Regulation F and reaching consumers through electronic communications is now a reality. Debt collection agencies have prepared as best they can and have implemented new compliance policies and procedures.

But what about creditors?

All creditor clients that use a third-party agency should know about Regulation F. Are you (and more importantly, are your clients) ready for data maintenance and handoff procedures requiring high trust and communication?

In a PDCflow-sponsored webinar through Accounts Recovery, Panelists Chuck Dodge, Hudson Cook, LLP and Matt Stegall, Vantage Credit Union, discussed consent management for electronic communication from both perspectives.

Types of Consent

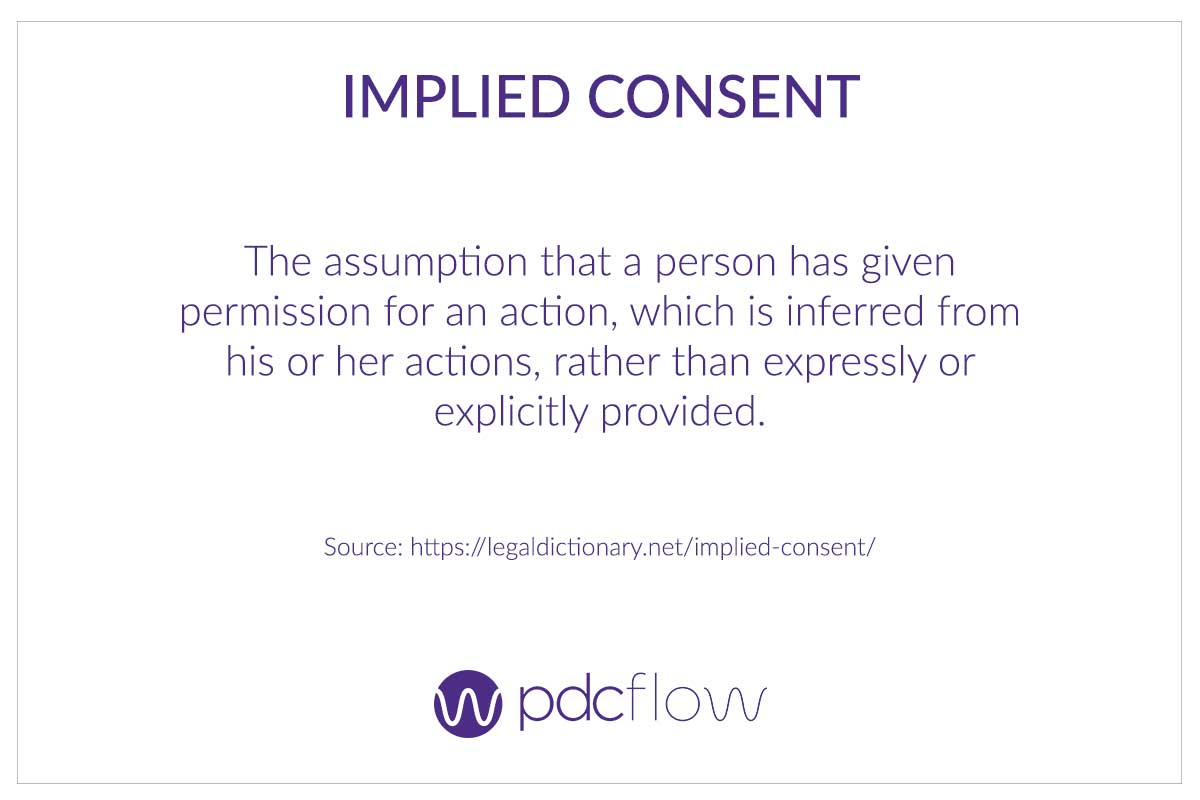

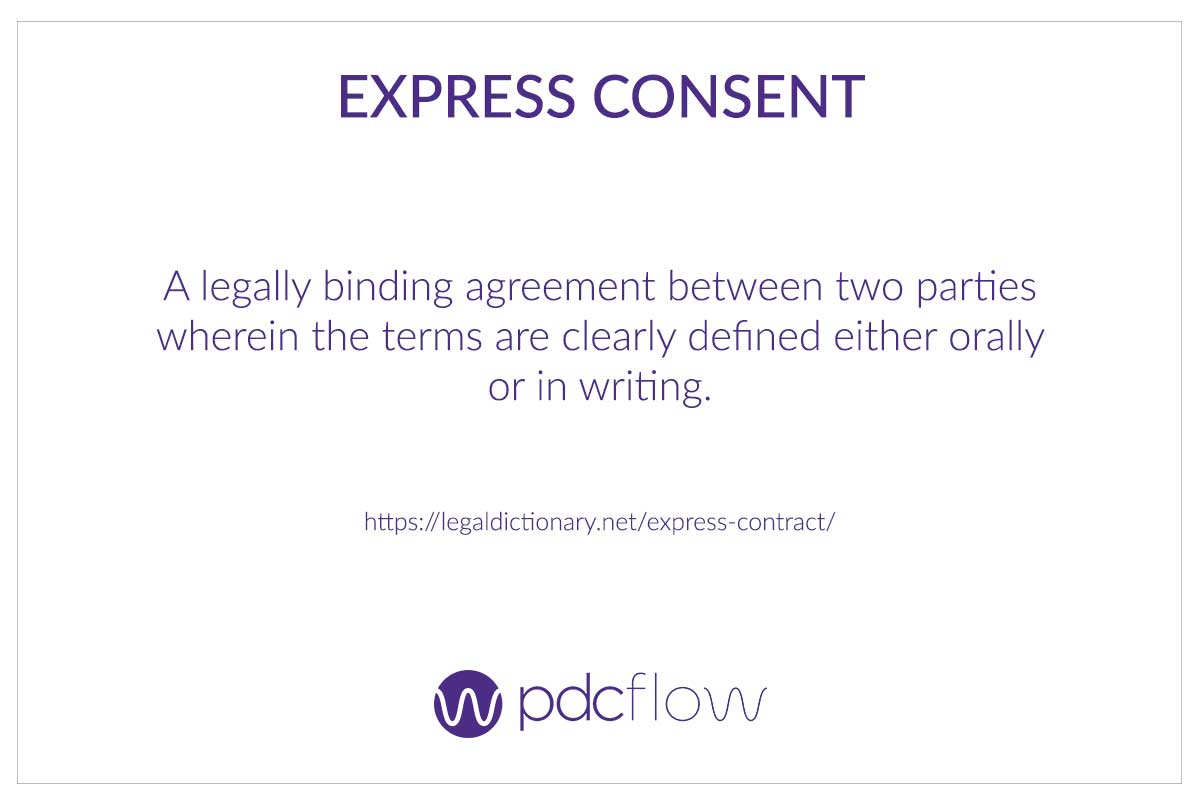

IMPLIED VS EXPRESS CONSENT

Regulation F permits debt collectors to use digital communication like text messages and email. But these practices come with strict rules about gathering consumer opt-ins and opt-outs.

For compliance purposes, there are two types of communication consent you may gather from a consumer – implied or express consent. Knowing the difference is essential because obtaining the right consent may take extra work and a stronger partnership with creditors.

Implied Consent

Implied consent works just as the name suggests. A consumer’s actions imply they consent to what you’d like to do with their information.

For example, a consumer who stays on the line after hearing a call recording disclosure implies their consent to be recorded. Creditors often use this type of user consent because it satisfies their compliance burdens

Express Consent

Express consent is more formal, and generally preferred by attorneys, as it provides a greater defense if challenged. Express consent is typically gathered in writing, either through a legal wet esignature tool or on paper.

Express consent can also be gathered through a recorded call conversation. Front-line collectors should understand the difference between express and implied consent and know which is appropriate to gather, depending on the situation.

Data Management Systems

Who is responsible for data collection and maintenance along the payment collection chain?

“Definitely upon assignment, I think a lot of the weight is on the creditor to make sure their data’s clean...Once the account is in that debt collector’s office though, that’s where I think the burden is on them,” says Stegall.

Within his credit union, they include language about consent to receive electronic communications in the terms and conditions of membership agreements or any time a consumer signs up for new services.

When accounts are placed with a third-party collector, original creditors should hand over the emails and mobile numbers of anyone who opted in during the initial process.

These consumers are subject to passthrough consent rules.

Collectors are allowed to contact the new accounts via email or text, but extra consent may be needed before sending an electronic Model Validation Notice, depending on the agency’s processes.

“The critical component is how we communicate back and forth with these things,” says Dodge. “Especially if you have a relationship with a debt collector that’s going to be a primary placement or secondary placement for a period of time, and during that period they get some kind of revocation of consent.”

Because both creditors and clients must own a portion of the consent and preference management process, you should establish clear, consistent communication between both parties. Responsibilities should be outlined in your commercial agreements so everyone understands what is expected of them.

How to Work with Creditors to Get Consent Webinar Recording

Communication Consent Channels and Revocations

Regulation F’s main purpose is to give consumers greater control over how debt collectors can interact with them. This means consumers should be able to choose the dates, times, and communication channels.

In line with this philosophy, you should offer the ability for consumers to opt in and out of channels as they choose. Meaning, that consent for electronic communications and revocation can be given for (or taken away from) any channel at any time the consumer wishes.

Log all new opt-ins and revocations you encounter during collection, so they can be passed back to the client for future reference. Be sure you’re also equipped to honor changing consumer consent and preferences in a timely manner.

Disregarding consumer preferences is against Regulation F compliance, damages the customer experience, and erodes client trust in your business.

Strengthening the Client/Collector Relationship

Be ready to share your processes and explain your Regulation F compliance plans with prospects and current clients. Perhaps most importantly, be honest about your limitations.

If data a creditor client provides is out-of-date or inaccurate, you need to be clear about how it might affect your processes.

Keep your relationship strong through communication, honesty, and transparency. You must be able to tell the companies you service what data you need and how you plan to use that data during collection.

They want assurance that you are knowledgeable about compliance and consent for electronic communications to help them maintain their consumer relationships. This way, clients can continue to regain lost revenue and debt collectors can work as effectively as possible.

Impact of Electronic Communication Consent

Since Regulation F’s implementation, digital communication has become an expected – almost essential – part of the standard debt collection strategy.

Debt collectors and creditors both see more positive impacts from email and SMS communications from higher engagement rates to faster account resolutions.

When creditor clients outsource bad debt to third-party agencies, it is in their best interest to make the transition as seamless as possible, so consumers are fully aware of the change.

Creditors should provide agencies with current, reliable contact information for those that have given passthrough consent.

They should also consider using email and SMS communication channels to send handshake letters before handing consumers over to agencies. This cuts down on misunderstandings and prepares customers for future debt collection activity.

A handshake letter is when an original creditor sends an email or text communication to a customer who has become delinquent, informing them the account will be passed to a debt collection agency on a specific date.

This gives the customer a final opportunity to address the past due bill with the creditor and introduces the collection agency by name, so the customer is familiar with the agency when the first communication is sent.

What is the revenue impact of creditors passing consent for electronic communications to agencies?

Letters and phone calls are no longer effective and the operational cost is significantly higher. If agencies can cut the cost of collections, the savings can be passed on to their clients.

Agencies collect more through digital communication channels, which means creditors will reduce their losses. One PDCflow client who recently implemented SMS has seen these results in as little as one month after implementation:

- 24% increase in total payments

- 55% increase in total payment amounts

- 26% increase in average payment amounts

PDCflow for Flexible Digital Communications and Payments

Plug-and-play email and SMS channels

Use our pre-approved messaging to get started quickly with email and SMS, without the extra cost, waiting to be approved by phone carriers, or worry of messages being blocked.

Open APIs for email and SMS

Businesses can have more control over messaging and branding. Integrate to our customizable Flow and SMS texting APIs – which allow white labeling – so your business can choose the messages you send to customers and brand the entire process for a seamless experience.

Set up a call with a PDCflow Payment and Communication expert today to learn more.

Set up a call:

Want to know more about PDCflow Software?

Press ▶️ to watch our explainer video

REDUCE RISK

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles