The Difference Between First Party and Third Party Collections

First party collection means you are collecting late payments on behalf of your client under their branding – before accounts become bad debt. This type of collection is a good business expansion strategy for agencies, which often have insight and experience clients lack.

However, collecting from consumers who are not yet in the bad debt phase brings its own set of challenges and workflows. Agencies and EBOs may find themselves handling:

- Early intervention strategies

- Charity care

- Financial assistance questions

- Billing issues or complaints

- Other customer service activities not always tied to collecting a payment

How to Incorporate First Party Collections into your Agency

Using Separate Processes

You must separate customer-facing touch points from those in your third party process, as well as where collected funds end up. Here are just some of the areas where processes must be separated.

Phone systems and addresses

You shouldn’t route third party consumers through the same systems as first party customers or patients. Because you will be collecting on behalf of a client under their name, you should keep these systems separate.

Also, be careful to use the correct address on letters, receipts or other customer-facing communications. If your address doesn’t match the company name consumers are expecting, they may think your collection activities are a scam.

How you represent your name

Make sure agents, letters, receipts and other customer-facing interactions reflect your creditor client. Again, it’s essential to maintain the trust consumers have in your client.

This means you should provide a seamless experience, so customers or patients don’t question your motives or become distrustful of your business, agents or the original creditor.

Where collected money goes

Where you hold funds after payment collection is an important consideration. First party or EBO businesses may choose to use separate merchant accounts for different purposes, or even use the client’s payment portal to collect payments.

Considerations Before Starting Your Business Expansion

Software Tools for Organized Processes

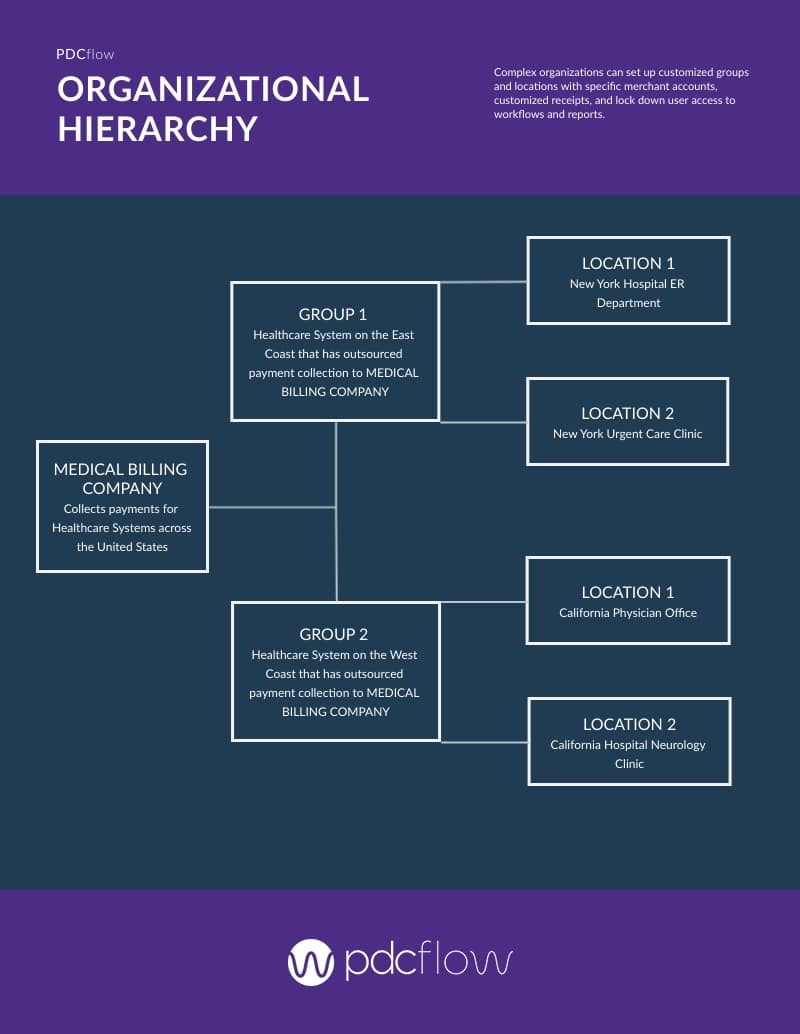

Debt collection agencies can easily run different lines of business if compliance and logistical considerations are in place. Software tools like PDCflow’s Organizational Hierarchy can help you keep workflows and merchant accounts separate.

Companies that process third party, first party or medical billing transactions can set up different merchant accounts where settlements are routed if they want to keep things separate for reconciliation purposes. This is also needed to ensure the correct DBAs (“doing business as” names) are displayed on a consumer’s bank statement.

Most merchants are required to have a separate account for medical processing by their Merchant Service Providers (MSPs). The rule of thumb is that a merchant should process at least 80 percent of total processing in a strictly medical billing merchant account in order to gain approval for the medical Merchant Category Code (MCC) to process medical cards (HSA, FSA).

PDCflow’s payment processing software offers organizational features that help accounts receivable professionals:

- Manage more than one merchant account from the same system

- Separate payment collection efforts by group or location

- Grant or deny staff access to accounts to avoid human error

In-House Experts

Having an expert on staff will greatly increase your likelihood of success during business expansion into an early out collection model. Do you have first party experts in your organization?

If you don’t have someone who can take this on, it’s time to hire a new staff member. You’ll want a subject matter expert who can help create training materials and standard operating procedures, lead training sessions, etc.

Common Types of Early Out

Many industries could benefit from hiring an early out collection team to recover more revenue. A few of the main types of debt you’ll find yourself collecting on may include unpaid loans or credit card bills, lines of credit and mortgages.

Healthcare

In addition to the list above, a large portion of early out business comes from the healthcare industry. If your agency is ready to take the first step towards expanding your collection business, begin by choosing which types of clients you will pursue, such as:

- Hospitals

- Physician offices

- Labs

- Ambulatory care

Early Out Compliance Concerns

No matter what industry you work in, there will always be regulations to follow. In the case of early out collection, you should understand basic payment compliance rules to keep data safe.

In addition, you’ll likely find yourself needing to understand other compliance rules that may impact your clients and their consumers.

Keeping a HIPAA compliance expert on staff and running proposed workflows past your company’s attorney are steps you should not skip when creating your expansion strategy.

Client Relationships

Remember, creditors are turning to you for help because they can’t collect on their own. This can be due to lack of experience, in-house tools or resources like time and staff.

To grow as a company, you need to learn to work with clients as an early out business. You must be clear in client contracts about what services you’re willing to provide. You can use unique services as a selling point, or even include software tools, analytics or other capabilities to entice new clients.

Off Contract Work

Oftentimes, clients will make requests not outlined in a contract. While tacking on special requests may not always be a bad idea, employees can become overwhelmed with the amount of work you’ve agreed to. Only you know what is best for your business.

Keep an open dialogue internally with agents and management as well as externally with the clients themselves. Be clear and realistic about what your team can – and more importantly can’t – accomplish. A clear understanding from the start eliminates doing work for free or even spending money completing early out work.

In first party collection, as with all other aspects, in-house counsel and subject matter experts can strengthen your organization by giving you advice and protecting your company from risk. In addition, you should stay informed of industry trends, implementation strategies and new technologies that will help your business grow.

For more accounts receivable news and content like this, to help you win business, increase efficiency, and take more payments, subscribe to the PDCflow blog.

Subscribe to the PDCflow Blog

Want to know more about PDCflow Software?

Press ▶️ to watch our explainer video

REDUCE RISK

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles