Debt collection letters are a central part of a collection agency's compliance management system.

However, the California Association of Collectors (CAC) 2017 Collection Boot Camp panel, Courtney Reynaud, Shawn Suhr, Kelly Parsons-O’Brien (agency owners) and June Coleman (attorney), recognize the potential liabilities inherent in drafting collection letters.

Their combined expertise and Coleman’s legal know-how as the CAC’s MAP attorney provided insight and in-depth information on how to write a compliant debt validation notice.

Collection Letter Format: What to Watch Out For

Section 809 (b) of the FDCPA states that “any collection activities and communication during the 30-day period may not overshadow or be inconsistent with the disclosure of the consumer’s right to dispute the debt or request the name and address of the original creditor.”

This language leaves much room for interpretation, which can be difficult for agencies attempting to draft a collection agency letter template.

Be aware that a wide variety of items can be considered as overshadowing, including sending a second collection letter within the 30-day period that requests the debtor act before the 30-day period ends.

Similarly, if a letter makes reference to disputing a debt during the 30 days, this reference may be seen as overshadowing the language that directs the debtor to dispute in writing.

Below are some of the most common formatting and language mistakes that can leave debt collection agencies open to legal action.

According to the CFPB, overshadowing the rights of consumers to dispute or request original-creditor information is prohibitied.

During the validation period, a debt collector must not engage in any collection activities or communications that overshadow or are inconsistent with the disclosure of the consumer’s rights to dispute the debt and to request the name and address of the original creditor.

Source: Consumer Financial Protection Bureau

OVERSHADOWING

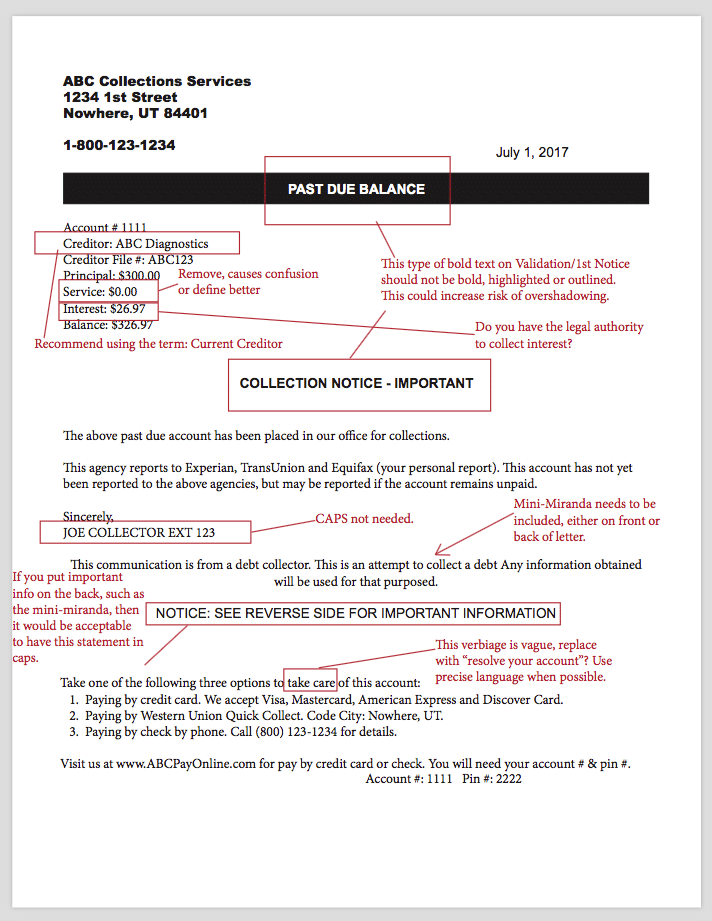

Avoid bolded or highlighted text on your first notices.

Bolding or highlighting text you deem important might seem harmless. You may even feel you are helping the consumer by making the letter easy to read. But the truth is, too much bold or highlighted text can cause overshadowing, and take attention away from other important elements of the letter.

Use CAPS LOCK with caution on your first notices.

Just as with the first tip, you must be careful of using all caps in your letters. Anything that may overshadow the main point of the notice is likely to cause issues.

Avoid statements that may overshadow the consumer’s right to a 30-day validation period. Avoid deadlines that fall within the 30 days.

The 30-day debt validation period of a first notice is extremely important. Consumers must be able to understand they are allowed to dispute their debt within this time frame. If anything in your collection letter confuses this point or draws attention away from it, you are at risk of violating the FDCPA’s rules, and may get sued.

For instance, you should avoid extending a debt settlement offer with a deadline to accept within the 30-day period because this would overshadow the consumer’s right to validate throughout the 30-day period.

SIMPLIFY WHEN POSSIBLE

Use verbiage and wording on notices that are easy for the consumer to understand.

Your consumers might not have any previous experience with debt collection, and most people probably won’t understand technical industry terms. It is important to write your notices in plain language that the least sophisticated consumer can easily read and understand.

The term “current creditor” should be used to identify who the agency is collecting the debt on behalf of.

During the CAC webinar, Coleman referred to a case she was directly involved with on this topic. In that case, the plaintiff’s attorney argued that the least sophisticated consumer could not tell whether the bill was sent on behalf of the current creditor because the letter only referenced “creditor.”

The Plaintiff admitted that he knew the creditor referenced in the letter was the current creditor. Nonetheless, the Court awarded judgment to Plaintiff on this issue.

Because this is such an easy fix, Coleman cautions that it is worth playing it safe by using the term “current creditor.” After all, it’s better than dealing with the expense of defending a lawsuit.

Don’t add a service fee line if no fee is being collected.

Having a service fee line included in a letter when the fee is $0.00 raises questions for the consumer. Is the service fee always going to be $0.00 or will it increase in the future?

Also, a service fee may or may not be allowed under state law, depending upon which states your agency is collecting in.

Coleman advises clients not to represent that an agency has added any additional fees to the amount of the debt owed. Rather, they should state that fees or interest have been added by operation of the law.

Do not add interest to the balance unless you have the authority.

Be certain that under the law, your agency or your client has the authority to collect interest on a debt owed. Make sure you understand the legal authority for the interest, and you have your client’s authority that interest will increase the amount of the debt.

Debt Collection Letter Example

KEEP STATUTORY LANGUAGE INTACT

When statutory language is required, don’t ad-lib or adjust the language. Use exact verbiage of the statutory text.

The statutory language on collection notices should never be changed. While it may seem harmless to adjust or reword what this language says, you risk distorting or omitting important sections that must be communicated to your consumers. Never change this language.

Must include the mini-miranda.

This can be on the front of the letter or on the back of the letter. If you choose to place it on the back of the letter, you must place a notice on the front directing the consumer to see the reverse side for important information.

Email and Text Collection Letters

With the passage of Regulation F in 2019, the CFPB laid the foundation for compliant electronic communications.

Debt collection agencies can now send the debt validation notice and other collection letters, such as a settlement letter, via email and SMS.

Considerations that agencies need to plan for include:

CONSENT

FORMAT

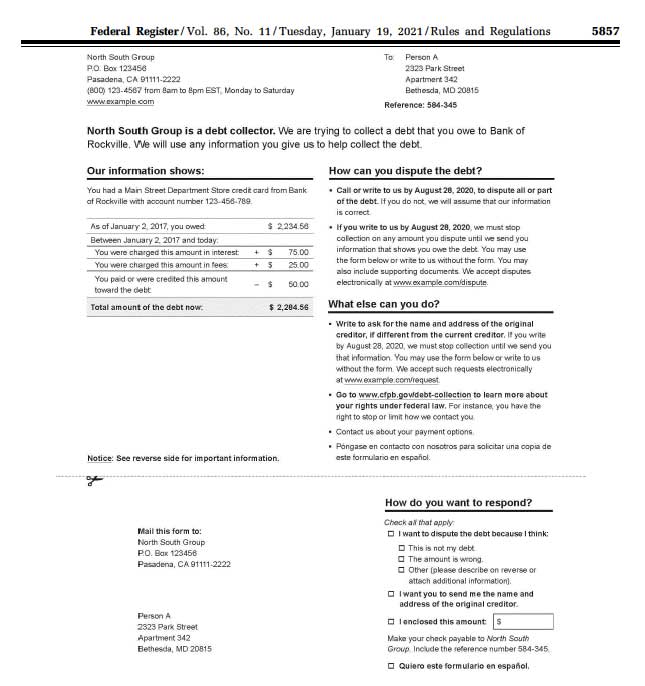

For safe harbor to apply, your agency must make sure your validation notice is substantially similar to the one outlined in Regulation F. There isn’t an exact definition of what this means, and will be left up to courts to determine.

That’s why it’s best to follow the model Form B-1 as closely as possible to prevent this type of a challenge. Remember, your ultimate goal as a debt collection agency is to avoid lawsuits. Following the model validation notice as closely as possible is the best way to do so.

Sample Model Form B-1

Collection Letter Review

After you’ve formatted your letters, there’s one more step you should take before sending them to consumers.

Coleman strongly recommends that every collection letter an agency distributes — whether via traditional mail or through digital channels — should first be reviewed by a lawyer.

Attorneys can catch problem language or missing items that your office might not notice, which will minimize your risk of being sued. The extra effort it takes for your agency to create a compliant collection letter and communication process can prove invaluable in the future.

Get actionable insights, tactics and expert advice to improve the payment experience and create a better cash flow delivered straight to your inbox. Sign up for weekly updates or our monthly newsletter.

Sign up:

Want to know more about PDCflow Software?

Press ▶️ to watch our explainer video

REDUCE RISK

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles