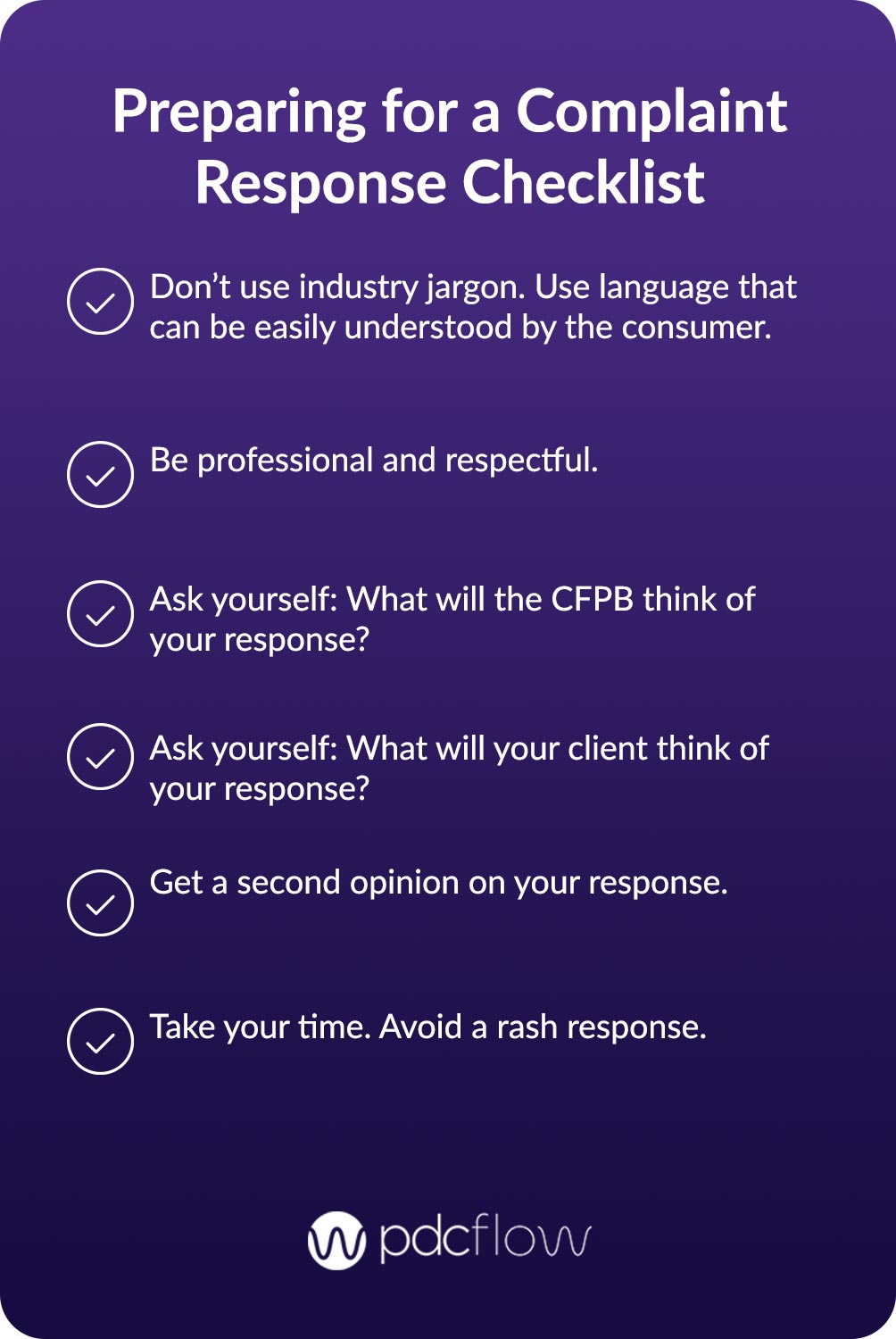

- Your consumer is not in the industry - Because those filing complaints likely do not have a background in collections, it is important to use language that can be understood by the “least sophisticated consumer.” This means being concise and avoiding industry jargon that those in the general public are not likely to recognize.

- Your response could be made public - In the age of social media, it is increasingly likely that an interaction with your consumers may end up on Facebook, Twitter, or somewhere else on the internet. Don’t say anything disrespectful or retaliatory and avoid statements that could put your organization in a bad light.

- Ask: What will the CFPB think? Is there anything in the statement that the CFPB would find inadequate? Is your language clear?

- Ask: What will your client think? Because you are collecting on behalf of another organization, you must also keep in mind how this issue will reflect upon them. Don’t throw them under the bus or make any comments that might make them look bad (unless you want to lose their business).

- Get a second opinion - When sending your response, it’s helpful to first have another manager at your agency read what you have prepared. Ask them to put themselves in the shoes of the consumer. Do they find the language troubling? Are there phrases that could be misconstrued? Having a second pair of eyes read your statement can help you avoid further issues with an already dissatisfied consumer.

- Take time to cool off - Getting a CFPB complaint can be frustrating, and sometimes it may even feel personal. In order to maintain composure and a professional appearance, take a day or two before drafting your response. Have others in your agency head up the investigation so you have time to clear your head for the issue. That way you can reflect on how best to address the complaint and avoid providing a rash response that would cause further issues down the line.

Handling Complaints In-House

Of course, it’s even better for consumers and your business if you can record and resolve complaints inside your agency instead of through the CFPB consumer complaint database.

Clark Hill Law attorneys Leslie Bender and Joann Needleman recently shared this strategy during a webinar regarding the CFPB’s latest priorities of enforcement and supervision. They view proper complaint handling as an essential part of ARM compliance management systems (CMS).

You should have a system for receiving and responding to consumer complaints so you are in control of your agency’s reputation and can build rapport. Capturing and storing complaints will also let you track them and recognize trends.

A recurring complaint may mean you have gaps in your policies and procedures.

Want to receive notifications for upcoming events, content and resources to help you with compliance, security, digital payment strategy, and customer experience? Subscribe today!

Sign Up:

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles