Implementing systems and workflows in line with Regulation F was a huge project for debt collectors. But recent remarks, social media posts, bulletins, blogs and CFPB press releases suggest that the focus on CFPB compliance isn’t over for AR professionals.

Joann Needleman and Leslie Bender, Attorneys at Clark Hill Law, have monitored CFPB rules and actions for many years and continue to follow compliance trends in financial services.

They believe that updating and maintaining your compliance management system (CMS) will continue to be critical as the CFPB moves into a period of enforcement and supervision of the existing rules for ARM and other financial services.

Watch the Webinar Recording

How CFPB Enforcement Decisions Will be Made

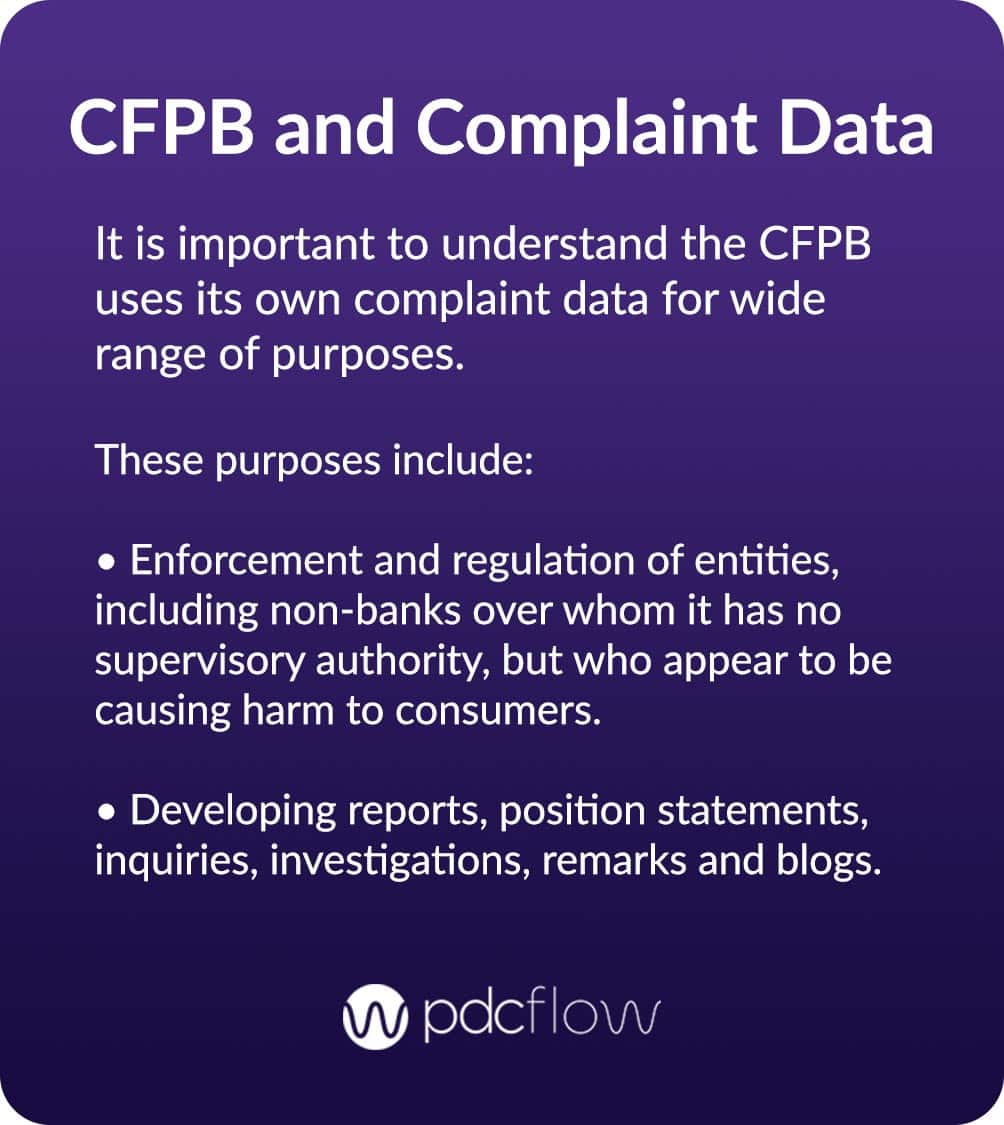

The Bureau has made it clear that much future decision-making will rely on the consumer complaint data they gather. Be aware, the CFPB weighs every type of complaint in their system equally. In addition the CFPB receives complaint data from other consumer protection agencies and law enforcers that it evaluates as well.

“Many organizations challenge whether substantively issues logged in the CFPB’s complaint portal are really a complaint – or merely a dispute or inquiry,” says Bender. “From the CFPB’s perspective, issues filed as complaints are counted as ‘complaints’ regardless of their subject matter or whether a company ultimately resolves the complaint to a consumer’s satisfaction. It is critical to review, investigate and respond to all complaints. Once filed as a complaint, an issue is considered a complaint.”

Key Components of CFPB Compliance

Complaint management isn’t the only area of concern for collectors, though. That’s just one component of your larger CFPB compliance management system. Needleman and Bender say there are four parts of a compliance management strategy that you should construct within your agency.

- Board and management oversight - establish a board of directors (or comparable highest governing body – even if a committee of your department heads) in your organization to handle decision-making for your compliance programs.

- Compliance program - In order to protect consumers and prevent even the potential for harm, track and trend your complaints and disputes and learn from them when updating your compliance policies and procedures. Document, document and document your compliance program expectations. Your compliance program documentation serves as a guide for your workforce and creates standards or expectations against which you can monitor and audit. It is also a great way to assure accountability among your entire workforce (and possibly also vendors).

- Consumer complaint management - Tracking and trending your complaints and disputes and reporting the results out regularly to your highest governing body is a fantastic early warning system. By watching your trends you can identify areas for continuous improvement and compliance controls that are not working as you may intend.

- Compliance monitoring and audits - Trust but verify. Once you have updated your compliance documentation and trained it out to your workforce, now test and monitor on a consistent, predictable and regular basis. This not only helps you detect non-conformities but it also alerts you to opportunities to calibrate or retrain individuals or teams to meet your compliance expectations as well as those of your clients.

Managing Complaints

“It’s not enough that consumers complain to you,” says Needleman. “And it’s not enough that you respond to them.” She says that there is a multi-step process that the handling of each complaint should follow.

This is because, as noted above, proper logging/investigation and handling of complaints will help you notice patterns, like multiple consumers experiencing the same problem. This helps you isolate and correct issues, as well as show the CFPB you can detect and correct your own compliance errors.

What should you do with your complaints?

- Record

- Investigate

- Address all complaints

- Tracking and trending

- Report to your highest governing body about your complaint experience, including litigation, on a regular basis and obtain feedback from the highest governing body.

You can use any system that works for you (and your CFPB compliance team) to log, track and trend complaints. If you’re currently using software like Zendesk and Salesforce for IT tickets, these can easily help organize complaint data for future reference.

Top Bureau Priorities

There are many other areas in which the CFPB under director Chopra is interested. Director Chopra is passionate about consumer protection. Here are just a few of the key topics in which this CFPB has expressed an interest:

Buy Now, Pay Later - Buy now, pay later (BNPL) payment options are a new type of installment loan offered to consumers. It’s not a traditional credit card company using these lending programs and there isn’t a specific company in charge of BNPL lending or regulation. BNPL installment loans are generally not reported on consumers’ credit files.

Because there is very little guidance regarding buy now, pay later options, it is a topic of interest. The CFPB is looking to understand consumer use and impact of BNPL on consumers’ financial outlooks.

Infotech, Data and Bias - This CFPB is dedicated to identifying and rooting out bias. You may need to give some thought to whether or not any of your activities could potentially yield a disparate impact – even if unintended. Look closely at your data and partner with vendors you trust to maintain fair practices. Ask questions of your data vendors.

Dormant Authority

Compliance Management Takeaways

Expect to see more movement regarding fact-finding for businesses such as fintechs, IT vendors, data vendors, payday lenders, BNPL lenders and payment processors as the CFPB under Director Chopra moves into more enforcement areas.

Ensure your practices are in line with CFPB compliance rules and choose vendor partnerships based on trust, communication and transparency. You should also expect extra scrutiny from the Bureau in the future if you use any of the entities listed above. Look out for problems like:

- Equal credit/fair lending/disparate impact

- Complaints and how easily consumers can make them to your company

- Debt substantiation and self-identification of issues and errors

Credit Reporting

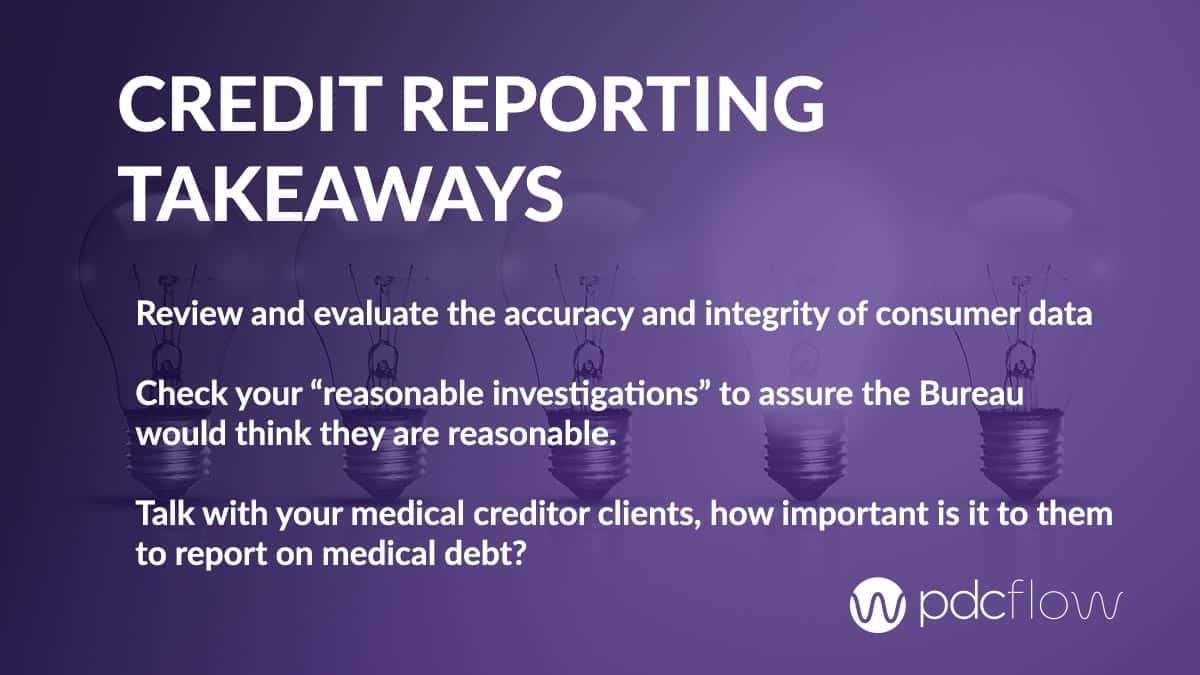

The number one complaint to the CFPB is in regard to credit reporting – specifically in reporting on medical debt. How you assure the accuracy and integrity of the data you furnish as well as how you respond to credit reporting disputes and complaints is important.

You should always evaluate how accurate your consumer data is before using it during debt collection. You can do this through sampling accounts across your lines of business. Tracking, trending and monitoring disputes and complaints is also essential in this effort.

You can’t ignore patterns or issues that arise in your data or through disputes. Don’t wait for complaints to come in before you evaluate whether data is incomplete. Remember to keep your highest governing body in the know about any potential compliance concerns or trends.

What Do You Need To Do?

Considering Director Chopra’s approaches to preventing and rooting out consumer risk and harm, make sure your CFPB compliance management system is as robust as it should be given the size and complexity of your business. Make sure every member of your workforce can find – and understands – all of your policies and procedures.

Monitor workflows and complaints and change procedures accordingly to ensure you are following Regulation F as well as future rules and regulations that are put in place. Don’t forget to keep an eye on state regulatory developments as well as you update your compliance programs. You can add much of this functionality to portals on your website, which can go side-by-side with communication preference management.

Of course, your CMS should address all aspects of compliance within your organization – not just Regulation F. Our goal at PDCflow is to help financial services and AR teams be compliant and engage with consumers and provide a positive customer experience.

For more content, news and compliance best practices to help you win business, increase efficiency, and take more payments, subscribe to the PDCflow blog.

Subscribe to the PDCflow blog

Want to know more about PDCflow Software?

Press ▶️ to watch our explainer video

REDUCE RISK

- ABOUT THE AUTHOR -

Hannah Huerta, Marketing Specialist

Hannah Huerta is a Marketing Specialist at PDCflow. She creates content for the accounts receivable and payment industry.

Related Articles