Traditional communication methods like telephone calls and paper correspondence are becoming less popular with consumers. As new digital communication methods emerge, consumers expect companies to keep up with tech trends by offering communication methods they most prefer.

Unfortunately, heavily regulated industries like debt collection have been slow to respond to this trend, fearing lawsuits due to non-compliance.

During a PDCflow webinar, Joann Needleman, Clark Hill, John Bedard, Bedard Law Group, and John Chebat, Occupational Management Group, discussed how debt collectors can use text and email right now to better communicate with consumers while remaining compliant.

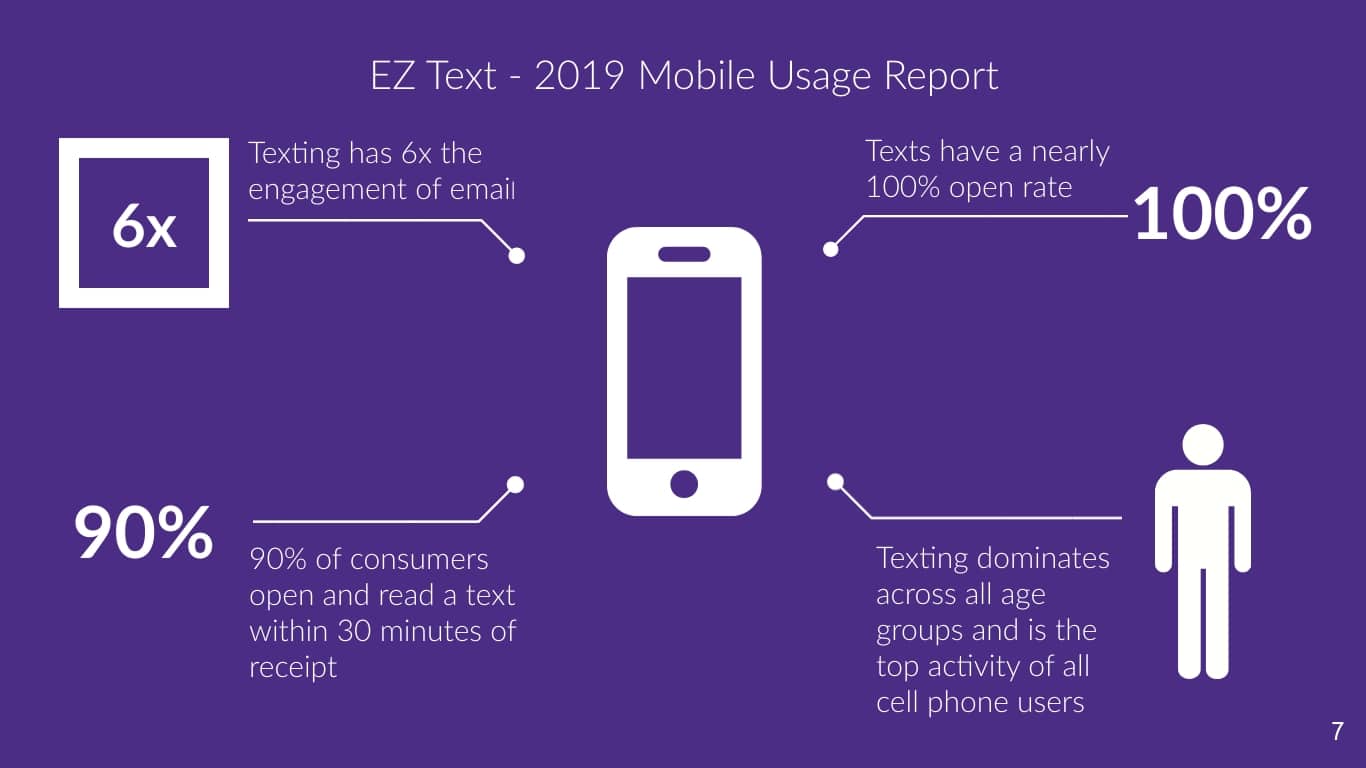

Needleman began the presentation by discussing recent statistics about the effectiveness of digital communication. According to one survey by EZ Text, text messages have a nearly 100% open rate, and nearly 90% of consumers open and read a text within 30 minutes of receipt.

“We can be a lot more strategic in our communications in email and text because they’re being read.”Joann Needleman

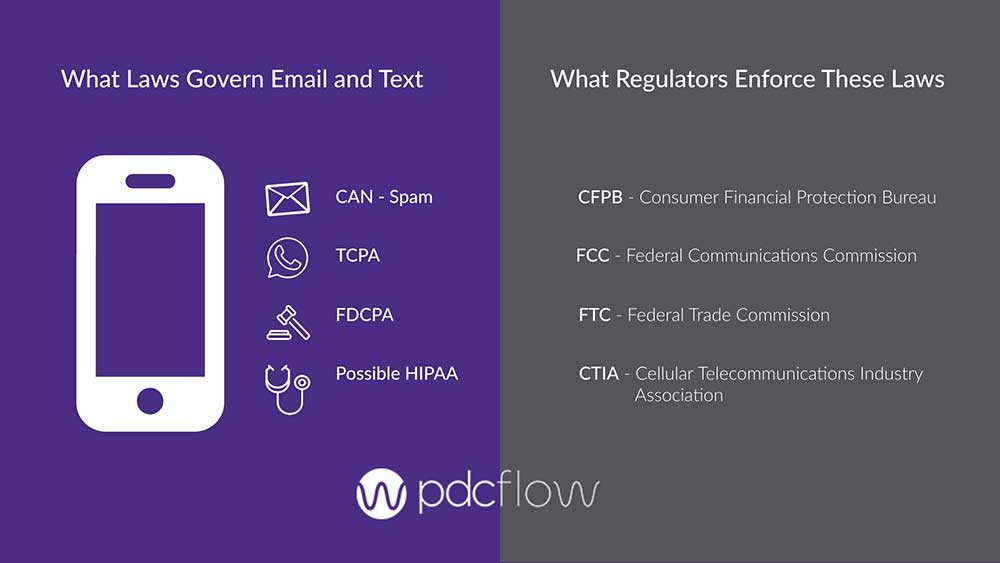

Laws and Regulators Governing Email and Text

Laws

The laws that may apply when incorporating text and email into your debt collection strategy come from a few different sources.

Some apply to the communication method, some to the industry itself and some may apply depending upon the information being sent. The four main laws that likely apply to using text and email are:

- CAN-Spam: FTC has jurisdiction over this law. CAN-Spam mostly addresses promotional emails. An important aspect for all businesses, however, is that you must offer an opt-out or unsubscribe method for consumers.

- TCPA (Telephone Consumer Protection Act): Because a text is considered a call, TCPA applies. If you will be sending mass texts, you must keep TCPA in mind.

- FDCPA (Fair Debt Collection Practice Act) : This applies due to communication with consumers about their debts.

- Possible HIPAA: For those collecting medical debt, HIPAA is an additional concern that should be addressed when considering any communication with consumers.

Laws and Regulators Governing Email and Text

Regulators

There are many different regulators that can take action against a business for violating regulations. Again, they may apply because of the communication method or because the regulating body addresses the actions of those in the industry.

- CFPB (Consumer Financial Protection Bureau): The CFPB’s Regulation F put forth many expectations for collectors using text and email for collection purposes. As the rule has been finalized, it is important to understand your FDCPA compliance responsibilities and the consequences of violation.

- FCC (Federal Communications Commission): This group has authority over the TCPA. Any misuse of text messaging (considered a phone call) can trigger actions by the FCC.

- FFTC (Federal Trade Commission): Shares jurisdiction with the CFPB over consumer financial protection laws. While the FTC cannot make rules for the collection industry it may investigate and take action against collectors.

- CTIA (Cellular Telecommunications Industry Association): The CTIA is not a government entity, but rather a private, self-regulatory entity. If you do not follow their guidelines, instead of legal action, you risk losing the ability to use the technology this group provides. Specifically, the CTIA is responsible for leasing short codes. If you don’t follow their guidelines or use these short codes correctly, they will take away your power to use them.

- HHS (Department of Health and Human Services): This entity applies for those collecting on medical debt. If you do not protect the privacy of consumers in regards to medical history or private information, they have the authority to take action for HIPAA violations.

- Phone Carriers (AT&T, T-Mobile, and Verizon): In an effort to keep text messaging an effective and safe communication channel for consumers, the major phone companies have recently created rules that will impact all brands using this form of communication.

To maintain compliance, you must understand what is expected of you from each of these sources and any others – including state regulators – that may have additional rules you must follow.

“Suffice it to say, there are a lot of people in the government looking over our shoulders when it comes to how we communicate with consumers electronically.”John Bedard

Using Email in Your Debt Collection Strategy

Email defined: For debt collection, an email communication is a writing and must comply with all written correspondence requirements.

The Bureau acknowledged in the NPR that an email is a writing. This means that all the FDCPA requirements that apply to a writing also apply to the use of email in collecting a debt.

Regulators

An appropriate consent policy also provides a sense of legitimacy for your agency that can build trust with consumers wary of being scammed.

Bedard says that it’s helpful when creating these policies to consider why specifically you are asking for consumer consent. What actions are you planning to take by email?

“When I think about consent, I think about it in terms of the channel but I also think about it in terms of everybody else I want permission to communicate with.”John Bedard

OBTAINING EMAIL CONSENT

Consent can be obtained in a few different ways. You may wish to include information for consumer opt-ins on the initial demand letter you send by mail.

You can also gather consent during inbound and outbound calls. You may find it most convenient to add it to your right-party contact procedure.

During the consent process:

- Confirm the email address provided is not a work email address, as work email is often monitored by employers.

- Consider providing an oral disclosure statement to confirm all email actions that may take place (consumer receipt of emails, follow-ups through email, etc.) and provide a written disclosure as well.

- You may want to send a confirmation email or link to confirm email.

- Consider what actions will trigger E-SIGN Act consent to be required and have an appropriate system in place to gather proper E-SIGN consent.

CONTENT OF EMAIL

What should your email contain?

Your email should be addressed to the consumer you are trying to communicate with, and the “from” line should contain the true name of your agency (avoid shortened names or acronyms).

The subject line of your email should include the name of the creditor, the purpose of the email, and the consumer’s account number.

The best course of action is to provide only a partial account number to avoid third party disclosure or data security issues in the event the consumer’s email is hacked.

Within the body of the email, you should include a mini-miranda, a link to a payment portal, and/or to your collection agency’s website.

Needleman stressed the importance of driving consumers back to your agency's website because it can help you gain additional consents to email and allow consumers to take control of selecting their own communication preferences.

Lastly, the email should include an opt-out or unsubscribe option to easily direct consumers to decline further emails.

Using Text Messaging in Your Debt Collection Strategy

TEXT CONSENT AND REVOCATION

Much like email, it is best to gain consent to text while speaking live with the consumer on the phone. During this process, your collectors can verify the mobile number and send an opt-in text while still speaking to the consumer, ensuring the process is complete before concluding the conversation.

Consent can also be gained through your agency’s website, allowing consumers to feel more in control of their preferences.

It is important to understand not only when consumers consent to texting, but also when they do not wish to be contacted. It’s necessary to follow CTIA, TCPA, and Carrier Rule requirements when texting.

- While gathering express consent to receive text messages from your company, you must inform your customers what company will be delivering the text messages.

EXAMPLE

"Since you have asked to receive text messages from our company, please be aware that those text messages will be delivered for us by PDCflow."

- You must record and retain each and every prior express consent obtained. Keep records in a secure and accessible location. PDCflow requires a retention period of 4 years and requires customers to be able to provide records of prior express consent to PDCflow upon request.

Revocation should be offered at any reasonable time, place or manner for those wishing to discontinue communication by text and you must take action to stop texting them as soon as reasonably possible.

- If a recipient opts out (if they revoke their consent) then you must obtain renewed consent before sending that person an SMS text again.

TEXT MESSAGE CONTENT

If your company doesn't follow carrier rules the consequences may include increased blocked text message rates and even being dropped from carrier service. Plus violating TCPA and FDCPA rules can have severe legal consequences.

An initial text message to a recipient should contain the following information:

- Your company name.

- The reason you are sending the message. This reason should be the same one given to the recipient while gathering their express prior consent to send communication via text message.

- Indication of who is sending the text (our SMS vendor's name if you're using one).

- A STOP statement.

EXAMPLE

“{firstName} {lastName}, {companyName} wants to send you PDCflow smart requests so that you can complete electronic transactions: text YES to receive these requests. Msg&data rates may apply. Reply STOP to opt-out anytime.”

Subsequent messages to a recipient should contain:

- Your company’s name

- The reason you are sending the message (this reason should be the same reason given to the recipient while gathering their express prior consent to send communication via text message)

- Indication of who is sending the text (your SMS vendor’s name if you’re using one)

EXAMPLE

"{firstName}{lastName}, {companyName} sent you a PDCflow smart request "{FLOW Title}" to complete: {link}”

“The penetration rates are just so dramatically different than these traditional communication channels that we have been used to for decades. It really makes me approach from a different perspective how to utilize these channels.”John Bedard

One Debt Collection Agency’s Story

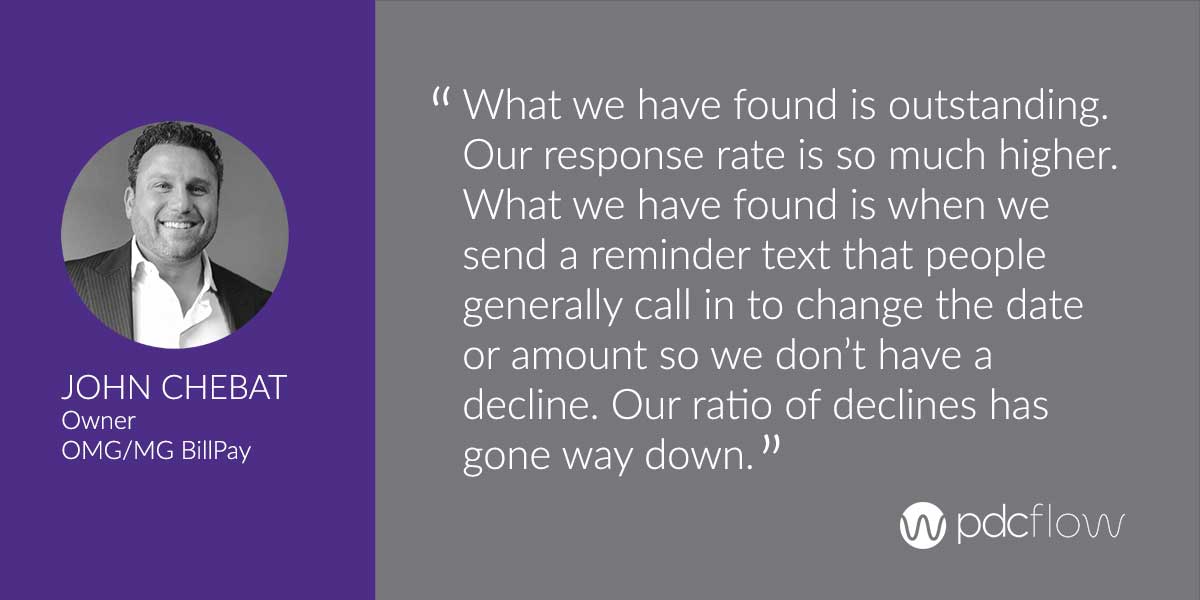

Occupational Management Group (OMG) uses a PDCflow API integration to use Flow Technology within their collection software. Chebat spent his portion of the presentation discussing how text messaging has worked for him within his agency through this integration and the results he has seen.

Chebat explains that after gaining verbal consent, OMG uses texting to send documents to consumers after a payment arrangement has been reached (while they are still on the phone).

After a transaction is complete, it generates an audit trail. This report can be accessed by authorized personnel at OMG at any time in the future to reference key transaction details:

- Consumer cell phone number

- Time/date stamp on the transaction

- Geolocation of the consumer completing the transaction

The typical items OMG sends to consumers include:

- Letters

- Recurring Schedule Agreements

- Settlement Agreements and/or Paid in Fulls

Each consumer:

- Receives the agreement in real-time while still on the phone with the agent

- Can open, read, digitally sign, return the agreement and authorize a payment transaction within seconds

- Can request a copy of the transaction details. The agreement and audit trail is also stored in the Blue Chip software indefinitely

OMG’S RESULTS

OMG has seen several improvements in the collection process due to implementing text messaging.

- Higher Response Rate - Sending payment reminders to consumers has improved the rate of consumers reaching out to change or update payment information.

Chebat says this response rate has also led to more successful payments throughout payment schedules. “Our ratio of declines has gone way down.”

- 50% Decrease in Chargebacks - “Because this is done in writing and because there's action taken by the consumer to read the letter, to actually understand the letter, to be part of the process, we found that chargebacks have gone down by more than 50 percent,” says Chebat.

- Fewer Miscommunications and Complaints- Incorporating texts into the larger debt collection strategy has cut down on miscommunications and complaints that sometimes occur during payment negotiation. Consumers prefer texting, and it allows for a more immediate transfer of data. This means consumers can review or correct information immediately.

OMG Flow Results

95% Flow Delivery Rate

80% Flow Completion Rate

Implementing text messaging and email in your debt collection strategy can have great benefits. Be sure you prepare your agency and understand the compliance requirements you must follow.

Now that the CFPB has finalized Regulation F, agencies can use email and text to engage, communicate, and accept payments from consumers.

PDCflow for Email, Text and Payments

PDCflow’s Flow Technology lets agencies reach consumers through email and SMS. Send a text message, email–or both–for all kinds of payment communications, including:

- Sending a validation notice

- Sending a payment request

- Providing documents for review (agents can do so while still on the phone live with a consumer so they can review them together)

- Sending documents to be digitally signed and returned

- Requesting photos (like IDs or insurance cards) to be uploaded and sent back

- Sending payment reminders on recurring payment schedules

Along with Flow Technology’s email and text channels, PDCflow’s payment processing software can help your agency better manage your payments.

- Accept credit, debit or HSA card payments as well as ACH

- Keep payment details secure with data encryption, tokenization and storage

- Set up groups, locations or multiple merchant accounts, so you can keep all of your lines of business separate from one another

- Monitor performance with our robust Insights Reporting

For more information on using PDCflow to manage payments, streamline workflows and reduce costs, sign up for a demo with a PDCflow Payment Expert today.

Request a Demo:

Want to know more about PDCflow Software?

Press ▶️ to watch our explainer video

REDUCE RISK

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles