The CFPB Notice of Proposed Rulemaking (NPR) has been covered extensively in articles and webinars over the past few months. The prospect of using text and email messages is exciting for an industry that has been all but left out of using the latest technology.

The question is, how will you use digital communication safely?

Here are a few common concerns about digital communication and a few of the Bureau’s proposed safe harbors addressing them.

Third Party Disclosure Safe Harbor

From survey responses and in speaking with clients, we have learned that the most prevalent concern with using text messaging and email is the possibility of third party disclosure. Under the proposed rule, this would no longer be a worry.

The fact that the collection agency’s name or information about a debt appears in a message is not “unfair or unconscionable” under the proposed rule. The information contained in the email or text message is intended for personal communication.

The consumer has control over what messages are opened when, and who can see them. If someone is standing over their shoulder reading a personal message, that is the consumer’s fault.

Using debt information in text or email communication would be a safe harbor under 1006.22 as long as you follow the suggested “reasonable procedures” in 1006.6.

Right Party Contact Safe Harbor

The right party contact requirement that may be a little trickier is that your agency must have reasonable procedures in place to ensure that a message is going to the correct consumer. Email addresses and cell phone numbers can be exchanged and recycled quickly.

To address this risk, the proposed rule offers a safe harbor for an incorrect email or phone number that the consumer used to contact the agency under the term “recently used.”

The CFPB has yet to define “recently used,” so this subject still requires further clarification.

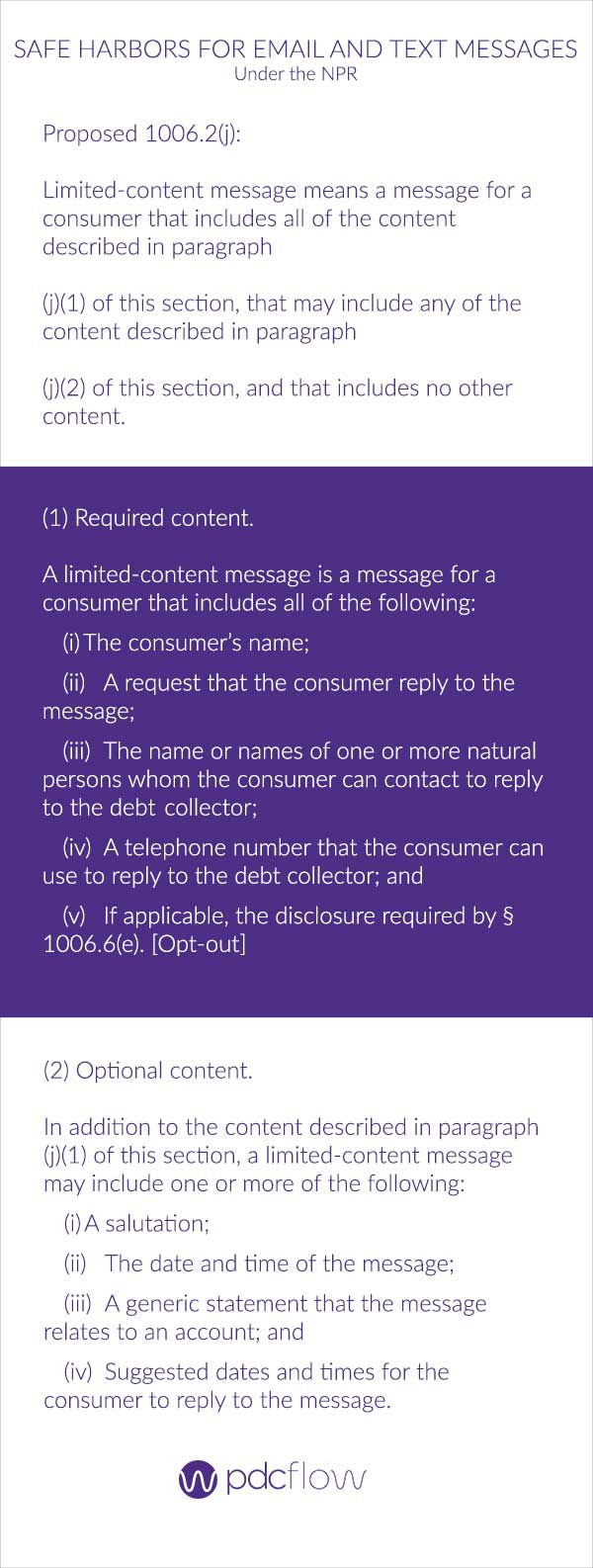

Limited Content Messages Safe Harbor

Another safe harbor for text messages (not for email) is the Limited Content Message. If you follow the prescribed message exactly, it is a safe harbor and you can not be sued for an FDCPA violation if this portion of the rule becomes final.

Keep in mind, however, that text messaging is also subject to the TCPA.

Time and Location Safe Harbor

Given the mobile nature of cell phones and the fact that email and texts are both retrievable on cell phones, it is likely that common messages will end up on a cell phone.

While you don’t need to worry about delivery time for emails, the text message is still viewed as a “call” and is subject to the FDCPA as well as the TCPA.

Under the FDCPA the proposed rule provides a safe harbor for time and location issues that says “the debt collector would comply if the debt collector communicated or attempted to communicate with the consumer at a time that would be convenient in all of the locations at which the debt collector’s information indicated the consumer might be located.”

Electronic Validation Notice Safe Harbor

There are a few procedural issues in the NPR dedicated to the electronic delivery of the validation notice and other required disclosures that are not entirely clear.

The NPR explains how E-Sign Act consent comes into play for the required disclosures. However, the FDCPA states that the validation notice is required within 5 days IF the information is not contained in the first communication.

This may mean that electronic delivery of the validation notice is permitted under normal electronic communication consent. Hopefully, this and a few other questions will become more clear in the final rule.

Although the new rule will clarify certain uses and safe harbors that come with new technologies, PDCflow’s text messaging and email software can be integrated into your debt collection strategy for many uses today.

Subscribe to our weekly updates or monthly newsletter to get actionable insights, tactics, and expert advice to improve the payment experience for your customers and create a better cash flow.

Subscribe:

Want to know more about PDCflow Software?

Press ▶️ to watch our explainer video

REDUCE RISK

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles