Time is money. This is especially true for financial transactions between companies, where delays cause significant losses and missed opportunities.

By eliminating the hurdles of traditional payment methods, business-to-business Automated Clearing House (B2B ACH) payments create a swift, secure way to navigate modern business operations.

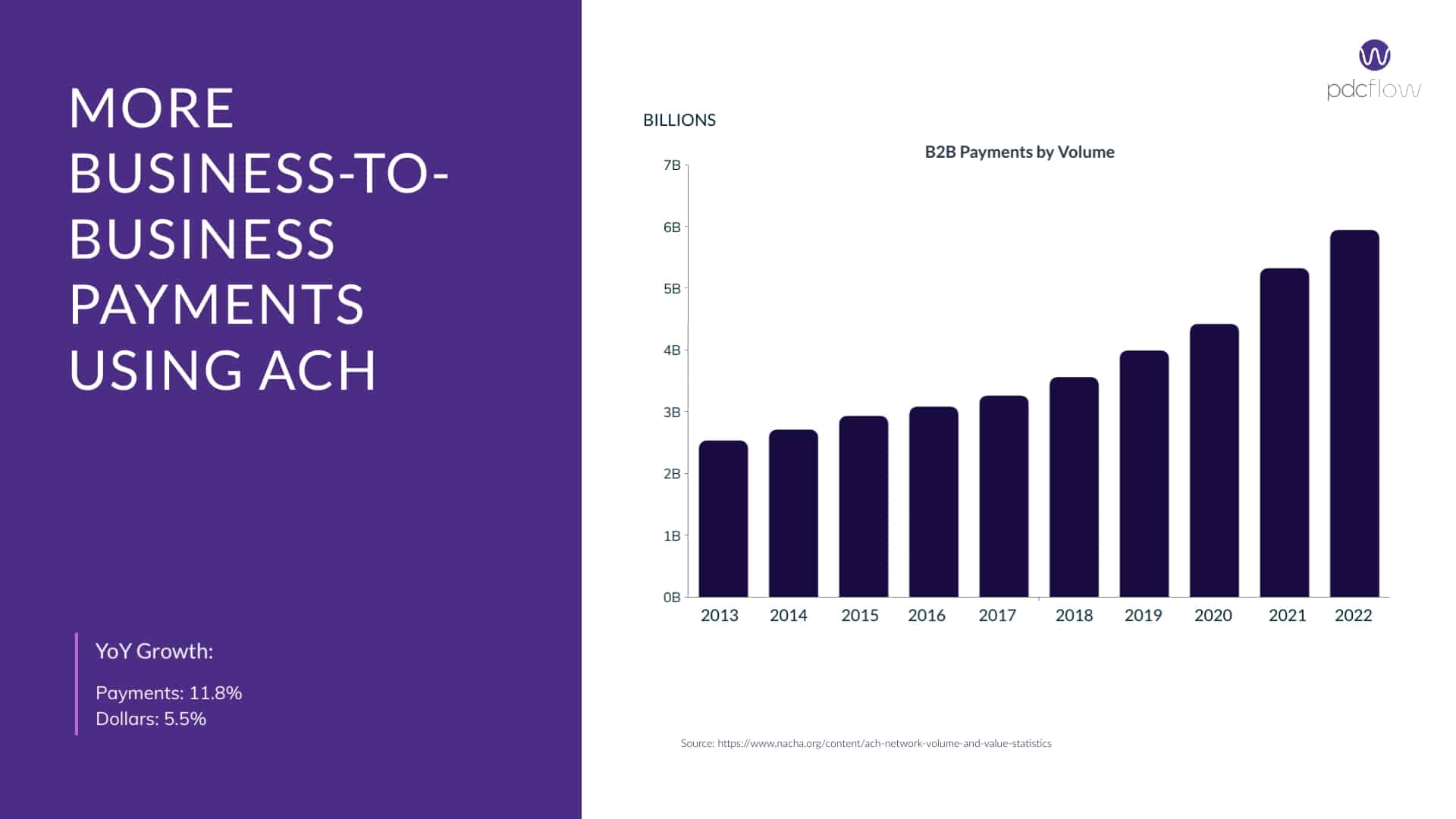

Business to Business ACH Debit Transactions

B2B ACH refers to electronic payments made through an automated clearing house network – these are often facilitated by banks or other financial institutions acting as intermediaries.

They create a digital plaza where businesses can securely initiate transactions with each other without having to deal with physical checks, wire transfers or credit card fees.

Importance of B2B ACH in the Modern Business Landscape

Traditional transaction channels create delays; whether that’s waiting days for checks to clear, or navigating through several intermediaries before your transaction reaches its destination.

Companies need methods for modern, fast-paced, streamlined transactions.

With this surge towards a digital society, embracing B2B ACH represents a company that is ready for the future: one efficient at handling large volume payments while maintaining security and reliability.

Why Business to Business ACH Transactions?

Efficient, Streamlined Payment Process

One benefit of business to business ACH is to simplify business workflows. Electronic ACH bank transfers eliminate the need for:

- Waiting for a check to arrive in the mail

- Extra trips to the post office to collect check payments

- Repeated calls with customers after a check doesn’t arrive

- Manual reconciliation efforts

Instead, business ACH payments speed up transaction times by managing and scheduling payments directly between bank accounts in minutes.

As a result, both payers and payees experience quicker access to funds.

Automated B2B ACH payments also make recurring payment schedules simple to create and manage, with little to no intervention after setup.

Automation cuts down on error-prone manual processes. It saves time fixing mistakes and makes offices run more efficiently, while providing reliable payment processing experiences.

Coupled with real-time tracking capabilities of most ACH gateways, organizations gain control over finances, reporting, and reconciliation.

Cost Savings

The cost savings gained from processing ACH transactions is a big advantage. Compared to other methods like card processing or accepting paper checks, ACH processing is often less expensive for businesses. This is because ACH transactions:

- Come with lower processing costs - ACH processing costs are typically lower than those associated with credit card processing.

- Cause fewer surprise fees - When a company accepts paper checks, there is no guarantee that payments will go through. Using account validation like PDCflow’s ACH Verify makes it easy to pre-verify bank account details before a payment is submitted. This eliminates paying return fees associated with a bad check.

- Save time - Companies that take paper checks spend longer waiting on payments to arrive in the mail. Then, they must wait even longer after cashing these checks for the funds to end up in a merchant account. Processing B2B ACH transactions online is faster and easier, from beginning to end.

Enhanced Security for Financial Transactions

Payment encryption and tokenization in your ACH system are essential security measures. They mask important payment details to create a line of defense against fraudulent activities and data breaches. Your payment software should do this for you.

In addition, taking online ACH payments through self-serve channels keeps payment details private, even from the payment recipient.

Giving out bank details isn't necessary when doing business ACH transactions because the payer can enter their own information for a transaction – no need to read a bank account and routing number out loud to an agent.

These secure B2B ACH features not only combat fraud but also cultivate trust among business partners, enhancing relationships and meeting stringent industry standards.

Challenges Implementing B2B ACH Processing

Integration with Existing Accounting and Financial Systems

Many businesses now use proprietary systems or have an existing CRM or accounting infrastructure that can’t be changed just to accommodate payments.

To get full use of business ACH payments and reporting alongside current systems of record, companies will need to integrate using APIs. This will add payment functionality into existing accounting systems.

Open APIs should offer:

- Support from developers - Using APIs should be straightforward, but sometimes questions come up. You should be able to reach the software developers for a sandbox account or to answer questions as you integrate.

- Low-code options - APIs that are low-code make projects go faster, so companies can begin taking business to business payments as soon as possible.

- Drop-in components - Integrating B2B ACH payments shouldn’t be a long, hard, arduous process. Drop-in integrations make work faster and simpler.

While APIs should make the process simple, corporate ACH payment integration requires thorough analysis.

Organizations need an understanding of existing structures, procedures, and software capabilities, and a project manager who can oversee the integration process.

Compliance, Regulatory Requirements, and Industry Standards

The payment processing landscape is governed by many rules and standards.

These are dictated by both the government (through rules like the EFTA’s Regulation E) and through independent organizations (like the National Automated Clearing House Association, Nacha, which oversees all US ACH transactions).

For any organization that uses B2B ACH payments, adhering to these requirements is non-negotiable.

Following payment compliance:

- increases the likelihood of legitimate transactions

- reduces (and often eliminates) bad transactions

- keeps companies from being fined and otherwise penalized for noncompliance

Before implementing a Business to Business ACH platform into their operations, companies have to ensure they understand these laws and rules thoroughly.

Risks Associated with Fraud and Data Breaches

As convenient as B2B ACH transactions are for ease-of-business, they aren't completely immune from risks of fraud or data breaches — a concern frequently seen in digital channels.

This is why companies need security protocols and continuous monitoring of corporate ACH payment environments.

Businesses have to prioritize protection against cyber threats and fraud while ensuring they have preventive measures and contingency plans in place.

Often, payment vendors manage data storage and provide payment security features that address these concerns.

Impact on Customer Relationships and Satisfaction

Don’t overlook the importance of customer satisfaction when adopting B2B ACH payments.

Your clients are essential in every Business to Business ACH transaction and their user experience shouldn't be ignored.

Businesses need to create a friction-free process for customers who might feel uneasy about changing from traditional methods, like cutting a paper check.

ACH payment software should make digital payments faster, easy to use and create a safe, secure environment.

Want faster customer payment cycles and better payment processing transparency?

How Can Businesses Implement B2B ACH Processing?

Digital business ACH payments enhance workflows for both payers and payment recipients.

But many companies worry about the steps required to incorporate ACH processing into their operations.

The following section will guide you through some key considerations and successful practices to implement B2B ACH processing.

Choosing a B2B ACH Payment Processing Vendor

Finding a suitable provider for your corporate ACH payment service is a critical step. Here's a straightforward process you can follow to make the right payment vendor choice:

- Identify Your Needs: Outline what you expect from your business to business ACH provider in terms of support, cost-effectiveness, integration needs, and security features.

- Research Potential Vendors: Look at testimonials and case studies on vendor websites, and visit review sites like G2. This feedback directly from other customers gives a starting point for what to look for and expect in different companies.

- Compare Shortlisted Options: Make comparisons based on price, efficiency of the system, and integration options.

- Request Demos or Trials: Get a tailored, one-on-one demonstration of how the software functions. This gives companies a way to picture how the system will enhance current processes or replace existing inefficiencies.

Remember that while cost matters, don't let it overshadow other crucial factors like functionality, system uptime, and reliable customer support.

PDCflow’s Essential Features and Functions for B2B ACH Payment Processing

PDCflow is an all-in-one payment and document management software companies use for faster payments, simplified office processes, and built-in payment compliance.

Take B2B ACH payments safely and efficiently with features like:

- Payment information encryption - PDCflow encrypts all payment information.

- Bank account detail tokenization - PDCflow tokenizes all bank account numbers.

- ACH verify - ACH Verify allows companies to test a bank account’s validity before officially submitting a transaction. This prevents declined and returned payments.

- Nacha compliance - PDCflow follows Nacha guidelines and processes ACH transactions in accordance with their rules.

- Open APIs - PDCflow’s payment APIs are a fast, low-code way to add payment and digital communication functionality into your existing systems.

- Multiple ACH processor options - PDCflow works with an extensive list of ACH processors, so companies can choose the best fit for their business.

- Email and text message payment requests - PDCflow’s Flow Technology allows companies to send documents, along with payment, esignature, and photo requests, all in one email or text. The recipient just has to open the message, follow the prompts, and fill in payment details.

This streamlined process increases cash flow, drives timely service delivery, and keeps businesses ahead of the competition.

Adapting to these modern trends could have tremendous benefits for businesses in improving efficiency, security and user experience associated with B2B ACH Payments.

Learn more about taking ACH payments through PDCflow. Request a call from a PDCflow Payment Expert today.

Request a Call:

Want to know more about PDCflow Software?

Press ▶️ to watch our explainer video

ONE-STEP PROCESS

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles