SURVEY SAYS:

Why Customers Make Payments Over the Phone

Convenience

Allowing customers to pay the way they want is convenient. Some may not like online payment pages or have a complex problem that can’t be solved by looking at the resources on your website.

Others might find it difficult to navigate self-serve options or don’t have a reliable way to access them when a payment is due. Companies should take payments over the phone to offer convenient options for every situation.

Personalized service

Speed

Accessibility

Perceived Security

Regulations like Payment Card Industry (PCI) standards govern how organizations accept, process and manage credit card information. Every merchant who accepts card payments must know these requirements but most customers don’t know about PCI compliance.

Although taking payments over the phone can open your company to risk, some customers may not trust an online payment system or other automated payment options. Companies should take phone payments securely to keep customer data safe.

Why Companies Take Payments Over the Phone

Revenue increase

Accuracy

People make mistakes. Customers might type in their payment information wrong or miss a required field during an online payment and become frustrated with the process.

When agents take payments over the phone, they can stand by during transactions to make sure they process correctly. Staff can address problems immediately and provide immediate customer support.

Customer service

SURVEY SAYS:

Limitations to Taking Payments Over the Phone

Fear of fraud

Just as some customers may think it’s safer to trust their data to an agent, others will worry about reading payment information out loud. After all, customers don’t know who is on the other end of the transaction and don’t know how information is stored.

Your organization should follow PCI compliance for card payments and Nacha regulations for ACH transactions.

Your company should also block employees from hearing, seeing or accessing private payment data (during transactions and afterwards). This prevents data breaches and increases trust in your business.

Human error

Customer service representatives also run the risk of typing payment data incorrectly, accessing the wrong files, or sending incorrect information to a customer. This can harm your business reputation and cause problems during payment reconciliation.

To take payments over the phone, use payment software that creates safeguards and prevents errors from occurring by:

- limiting staff access to only the information they need

- storing payment data so your company can manage risk

- allowing customers to key in their own payment information while still on the phone with an agent

Customer dissatisfaction

Credit Card Payment Security and Compliance Risks

Accepting credit card payments over the phone means your company must follow PCI compliance requirements. Specifically, your organization can not use voice recording software that might capture and store payment data from a customer’s transaction.

Simply allowing staff to hear card numbers can also expose your company to more risk. If an employee writes a credit card number on a piece of paper, that paper becomes a liability for your organization – especially if you allow agents to work from home.

Fast, Secure, Compliant Phone Payments With Flow Technology

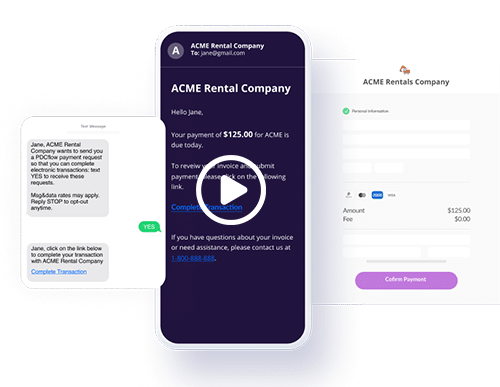

PDCflow’s Flow Technology is a delivery system that lets agents send a text message or email to customers while they are still on the phone with an agent.

Customers can open the message, key in their card or bank account information and complete a payment – all while they’re still on the line with your staff.

Because Flow Technology prevents agents from having to key in payment numbers, customers can enjoy a personal touch without worrying about fraud or mishandled data.

Organization hierarchies in PDCflow’s software also allow administrators to choose who can access workflows, templates or other information in the system. This can be segmented by group, department or location to avoid confusion and human errors.

For more information on how to take secure agent-assisted payments, even with remote workers, request a demo with a PDCflow payment expert today.

Request a Demo:

Want to know more about PDCflow Software?

Press ▶️ to watch our explainer video

ONE-STEP PROCESS

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles