This article was written by Joann Needleman, Ann E. Lemmo, and Leslie C. Bender. It was originally published by Clark Hill Law and is republished here with permission.

On Dec. 18, the Consumer Financial Protection Bureau (“CFPB” or “Bureau”) completed its seven-year rulemaking process for debt collection. In 2013, the CFPB embarked on an ambitious journey to write regulations to interpret the 40-year-old Fair Debt Collections Practices Act (“FDCPA”).

Until the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) was passed, no federal regulator had the authority to interpret the FDCPA through rule writing. The Dodd-Frank Act expressly paved the way for a federal regulator, the CFPB, to take a look at what it regarded as evidence of “abusive, deceptive, and unfair debt collection practices” and to interpret appropriate features of the FDCPA through rule writing.

CFPB Debt Collection Rulemaking Process

The broad range of industries supported by debt collectors and collections activities, like the debt collection industry itself, is complex. In the final part of Regulation F (the “Disclosure Focused Rule” or Part 2), the CFPB reports it has used much of the past seven years researching consumer inquiries and “qualitative” and “quantitative” focus groups in developing a model collection notice, something the credit and collections industry has requested from federal regulators for decades.

Like Part One of the Rule which was released on Oct. 30, (both Parts collectively referred to as the “Rule” or “Final Rule”), each segment of the Rule shares an enforcement date of Nov. 30, 2021. The well thought out events leading to the final Rule include an Advanced Notice of Proposed Rulemaking (ANPR) in 2013, an Outline of Proposal and Small Business Review Panel in 2016, a Notice of Proposed Rulemaking in 2019, and finally the issuance of Parts One and Two of the Rule on Oct. 30, 2020, and Dec.18, 2020, respectively.

As noted in our Nov. 2 alert, Part One of the Rule focused on debt collection communications, including the use of electronic communications when contacting consumers.

Part Two of the Final Rule referred to here as the “Disclosure Focused Rule” implements FDCPA requirements regarding certain disclosures that must be made to consumers during the debt collection process. The Bureau however withdrew a proposal which would have required a debt collector to make letter disclosures about whether a debt is time-barred upon evaluating all the public commentary.

Summary of Disclosure Focused Rule

A summary of these Disclosure Focused Rule disclosures and restrictions are as follows:

Time-Barred Debt

The CFPB has interpreted the FDCPA to prohibit debt collectors from taking or threatening any legal action on a debt where, under state law, the statute of limitation has expired. This is a strict liability standard.

The CFPB expressly defers to state laws for determining whether or not statutes of limitations have lapsed causing the use of legal or other means to collect to be “time barred.” Many states already require debt collectors to disclose whether or not a state statute of limitations has run in regard to a particular debt, and the Bureau’s approach respects state law in this area.

Also, Part 2 does not pre-empt any state law that may restrict or bar any collection activities related to time-barred debt.

Prohibition Against Passive Debt Collection sometimes called "Debt Parking"

The Disclosure Focused Rule requires debt collectors to communicate with a consumer “about a debt” before furnishing information about a debt to a consumer reporting agency ("CRA"). This practice is often called “debt parking.”

Part Two of the Rule requires a debt collector to inform the consumer (either by phone or in writing, including electronic communications) “about a debt,” which could be in the prescribed initial collection notice and wait a reasonable time (14 days) before the debt collector can furnish data to the CRAs. The debt collector must monitor whether the initial communication “about a debt” is undelivered before furnishing data to the CRAs.

Providing Validation Information in a Validation Notice

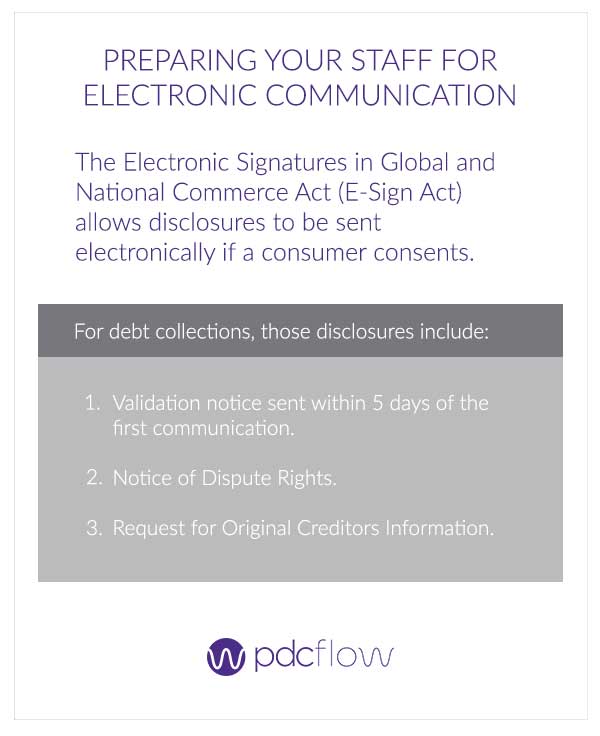

The most significant aspect of the Disclosure Focused Rule was the finalization of specific validation information that must be included in a validation notice as required under 15 U.S.C. §1692g of the FDCPA.

The Bureau provided a Model Form of the validation notice in Appendix B of Part Two. Disclosure of the required validation information, including some optional language, by use of the Model Form or in some other variation that is “substantially similar,” including electronically, will provide the debt collector with a safe harbor for compliance with the Rule.

Although state debt collection regulators had filed a comment with the CFPB requesting that the Model Form include references to any licenses or NMLS reference numbers a collection agency held, that data point is not in the Model Form. Perhaps this would be a “substantially similar” modification to the Model Form that would not disrupt debt collectors’ safe harbor or an opportunity to seek an advisory opinion from the CFPB.

Litigation Considerations

There has been a formidable amount of individual and class action litigation regarding a wide range of alleged technical and substantive letter language under the FDCPA since its enactment in 1977. While the Disclosure Focused Rule may close the door on potential claims that may arise with respect to the use of the Model Form, what variations may or may not be viewed by courts as “substantially similar” in instances where the Model Form is modified in any respect is unknown.

Digital Communication Options

Moreover, as Part One opened the door to the use of modern methods of communication for debt collection, it is also unknown how the method of delivery of communications and the management of consumers’ consent preferences will impact debt collection activities or litigation flowing therefrom. Nevertheless, the ability to utilize the validation notice electronically represents an opportunity to engage with consumers to meet the objectives of the Final Rule which is to ensure that consumer preferences are met.

As creditors and ARM industry entities begin to assess how to modify existing strategies and processes to align with the Final Rule, consideration of when to seek either no-action letters or advisory opinions may be a logical step. Last month the CFPB finalized its advisory opinion program which can be an important opportunity for the industry to leverage when implementation challenges are ultimately recognized.

The Final Rule allows essentially a year for the industry to assess and incorporate these modern forms of communication and prioritize consumer communications preferences. It will be important to keep an eye on the CFPB with respect to actions taken under its authority for enforcement and supervision, areas that will guide the industry as it gears up for implementation.

Get the latest in accounts receivable industry news and digital engagement tips.

Subscribe:

Related Articles